My new Startup Board Mantra: 1-1-1

Last week, I blogged about Bolster’s Board Benchmark survey results, which really laid bare the lack of diversity on startup boards. There are signs that this is starting to change slowly — one big one is that of all the board searches we are running at Bolster, about ⅔ of them are open to taking on first-time directors; and almost all are committed to increasing diversity on their boards.

This is also something that I would expect to take some time to change. Boards are small. Independent seats aren’t necessarily easy to open up. Seats don’t turn over often. And they take a while to fill, as CEOs are thorough in their recruitment and selection process.

My new mantra for Startup Boards is simple: 1-1-1.

1 member of the management team.

Then 1 independent for every 1 investor.

Simply put, this means you should grow from having 1, to 2, to 3 independent directors as your board grows from 3, to 5, to 7 members.

Here are four tough conversations you may have to have along the way, with some suggestions on how to navigate them. All of these conversations need to come with a point of view of why independence and diversity matters to your company, a lot of empathy, and appreciation for the value the person brings to the table.

The conversation with your co-founder about only one founder/executive on the board. This one will be the most personally difficult, since you likely have a strong personal bond. Expect to hear things like “Aren’t we partners in this business?” and “How come my vote doesn’t count?” Just let your co-founder know that while of course they’re a key partner, the company has a limited number of board seats to fill — each one is a golden opportunity to get an outside perspective on your business and get really good mindshare of an industry expert and create a new brand ambassador. You already have 100% of the mindshare and ambassadorship your co-founder has to offer. You can make that person a board observer, you can make sure they’re in all the key board conversations, and you can even give the person some special voting right in your charter or by-laws if you need to. But do not put them on the board. It’s obviously easier to do this from the beginning as opposed to removing them from the board down the road, but at least try to have the conversation up front that someday, it’s going to happen (note this could be a different dynamic if the person is a founder but no longer active in the business).

The conversation with an existing VC about leaving the board to make room for new investors or an independent. This one will be less personally difficult but will require you to be very artful since the VC is likely contractually given a board seat – meaning you’ll have to get them to give it up voluntarily. You may also want to align with another VC on your board to help the conversation or process along. Depending on the circumstances at hand, your key points of logic could be one of the following: (1) you don’t own as high a percentage of the company as you once did, and I’d like to make room for the new lead investor to join the board without compromising our independents or making the board too big; or (2) I’d like to replace you with an independent director who brings operator perspective and comes from an underrepresented group – it’s important to me that we build a diverse board, and it’s not great that we have don’t have gender or race/ethnic diversity on our board in this day and age. As with a co-founder, you could change this person’s designation to a board observer so they’re still present for key conversations, you’re not changing their Information Rights, which are likely contractually given in your charter, and if required, you can give the person or firm some sort of special voting rights if there’s something they can no longer block (but which they have a contractual right to block) by losing their board vote.

The conversation with a new potential investor about not taking a board seat. If you have a big new lead investor writing a $40mm check into a growth round, you may not have a leg to stand on. But new investors who write smaller checks as you get larger, who might only be buying a 5-10% stake in the business…there, you might have some wiggle room to negotiate. Your best bet is to do it early in the process before you have a term sheet, and do it as an exploratory conversation. Otherwise, your talking points are the same as talking to an existing investor above. Investors are starting to realize the power of a diverse board, and may be open to this conversation. Some are making this a proactive practice, notably two of my long-time investors and directors Fred Wilson and Brad Feld (and some of their partners at Union Square Ventures and Foundry Group) — and those investors have also been willing to mentor the new, first time board members once they join.

The conversation with an existing independent director about leaving the board when their term is up. Perhaps you have an existing independent director who is not adding to the diversity of the board, but you already have a full board. Or perhaps your existing independent director isn’t doing a great job or has grown stale in the role. Once a director is fully vested, you have an easy opportunity to thank them graciously and publicly for their service, extend their option exercise period multiple years, and affirm that they’ll still take your call if you need help on something. You should set this expectation up front when you give the director their initial grant. If they ask why you’re not renewing them, you can simply say something like “We’d like to add some fresh outside perspective to the team.” One thing to think about, particularly for early stage companies, is only giving new directors a 1 or 2-year vest on their first option grant, so you can make sure they’re a high value director…and so you can have the option of an easy exit (or re-up) in a shorter period of time than a traditional 4-year vest.

The net of it is that as CEO of a venture-backed company, you wield an enormous amount of (mostly soft) power around the composition of your board – probably a lot more than you think. You just have to wield that power gently and focus on the importance of building a diverse board in terms of both experience and demographics.

7 Habits of Highly Effective Boards

(This blog post was first published as an article in Entrepreneur Magazine on April 15.)

Creating strong boards can help propel a board forward. Weak and ineffective boards hold a company back.

As a CEO, one of the most important (yet overlooked) tools in the playbook is building and leading a board of directors. Throughout my 20+ years of entrepreneurship, I’ve led four companies (including Bolster, where I’m a co-founder and CEO today) and served on eight boards. I’ve learned that strong boards can help propel a company forward and I’ve also witnessed how weak and ineffective boards can hold companies back. Mediocre or mismanaged advice, plus lack of accountability, can do long-term damage to a business as well.

Drawing from personal experience and anecdotes from dozens of Bolster’s client CEOs, here are some tried and true “Seven Habits of Highly Effective Boards.”

Habit 1: Begin with the board in mind

A lot of CEOs treat board curation as an afterthought, which means that boards tend to consist largely of who happened to be in their network at the company’s inception: investors. CEOs also tend to treat their boards as a distraction or an annoyance. Both of these lines of thought are problematic.

Boards should be viewed as a CEO’s second team (along with their management team), as a strategic weapon that helps the company succeed and as an opportunity to bring new voices and perspectives. Research has shown the more independent and diverse a board is, the better it performs.

Habit 2: Be proactive about board recruiting

Devote as much focus to building a board as to building the executive team. This process is time-consuming and can’t be delegated to anyone else. Aspire to reach people who may feel out of reach. Asking someone to join the board is a big honor, so that ask becomes a good calling card. When recruiting, interview as many contenders as possible, don’t be afraid to reject those who aren’t a good fit and have finalists audition by attending a board meeting. Source broadly, too. Diversity is really important for many reasons; challenge any recruiter, agency or platform to surface diverse board candidates.

Habit 3: Keep your board balanced using the Rule of 1s

Whether it’s a three-person startup board or a seven-person scale-up board, it should include representation from all three director types: investors, management directors and independents. A few basic principles on board composition that work well are what I call the Rule of 1s: First, boards should include one, and only one member of the management team: the CEO. Even if co-founders or C-level managers are shareholders, don’t burn a board seat for a perspective that you have access to regularly. Second, for every new investor to the board, add one independent director, which is the biggest opportunity to introduce external perspectives. If your board gets too crowded with subsequent funding rounds, ask one or more investors to take observer seats to make space for independents. And don’t be afraid to change your board composition over time. Companies are dynamic and boards should be, too.

Habit 4: Cultivate mutual accountability and respect

While a board might seem intimidating, work past the power dynamic and push toward collaboration and mutual accountability. To ensure board members are prepared for meetings, keep commitments and leverage their networks, set the example by demonstrating preparation, consistency and reliability. By regularly delivering pre-read materials to the board several days in advance, the board will build a new habit. By soliciting feedback from board members after each meeting (and even offering them feedback), you’ll show the board that you’re listening. Over time, they’ll lean in, too.

Habit 5: Drive intellectually honest discussions

Even on the healthiest leadership teams, it can be scary to disagree with or challenge a sitting CEO (after all, they are still the one in charge!). But this power dynamic flips in a boardroom, which gives that group a unique opportunity to push and challenge business assumptions. While it may be tempting to look for board members with softer dispositions, it can be more beneficial to have tough, direct board members who aren’t afraid to express their opinions, but who are also good listeners and learners. My favorite discussions are conversations where I’m pushed to consider a different direction. It helps get more done, surfaces better ideas and increases the effectiveness of the company.

Habit 6: Lean in on strategic, lean out on tactics

Even board members who are talented operators have a hard time parachuting into any given situation and being super useful. Getting operational help requires a lot of regular engagement on a specific issue or area. But they must be strategically engaged and understand the fundamental dynamics and drivers of your business: economics, competition and ecosystem. This is an easy habit to reinforce in meetings. If board directors drift toward getting too tactically in the weeds, that’s great feedback to offer after the meeting.

Habit 7: Think outside the box

Good board members understand all the pieces on the chess table; great board members go one step further and pattern match to provide advice, history, context and anticipated consequences. This is an enormous benefit to CEOs focused on the minutiae of the day-to-day, particularly if a business operates in a trailblazing industry where many of the rules may not yet be written. As a CEO, if you’ve never seen something first hand before, it’s hard to get clarity and external perspectives, which is why it’s crucial that great board members bring pattern recognition and “out-of-the-box thinking” to their role.

At the end of the day, boards are there to support and direct a company. There’s no perfect formula, but by implementing these steps with a few healthy habits, CEOs can cultivate strong, dynamic boards for their companies.

Introducing the Bolster Board Benchmarking Survey

Over the years, I’ve had a list of nagging questions every time I’ve contemplated my board, but didn’t have anyone I could turn to who had deep, broad advice on this topic. Those questions were:

- How big should my board be at this stage?

- How many independent directors should I have?

- What is the right profile of an independent director?

- How many options should I give a board member?

- How do I find the best, diverse, talent for my board openings?

That’s why Bolster is excited to announce the launch of our first CEO tool: Board Benchmarking. This application (which is free!) is the first of a series of tools that we’re designing to help CEOs understand the performance, design, and impact of themselves, their executive teams, and their boards. The results of this first application will shed light on the independence, diversity, and compensation of private company boards that’s never been available on a broad basis before.

Why are we starting with Board Benchmarking?

- Increasing Board Diversity is top of mind right now…

…and that means CEOs need to have a handle on three things at the same time to get it right: appropriate board size/number of independent seats, a talent pipeline that is diverse and well vetted, and clear compensation guidelines for independent directors. Diverse employee populations and customer bases start with having a diverse board and a CEO (you!) who is attuned to the benefits of diversity at the top. The longer you wait to prioritize diversity in the boardroom, the harder it becomes to change the makeup of your board. Culture becomes entrenched, recruiting becomes driven by referrals, and before you know it, everyone in an organization looks and thinks a little bit the same way. By capturing data on the diversity and composition of startup boards, we hope to offer an industry-wide snapshot to help CEOs start to have what can often be tricky conversations with their VCs about board size and composition as early as possible. And by pairing that with Bolster’s unique marketplace for diverse and vetted Board-ready talent, we hope to help CEOs slay all three dragons (number of independent seats, talent pipeline, and comp guidelines) at the same time.

- Private company board composition is notoriously tricky to benchmark.

Unlike public companies, which are required to disclose the identities and compensation packages for their boards of directors, private board structure tends to remain…well, private! While this makes sense from a regulatory perspective, it often means private companies CEOs are taking a shot in the dark when it comes to things like when to add independent directors and how much to pay them. By aggregating and anonymizing thousands of data points across hundreds of private companies, we hope to (for the first time ever) provide CEOs with a very real, in-the-moment look at how their board today stacks up against others in similar cohorts.

- Filling an open board seat is a high-priority item for a CEO, and a tough one to get right.

It’s said that good choices come from good options. Early benchmarking results show that half of startup CEOs expect to fill an open board position within the next 12 months. Just as it’s critically important to get the right executives around your (well, now virtual) table, it’s equally, if not even more important to build a board that effectively supports you, your company, and your customers. Every month that goes by with a board vacancy is another month where you’re potentially leaving valuable introductions and perspectives on the table. We hope that by exposing these board searches across such a broad subset of companies, we’ll also empower CEOs to take immediate next steps to fill those vacancies — including help recruiting multiple board candidates directly from the Bolster network.

As we conduct this survey over the next month, we’ll provide greater visibility into the size, composition, diversity, and director compensation of private company boards. We’re also establishing robust pipeline partnerships to amplify board-ready talent from organizations with diverse membership of African American, Hispanic/Latinx, and women orgs. So for anyone interested in adding qualified diverse talent to their boards, we’ll be ready.

Participants who complete the survey will receive early access to your benchmark results and a comprehensive guide to building and managing your Board of Directors.

In early Q1, we’ll invite all participants of our Board Benchmarking survey to log in to Bolster and view their results interactively. CEOs will be able to see how their own boards stack up compared to others in the VC portfolio network or other cohorts. VC partners will be able to see patterns across the entire portfolio.

Watch this space in the coming days and weeks for CEO-specific content about hiring Board members.

We invite you to register as a Bolster client to participate in our Board Benchmarking survey today.

The Startup Ecosystem Needs More Independent Board Members – That’s the Clearest Path to Having Better and More Diverse Boards

I love having independent directors on my Board. They are a great third leg of the stool alongside a CEO/Founder and VCs. They provide the same kind of pattern matching and outside point of view as VCs — but from a completely different perspective, that of an operator or industry expert. The good ones are CEOs or CXOs who aren’t afraid to challenge you. Equally important, they’re not afraid to challenge your VCs. At Return Path, I always had 2 or 3 independent directors at any given time to balance out VCs, and some have become great long term friends like Scott Petry, Jeff Epstein, and Scott Weiss. At Bolster, we’re already having a great experience with our first independent, Cristina Miller, and we’re about to add a second independent. And I’ve served as an independent director multiple times.

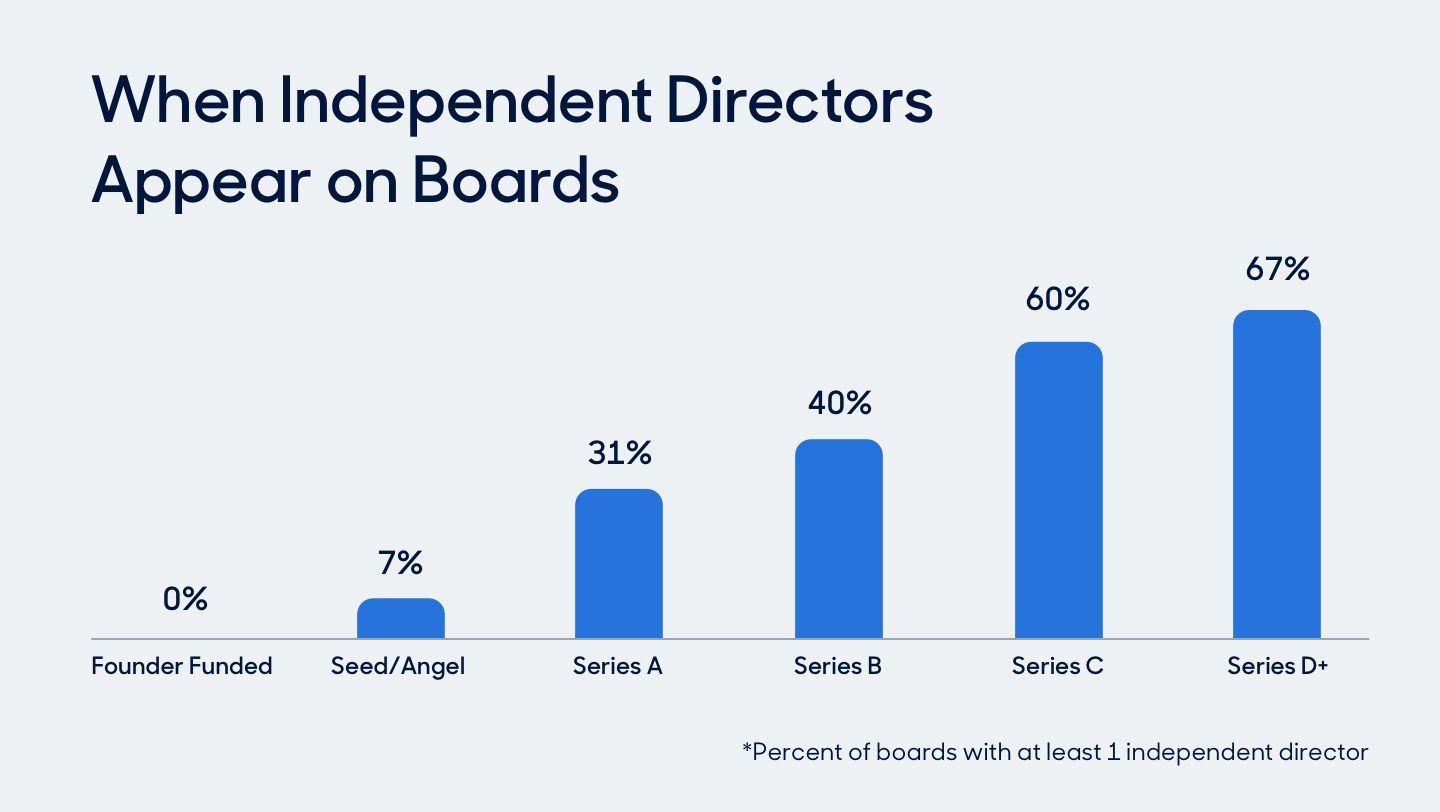

So as you can imagine, I was shocked by one of the headlines coming out of the Board Benchmark study we ran at Bolster across 250+ clients (detailed blog post with a bunch of charts and graphs) that only ⅓ of companies in the study have any independent directors. Even larger companies at the Series C and D levels only have independent directors 60% and 67% of the time. What a missed opportunity for so many companies.

Less surprising, though still sobering, were the numbers on diversity that came out of the study. 79% of the directors in the sample are white. 86% are men. 43% of boards are completely racially homogenous (most all-white) while 80% are mostly racially homogeneous (meaning only one diverse member); 56% are gender homogenous (most all men), while 87% are mostly gender homogenous (only one female). For an industry that is spending a lot of time talking about diversity in leadership teams and on boards, that’s disappointing.

Here’s the linkage of the two topics: The solution to the board diversity problem lies in having more independent directors, since management and VC board seats are often both “fixed” and non-diverse. Independent seats are the easiest to fill with diverse candidates. Conveniently, more independent directors also leads to higher quality boards.

In partnership with some DEI experts, our study also includes some suggested actionable tips for CEOs and board leaders, which I encourage you to read. There are really three simple (IMO) steps to having more diverse boards, and there is some good news in the Bolster study around these points:

- Add independent director seats. 50% of the companies in the survey either have or expect to have an independent board seat open within 12 months. That’s a good start, but honestly, I can’t imagine running any board without at least 1-2 independent directors (up to 3-4 for larger companies), starting on Day 1. Given that only ⅓ of companies in the sample have any independent board members at all, the 50% number feels quite low.

- Open the recruiting funnel to include first-time directors. Historically, companies have mainly targeted current or former CEOs or people who have board experience to be independent directors. That is a recipe to perpetuate having mostly white male board members. But Bolster has done a few dozen board searches so far, and 66% of those clients have expressed a willingness to take on first-time directors, as long as they are “board ready,” which we define as having been on any kind of board, not just a corporate board; having reported to a founder or CEO and had regular interaction with and presentations to a board; or having significant experience as a formal or informal advisor. Once you widen the funnel to include all candidates who meet those criteria, you can very easily have a diverse slate of highly qualified candidates. Bolster is a great source of these candidates (this is a real focal point for our business), but there are plenty of other online or search firm sources as well.

- Have the courage to limit the number of management/investor board members. Whether or not you can add independent board members may be a function of how many seats you have to play with in your corporate charter. Of course, you can add seats indefinitely, but there’s no reason to have a 7-person board for your Series A company. My rule of thumbs on this are simple: (a) Only one founder member of the management team on the Board – more than that is a waste of a valuable board slot; and (b) VCs should always be less than 50% of your board members, so as new ones roll on, old ones should roll off – or add a VC and an independent at the same time. Both of these take serious effort and courage, both are worth it, and both probably merit a longer blog post someday.

The Board Benchmark study also had a wealth of information about compensation for independent directors — cash vs. stock, what kind of stock, how much stock, vesting and acceleration provisions.

Here’s a Slideshare of the full survey results, in case this and/or the Bolster blog link isn’t detailed enough for you:

If you’re interested in learning more, the survey is free to take and all the granular results (including comp benchmarks) are available to benchmark against your company if you take it. Just email me if you’re interested at [email protected].

Book Short: Choose Voice!

Book Short: Choose Voice!

I took a couple days off last week and decided to re-read two old favorites. One –Ayn Rand’s The Fountainhead — my fourth reading — will take me a little longer to process and figure out if there’s a good intersection with the blog. One would think so with entrepreneurship as the topic, but my head still hurts from all the objectivism. The second — Exit, Voice, and Loyalty, by Albert O. Hirschman — is today’s topic.

I can’t remember when I first read Exit, Voice, and Loyalty. It was either in senior year of high school Economics or Government; or in freshman year of college Political Philosophy. Either way, it was a long time ago, and for some reason, some of the core messages of this quirkly little 125 page political/economic philosophy book have stayed with me over the years. I remembered the book incorrectly as a book about political systems, and I think it was born consciously in the wake of Eugene McCarthy’s somewhat revolutionary challenge to a sitting President Johnson for the Democratic Party nomination in 1968. But the book is actually about business; it’s just about businesses and their customers, not corporations as social structures (the latter being more of an interest to me). Written by an academic economist (I think), the book has its share of gratuitous demonstrative graphs, 2×2 matrices, and SAT words. But its central premise is a gem for anyone who runs an organization of any size.

The central premise is that there are really two paths by which one can express dissatisfaction with a temporary, curable lapse in an organization: exit (bailing), or voice (trying to fix what’s wrong from within). The third key element, Loyalty, is less a path in and of itself but more an agent that “holds exit at bay and activates voice.”

You need to read the book and apply it to your own circumstances to really get into it, but for me, it’s all about breeding loyalty as a means of making voice the path of least resistance, even when exit is a freely available option (few of us run totalitarian states or monopolies, after all). That to me is the definition of a successful enterprise, both internally and externally.

With your customers: make your product so irresistible, and make your customer service so deep, that your customers feel an obligation to help you fix what they perceive to be wrong with your product first, rather than simply complain about price or flee to a competitor.

With your employees: make your company the best possible place you can think of to work so that even in as ridiculously fluid a job market as we live in, your employees will come to their manager, their department head, the head of HR, or you as leader to tell you when they’re unhappy instead of just leaving, or worse, sulking.

With your company (you as employee): make yourself indispensible to the organization and do such a great job that if things go wrong with your performance or with your role, your manager’s loyalty to you leads him or her to give you open feedback and coach you to success rather than unceremoniously show you the door.

Ok, this wasn’t such a short book short — probably the longest I’ve ever written in this blog, and certainly the highest ratio of short:actual book. But if you’re up for a serious academic framework (quasi-business but not exclusively) to apply to your management techniques, this short 1970 book is as valid today as when it was written. Thanks to David Ramert (I am pretty sure I read it in high school) for introducing it to me way back when!

Startup CEO (OnlyOnce- the book!), Part III – Pre-Order Now

Startup CEO (OnlyOnce – the book!), Part III – Pre-Order Now

My book, Startup CEO: A Field Guide to Scaling Up Your Business, is now available for pre-order on Amazon in multiple formats (Print, Kindle), which is an exciting milestone in this project! The book is due out right after Labor Day, but Brad Feld tells me that the more pre-orders I have, the better. Please pardon the self-promotion, but click away if you’re interested!

Here are a few quick thoughts about the book, though I’ll post more about it and the process at some point:

- I’ll be using the hashtag #startupceo more now to encourage discussion of topics related to startup CEOs – please join me!

- The book has been described by a few CEOs who read it and commented early for me along the lines of “The Lean Startup movement is great, but this book starts where most of those books end and takes you through the ‘so you have a product that works in-market – now what?’ questions”

- The book is part of the Startup Revolution series that Brad has been working on for a couple years now, including Do More (Even) Faster, Venture Deals, Startup Communities, and Startup Life (with two more to come, Startup Boards and Startup Metrics)

- Writing a book is a LOT harder than I expected!

At this point, the best thing I can do to encourage you to read/buy is to share the full and final table of contents with you, sections/chapters/headings. When I get closer in, I may publish some excerpts of new content here on Only Once. Here’s the outline:

Part I: Storytelling

- Chapter 1: Dream the Possible Dream…Entrepreneurship and Creativity, “A Faster Horse,” Vetting Ideas

- Chapter 2: Defining and Testing the Story…Start Out By Admitting You’re Wrong, A Lean Business Plan Template, Problem, Solution, Key Metrics, Unique Value Proposition and Unfair Advantages, Channels, Customer Segments, Cost Structure and Revenue Streams

- Chapter 3: Telling the Story to Your Investors…The Business Plan is Dead. Long Live the Business Plan, The Investor Presentation, The Elevator Pitch, The Size of the Opportunity, Your Competitive Advantage, Current Status and Roadmap from Today, The Strength of Your Team, Summary Financials, Investor Presentations for Larger Startups

- Chapter 4: Telling the Story to Your Team…Defining Your Mission, Vision and Values, The Top-down Approach, The Bottom-Up Approach, The Hybrid Approach, Design a Lofty Mission Statement

- Chapter 5: Revising the Story…Workshopping, Knowing When It’s Time to Make a Change, Corporate Pivots: Telling the Story Differently, Consolidating, Diversifying, Focusing, Business Pivots: Telling a Different Story

- Chapter 6: Bringing the Story to Life…Building Your Company Purposefully, The Critical Elements of Company-Building, Articulating Purpose: The Moral of the Story, You Can Be a Force for Helping Others—Even If Indirectly

Part II: Building the Company’s Human Capital

- Chapter 7: Fielding a Great Team…From Protozoa to Pancreas, The Best and the Brightest, What About HR?, What About Sales & Marketing?, Scaling Your Team Over Time

- Chapter 8: The CEO as Functional Supervisor…Rules for General Managers

- Chapter 9: Crafting Your Company’s Culture…, Introducing Fig Wasp #879, Six Legs and a Pair of Wings, Let People Be People, Build an Environment of Trust

- Chapter 10: The Hiring Challenge…Unique Challenges for Startups, Recruiting Outstanding Talent, Staying “In-Market”, Recruitment Tools, The Interview: Filtering Potential Candidates, Two Ears One Mouth, Who Should You Interview?, Onboarding: The First 90 Days

- Chapter 11: Every Day in Every Way, We Get a Little Better…The Feedback Matrix, 1:1 Check-ins, “Hallway” Feedback, Performance Reviews, The 360, Soliciting Feedback on Your Own Performance, Crafting and Meeting Development Plans

- Chapter 12: Compensation…General Guidelines for Determining Compensation, The Three Elements of Startup Compensation, Base Pay, Incentive Pay, Equity

- Chapter 13: Promoting …Recruiting from Within, Applying the “Peter Principle” to Management, Scaling Horizontally, Promoting Responsibilities Rather than Swapping Titles

- Chapter 14: Rewarding: “It’s the Little Things” That Matter…It Never Goes Without Saying, Building a Culture of Appreciation

- Chapter 15: Managing Remote Offices and Employees…Brick and Mortar Values in a Virtual World, Best Practices for Managing Remote Employees

- Chapter 16: Firing: When It’s Not Working…No One Should Ever Be Surprised to Be Fired, Termination and the Limits of Transparency, Layoffs

Part III: Execution

- Chapter 17: Creating a Company Operating System…Creating Company Rhythms, A Marathon? Or a Sprint?

- Chapter 18: Creating Your Operating Plan and Setting Goals…Turning Strategic Plans into Operating Plans, Financial Planning, Bringing Your Team into Alignment with Your Plans, Guidelines for Setting Goals

- Chapter 19: Making Sure There’s Enough Money in the Bank…Scaling Your Financial Instincts, Boiling the Frog, To Grow or to Profit? That Is the Question, First Perfect the Model, Choosing Growth, Choosing Profits, The Third Way

- Chapter 20: The Good, the Bad, and the Ugly of Financing…Equity Investors, Venture Capitalists, Angel Investors, Strategic Investors, Debt, Convertible Debt, Venture Debt, Bank Loans, Personal Debt, Bootstrapping, Customer Financing, Your Own Cash Flow

- Chapter 21: When and How to Raise Money…When to Start Looking for VC Money, The Top 11 Takeaways for Financing Negotiations

- Chapter 22: Forecasting and Budgeting…Rigorous Financial Modeling, Of Course You’re Wrong—But Wrong How?, Budgeting in a Context of Uncertainty, Forecast, Early and Often

- Chapter 23: Collecting Data…External Data, Learning from Customers, Learning from (Un)Employees, Internal Data, Skip-Level Meetings, Subbing, Productive Eavesdropping

- Chapter 24: Managing in Tough Times…Managing in an Economic Downturn, Hope Is Not a Strategy—But It’s Not a Bad Tactic, Look for Nickels and Dimes under the Sofa, Never Waste a Good Crisis, Managing in a Difficult Business Situation

- Chapter 25: Meeting Routines…Lencioni’s Meeting Framework, Skip-Level Meetings, Running a Productive Offsite

- Chapter 26: Driving Alignment…Five Keys to Startup Alignment, Aligning Individual Incentives with Global Goals

- Chapter 27: Have You Learned Your Lesson?…The Value (and Limitations) of Benchmarking, The Art of the Post-Mortem

- Chapter 28: Going Global…Should Your Business Go Global?, How to Establish a Global Presence, Overcoming the Challenges of Going Global, Best Practices for Managing International Offices and Employees

- Chapter 29: The Role of M&A…Using Acquisitions as a Tool in Your Strategic Arsenal, The Mechanics of Financing and Closing Acquisitions, Stock, Cash, Earn Out, The Flipside of M&A: Divestiture, Odds and Ends, Integration (and Separation)

- Chapter 30: Competition…Playing Hardball, Playing Offense vs. Playing Defense, Good and Bad Competitors

- Chapter 31: Failure…Failure and the Startup Model, Failure Is Not an Orphan

Part IV: Building and Leading a Board of Directors

- Chapter 32: The Value of a Good Board…Why Have a Board?, Everybody Needs a Boss, The Board as Forcing Function, Pattern Matching, Forests, Trees, Honest Discussion and Debate

- Chapter 33: Building Your Board…What Makes a Great Board Member?, Recruiting a Board Member, Compensating Your Board, Boards as Teams, Structuring Your Board, Board Size, Board Committees, Chairing the Board, Running a Board Feedback Process, Building an Advisory Board

- Chapter 34: Board Meeting Materials…“The Board Book”, Sample Return Path Board Book, The Value of Preparing for Board Meetings

- Chapter 35: Running Effective Board Meetings…Scheduling Board Meetings, Building a Forward-Looking Agenda, In-Meeting Materials, Protocol, Attendance and Seating, Device-Free Meetings, Executive and Closed Sessions

- Chapter 36: Non-Board Meeting Time…Ad Hoc Meetings, Pre-Meetings, Social Outings

- Chapter 37: Decision-Making and the Board…The Buck Stops—Where?, Making Difficult Decisions in Concert, Managing Conflict with Your Board

- Chapter 38: Working with the Board on Your Compensation and Review…The CEO’s Performance Review, Your Compensation, Incentive Pay, Equity, Expenses

- Chapter 39: Serving on Other Boards…The Basics of Serving on Other Boards, Substance, or Style?

Part V: Managing Yourself So You Can Manage Others

- Chapter 40: Creating a Personal Operating System…Managing Your Agenda, Managing Your Calendar, Managing Your Time, Feedback Loops

- Chapter 41: Working with an Executive Assistant…Finding an Executive Assistant, What an Executive Assistant Does

- Chapter 42: Working with a Coach…The Value of Executive Coaches, Areas Where an Executive Coach Can Help

- Chapter 43: The Importance of Peer Groups…The Gang of Six, Problem-Solving in Tandem

- Chapter 44: Staying Fresh…Managing the Highs and Lows, Staying Mentally Fresh, At Your Company, Out and About, Staying Healthy, Me Time

- Chapter 45: Your Family…Making Room for Home Life, Involving Family in Work, Bringing Work Principles Home

- Chapter 46: Traveling…Sealing the Deal with a Handshake, Making the Most of Travel Time, Staying Disciplined on the Road

- Chapter 47: Taking Stock of the Year…Celebrating “Yes”; Addressing “No”, Are You Having Fun?, Are You Learning and Growing as a Professional?, Is It Financially Rewarding?, Are You Making an Impact?

- Chapter 48: A Note on Exits…Five Rules of Thumb for Successfully Selling Your Company

If you’re still with me and interested, again here are the links to pre-order (Print, Kindle).

Comment on Political versus Corporate Leadership, Part II: Admitting Mistakes

Comment on Political versus Corporate Leadership, Part II: Admitting Mistakes

My colleague Mike Mayor writes:

So you’e only asking for politicians to be honest Matt? Is that all? 🙂

Couldn’t agree more on the CEO side. A CEO who cannot admit to failure is doomed to be surrounded by “yes men” and, therefore, must go it alone, whereas the CEO who admits to having the odd bad idea every now and then is more likely to get truthful and accuruate information from those around him/her. Which scenario would you prefer to base your next decision on?

However, I look more to Hollywood for fostering the faux CEO/Board Room stereotypes, not politics. Look no further than the highest ranked show among 18 to 46 year olds: The Apprentice. Trump is just one contemporary example of successfully perpetuating the “kill or be killed” mentality of the ideal CEO. In his book, “How to Get Rich” one of his lessons is to “never take the blame for anything” (meanwhile Trump gets rich by being a caricature of a CEO).

The ideal CEO needs to set the example for the behavior of his employees, and creates opportunities by building relationships not “squashing the competition.” And like it or not, the ideal Board Room is actually a Think Tank of great minds working toward a common goal rather than a place to play mind games and mental poker.

Unfortunately, both of these things make for a horrible TV show but do contribute to building truly great companies! On the other hand, watch too many TV shows (or follow the politician’s lead) and you’ll likely become a CEO whose success is comparable to the CEOs of Enron and Tyco.

The Gift of Feedback, Part IV

The Gift of Feedback, Part IV

I wrote a few weeks ago about my live 360 – the first time I’ve ever been in the room for my own review discussion. I now have a development plan drafted coming out of the session, and having cycled it through the contributors to the review, I’m ready to go with it. As I did in 2008, 2009, and 2011, I’m posting it here publicly. This time around, there are three development items:

- Continue to spend enough time in-market. In particular, look for opportunities to spend more time with direct clients. There was a lot of discussion about this at my review. One director suggested I should spend at least 20% of my time in-market, thinking I was spending less than that. We track my time to the minute each quarter, and I spend roughly 1/3 of my time in-market. The problem is the definition of in-market. We have a lot of large partners (ESPs, ISPs, etc.) with whom I spend a lot of time at senior levels. Where I spend very little time is with direct clients, either as prospects or as existing clients. Even though, given our ASP, there isn’t as much leverage in any individual client relationship, I will work harder to engage with both our sales team and a couple of larger accounts to more deeply understand our individual client experience.

- Strengthen the Executive Committee as a team as well as using the EC as the primary platform for driving accountability throughout the organization. On the surface, this sounds like “duh,” isn’t that the CEO’s job in the first place? But there are some important tactical items underneath this, especially given that we’ve changed over half of our executive team in the last 12 months. I need to keep my foot on the accelerator in a few specific ways: using our new goals and metrics process and our system of record (7Geese) rigorously with each team member every week or two; being more authoritative about the goals that end up in the system in the first place to make sure my top priorities for the organization are being met; finishing our new team development plan, which will have an emphasis on organizational accountability; and finding the next opportiunity for our EC to go through a management training program as a team.

- Help stakeholders connect with the inherent complexity of the business. This is an interesting one. It started out as “make the business less complex,” until I realized that much of the competitive advantage and inherent value from our business comes fom the fact that we’ve built a series of overlapping, complex, data machines that drive unique insights for clients. So reducing complexity may not make sense. But helping everyone in and around the business connect with, and understand the complexity, is key. To execute this item, there are specifics for each major stakeholder. For the Board, I am going to experiment with a radically simpler format of our Board Book. For Investors, Customers, and Partners, we are hard at work revising our corporate positioning and messaging. Internally, there are few things to work on — speaking at more team/department meetings, looking for other opportunities to streamline the organization, and contemplating a single theme or priority for 2015 instead of our usual 3-5 major priorities.

Again, I want to thank everyone who participated in my 360 this year – my board, my team, a few “lucky” skip-levels, and my coach Marc Maltz. The feedback was rich, the experience of observing the conversation was very powerful, and I hope you like where the development plan came out!

Political versus Corporate Leadership, Part III: The First Debate

Political versus Corporate Leadership, Part III: The First Debate

Well, there you have it. Both of my first two postings on this subject — Realism vs. Idealism and Admitting Mistakes — came up in last night’s debate.

At one point, in response to Kerry’s attempted criticism of him for expressing two different views on the situation in Iraq, Bush responded that he thought he could — and had to — be simultaneously a realist and an optimist. And a few minutes later, Kerry admitted a mistake and brilliantly turned the tables on Bush by saying something to the effect of “I made a mistake in how I talked about Iraq, and he made a mistake by taking us to war with Iraq — you decide which is worse.”

So each candidate exhibited at least one of the traits of good corporate leadership, but on this front anyway, I think Kerry did a better job last night in turning one of his mistakes into a zinger against his opponent.

I Love My Job

I Love My Job

The picture below is a picture of my dress shoes in my closet at home. You may note that they all have dust on them. That's because I didn't put them on once for six weeks.

When we started Return Path back in 1999, we sat down to write our employee handbook, and all I could think was "what things can we add in here that will make this company a unique place to work?" And one of them was a six week paid sabbatical after 7 years. It didn't occur to me that we'd even exist after 7 years. Then for good measure, we said, "7 years and every 5 years after that."

I'm happy to report that everyone who has hit their 7 year anniversary has taken the time off. Some have traveled around the world, some have rented a house or villa somewhere, others (like me) did a "stay-cation." Although my sabbatical was delayed (and quite hard to schedule), it was a fantastic experience. I completely unplugged from work. Cold turkey. No email, no calls. Spending time with Mariquita and my kids, which I never get to do much of, was completely refreshing and energizing. And everything went fine at work, as I expected. Business is in the best shape it's ever been in, and my amazingly talented executive team and assistant handled everything without missing a beat.

But back to the subject line of this post. I figured a few things out while I was away. One was that I haven't actually become a workaholic over the years despite working hard. I *could* unplug without feeling aimless. Another was that it's really nice to be untethered from the Internet, but it's near impossible to go through life now without some minor usage of the web and messaging. But by far my biggest insight is plain and simple: I love my job. It's not that I didn't know that before, but I had more thoughtful time to break that down while I was away:

1. I love what I do: I consider myself extremely fortunate to love the substance of my job. The diversity of experiences that I have within a given week or day as a general manager, the interactions with people, shaping the business strategy, travel — it's all right up my alley. So many people out there don't have that match between interest, passion, skill, and reality.

2. I love who I work with: I have to admit that I stack the deck here since I do the hiring and firing, but the reality is that my colleagues at work are also my friends. Not working was one thing. Not talking to one particular subset of my life for six weeks was something else and just plain weird. I just missed them and the interactions we have, which always blend the professional with the social.

3. I love what we are working on: We have an incredibly interesting business at Return Path. It's very intellectually engaging, sometimes to a fault. The spam problem is incredibly complex, and we're coming up with some extremely innovative approaches to reduce its impacts and hopefully someday eradicate it. We're not curing cancer as I always say internally, but we're also engaged in some high impact problem solving that I just love.

So there you have it. My work shoes are now dusted off and back in action. It's great to be back. We'll see how long I can stay in "mental vacation" mode, how much more time I can try to make for my family now that I'm back in my work routine, and whether the fresh perspective translates into any new actions or decisions at work. But the best thought of all is that my 12 year anniversary is only another year and a half away!

Book Short: a Corporate Team of Rivals

Book Short: a Corporate Team of Rivals

One of the many things I have come to love about the Christmas holiday every year is that I get to go running in Washington DC. Running the Monuments is one of the best runs in America. Today, at my mother-in-law’s suggestion, I stopped i8n at the Lincoln Memorial mid-run and read his second inaugural address again (along with the Gettysburg Address). I had just last week finished Doris Kearns Goodwin’s Team of Rivals: The Political Genius of Abraham Lincoln, and while I wasn’t going to blog about it as it’s not a business book, it’s certainly a book about leadership from which any senior executive or CEO can derive lessons.

Derided by his political opponents as a “second-rate Illinois lawyer,” Lincoln, who arrived somewhat rapidly and unexpectedly on the national scene at a time of supreme crisis, obviously more than rose to the occasion and not only saved the nation and freed the slaves but also became one of the greatest political leaders of all time. He clearly had his faults — probably at the top of the list not firing people soon enough like many of his incompetent Union Army generals — but the theme of the book is that he had as one of his greatest strengths the ability to co-opt most of his political rivals and get them to join his cabinet, effectively neutering them politically as well as showing a unity government to the people.

This stands in subtle but important contrast to George Washington, who filled his cabinet with men who were rivals to each other (Hamilton, Jefferson) but who never overtly challenged Washington himself.

Does that Team of Rivals concept — in either the Lincoln form or the Washington form — have a place in your business? I’d say rarely in the Lincoln sense and more often in the Washington sense.

Lincoln, in order to be effective, didn’t have much of a choice. Needing regional and philosophical representation on his cabinet at a time of national crisis, bringing Seward, Chase, and Bates on board was a smart move, however much a pain in the ass Chase ended up being. There certainly could be times when corporate leadership calls for a representative executive team or even Board, for example in a massive merger with uncertain integration or in a scary turnaround. But other than extreme circumstances like that, the Lincoln model is probably a recipe for weak, undermined leadership and heartache for the boss.

The Washington model is different and can be quite effective if managed closely. One could argue that Washington didn’t manage the seething Hamilton and frothy Jefferson closely enough, but the reality is that the debates between the two of them in the founding days of our government, when well moderated by Washington, forged better national unity and just plain better results than had Washington had a cabinet made up of like-minded individuals. As a CEO, I love hearing divergent opinion on my executive team. That kind of discussion is challenging to manage — at least in our case we don’t have people at each other’s throats — but as long as you view your job as NOT to create compromises to appease all factions but instead to have the luxury of hearing multiple well articulated points of view as inputs to a decision you have to make, then you and your company end up with a far, far better result.