Public markets haven’t figured out how to bake in AI productivity gains

Yes, AI is driving the stock market. But look closely at what’s actually being priced in. Most of the AI-driven market gains are concentrated in companies that are vendors in the AI space — Nvidia, the hyperscalers, the infrastructure layer. The market is pricing in the building of AI. It hasn’t yet figured out how to price in the using of AI.

That distinction matters enormously.

There’s a line often attributed to Bill Gates, though it actually comes from Roy Amara, the former president of the Institute for the Future: “We tend to overestimate the effect of a technology in the short run and underestimate the effect in the long run.” That’s exactly where we are. The market has overpriced some AI vendor stocks in the short run and dramatically underpriced the productivity gains that AI will deliver to every other company in the long run.

A Century of Productivity Data Tells the Story

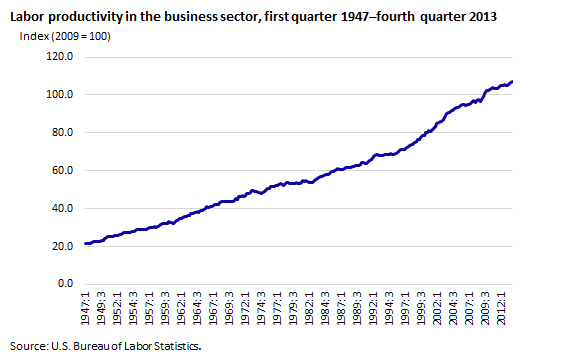

Take a look at the Bureau of Labor Statistics data on U.S. labor productivity over the last century. What you see is fairly slow and steady growth with a handful of notable bumps. U.S. productivity grew at about 2.8% annually from 1947 to 1973 — the post-war boom. Then it slowed. The computing and internet revolution of the late 1990s produced a surge to about 2.9% annual growth. Since 2004, it’s averaged just 1.5%.

{kind=link}

Think about that. The “peak” years — the ones economists celebrate as transformative — still topped out at less than 3% annual productivity growth. The entire computing revolution. The internet. Mobile. Cloud. All of it added up to a few percentage points.

Now look at what the Kansas City Fed found just last month: since late 2022, U.S. labor productivity has risen notably above its pre-pandemic trend, but the pickup is “not yet broad-based.” A small set of industries accounts for most gains. AI adoption is associated with faster productivity growth across industries, but it explains little of the shift in aggregate contributions — because AI adoption is still spreading.

In other words: the early adopters are already seeing it. The rest of the economy hasn’t caught up yet.

Where the Early Adopters Are

The best place to see what’s coming is software startups — the earliest and most aggressive adopters of AI tools.

Example 1: Me. I can’t use AI for everything in my job. I spend a lot of time in meetings and talking to people — you can’t automate that. But every time I use AI to help with something — and I wrote about this in my post on MattBot — the productivity improvement is staggering. Not 10-20%. Not even 50-100%. It’s routinely 50% to 1,000%. That’s not a typo. Specific tasks that used to take me two hours take 20 minutes. Things that took 30 minutes take 30 seconds. The range is 50% to 10x more productive, depending on the task.

Example 2: Our developers. Our junior and mid-level software developers at Markup AI are probably 50-100% more productive this year than they were three years ago (I can’t do the compound math in my head, but it’s not 2.9%), and their productivity is still improving as AI coding assistants get better. Our top-performing developer? Probably 10 to 25x more productive. Yes, you read that right — 10 to 25x. Our overall pace of software development is head-spinning. And it’s accelerating. More on that in some future posts.

The Math Doesn’t Add Up

AI coding assistants do more for software developer productivity than AI does for any other role — for now. They were the first and most natural implementation of AI productivity tools. But AI is getting more specialized by the month. Within two to three years, other white collar roles — marketing, legal, finance, operations — will have close to the same level of productivity boost that developers have today.

Even if you normalize for other sectors of the economy where AI will improve productivity but not as dramatically, it’s hard to see how the AI revolution will deliver only 1-2-3% annual productivity gains to the economy as a whole. And yet — that’s essentially what’s baked into the numbers right now. The market is pricing in incremental improvement when what’s actually coming is a step-function change.I’m not a stock picker, and this isn’t investment advice. But I do think the biggest market mispricing of our generation isn’t in the AI vendor stocks everyone’s watching. It’s in the productivity gains of the companies that are using AI — gains that most analysts haven’t even begun to model.