The Startup Ecosystem Needs More Independent Board Members – That’s the Clearest Path to Having Better and More Diverse Boards

I love having independent directors on my Board. They are a great third leg of the stool alongside a CEO/Founder and VCs. They provide the same kind of pattern matching and outside point of view as VCs — but from a completely different perspective, that of an operator or industry expert. The good ones are CEOs or CXOs who aren’t afraid to challenge you. Equally important, they’re not afraid to challenge your VCs. At Return Path, I always had 2 or 3 independent directors at any given time to balance out VCs, and some have become great long term friends like Scott Petry, Jeff Epstein, and Scott Weiss. At Bolster, we’re already having a great experience with our first independent, Cristina Miller, and we’re about to add a second independent. And I’ve served as an independent director multiple times.

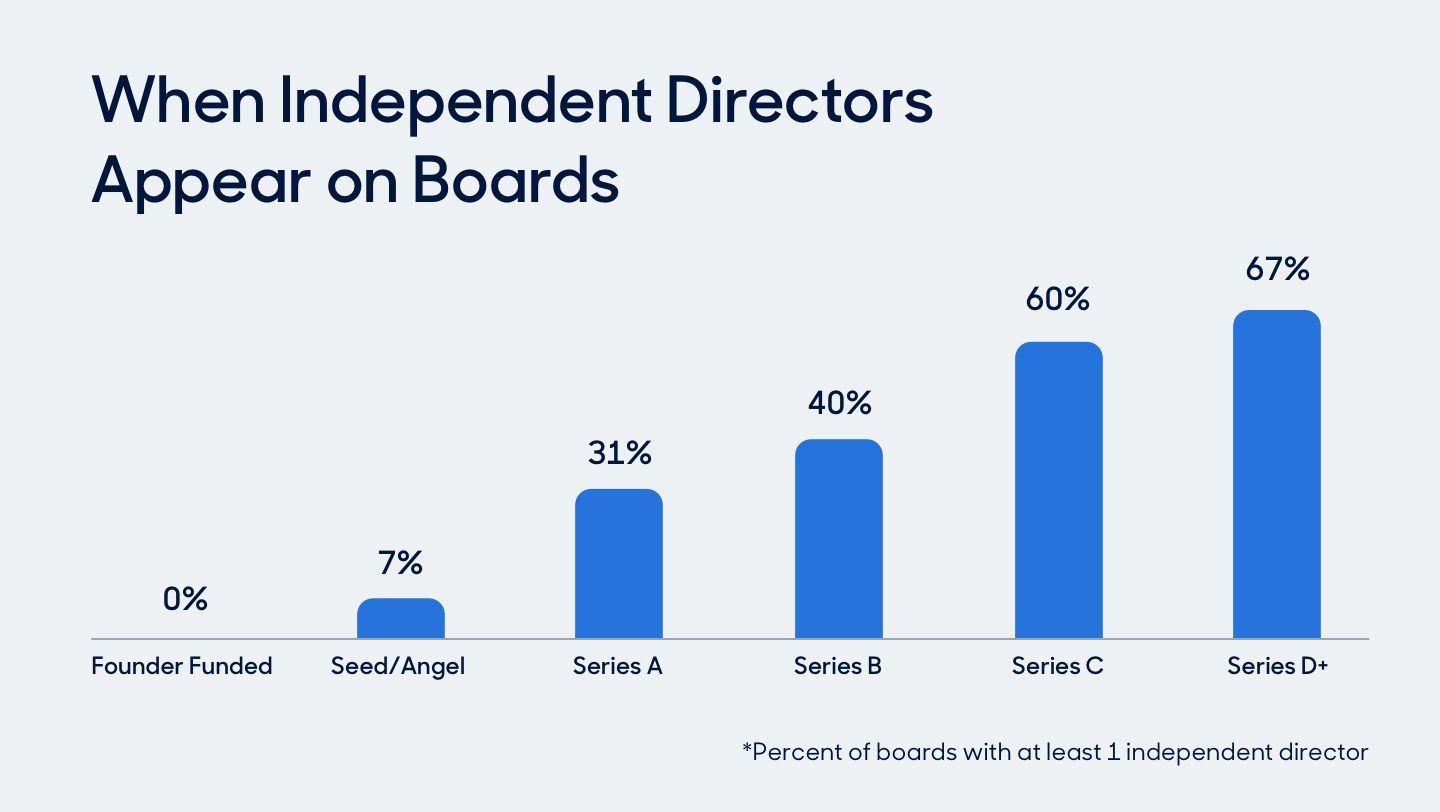

So as you can imagine, I was shocked by one of the headlines coming out of the Board Benchmark study we ran at Bolster across 250+ clients (detailed blog post with a bunch of charts and graphs) that only ⅓ of companies in the study have any independent directors. Even larger companies at the Series C and D levels only have independent directors 60% and 67% of the time. What a missed opportunity for so many companies.

Less surprising, though still sobering, were the numbers on diversity that came out of the study. 79% of the directors in the sample are white. 86% are men. 43% of boards are completely racially homogenous (most all-white) while 80% are mostly racially homogeneous (meaning only one diverse member); 56% are gender homogenous (most all men), while 87% are mostly gender homogenous (only one female). For an industry that is spending a lot of time talking about diversity in leadership teams and on boards, that’s disappointing.

Here’s the linkage of the two topics: The solution to the board diversity problem lies in having more independent directors, since management and VC board seats are often both “fixed” and non-diverse. Independent seats are the easiest to fill with diverse candidates. Conveniently, more independent directors also leads to higher quality boards.

In partnership with some DEI experts, our study also includes some suggested actionable tips for CEOs and board leaders, which I encourage you to read. There are really three simple (IMO) steps to having more diverse boards, and there is some good news in the Bolster study around these points:

- Add independent director seats. 50% of the companies in the survey either have or expect to have an independent board seat open within 12 months. That’s a good start, but honestly, I can’t imagine running any board without at least 1-2 independent directors (up to 3-4 for larger companies), starting on Day 1. Given that only ⅓ of companies in the sample have any independent board members at all, the 50% number feels quite low.

- Open the recruiting funnel to include first-time directors. Historically, companies have mainly targeted current or former CEOs or people who have board experience to be independent directors. That is a recipe to perpetuate having mostly white male board members. But Bolster has done a few dozen board searches so far, and 66% of those clients have expressed a willingness to take on first-time directors, as long as they are “board ready,” which we define as having been on any kind of board, not just a corporate board; having reported to a founder or CEO and had regular interaction with and presentations to a board; or having significant experience as a formal or informal advisor. Once you widen the funnel to include all candidates who meet those criteria, you can very easily have a diverse slate of highly qualified candidates. Bolster is a great source of these candidates (this is a real focal point for our business), but there are plenty of other online or search firm sources as well.

- Have the courage to limit the number of management/investor board members. Whether or not you can add independent board members may be a function of how many seats you have to play with in your corporate charter. Of course, you can add seats indefinitely, but there’s no reason to have a 7-person board for your Series A company. My rule of thumbs on this are simple: (a) Only one founder member of the management team on the Board – more than that is a waste of a valuable board slot; and (b) VCs should always be less than 50% of your board members, so as new ones roll on, old ones should roll off – or add a VC and an independent at the same time. Both of these take serious effort and courage, both are worth it, and both probably merit a longer blog post someday.

The Board Benchmark study also had a wealth of information about compensation for independent directors — cash vs. stock, what kind of stock, how much stock, vesting and acceleration provisions.

Here’s a Slideshare of the full survey results, in case this and/or the Bolster blog link isn’t detailed enough for you:

If you’re interested in learning more, the survey is free to take and all the granular results (including comp benchmarks) are available to benchmark against your company if you take it. Just email me if you’re interested at [email protected].

links for 2006-06-05

-

Dallas Mavs owner and Internet entrepreneur Mark Cuban on Click Fraud, a notorious member of the Internet Axis of Evil

Book Short: A SPIN Selling Companion

Book Short: A SPIN Selling Companion

At Return Path, we’re big believers in the SPIN Selling methodology popularized by Neil Rackham. It just makes sense. Spend more time listening than talking on a sales call, uncover your prospect’s true needs and get him or her to articulate the need for YOUR product. Though it doesn’t reference SPIN Selling, Why People Don’t Buy Things, by Kim Wallace and Harry Washburn is a nice companion read.

Rooted in psychology and cognitive science, Why People Don’t Buy Things presents a very practical sales methodology called Buying Path Selling. Understand how your prospect is making his or her buying decision and what kind of buyer he or she is, be more successful at uncovering needs and winning the business.

The book has two equally interesting themes, rich with examples, but the one I found to be easiest to remember was to vary your language (both body and verbal) with the buyer type. And the book illustrates three archetypes: The Commander, The Thinker, and The Visualizer. There are some incredibly insightful and powerful ways to recognize the buyer type you’re dealing with in the book.

But most of the cues the authors rely on are physical, and lots of sales are done via telephone. So I emailed the author to ask for his perspective on this wrinkle. Kim wrote back the following (abridged):

Over the phone it is fairly easy to determine a prospect’s modality. I’ve developed a fun, conversational question which can be asked up front, “As you recall some of your most meaningful experiences at XYZ, what words, thoughts, feelings or visuals come to mind? Anything else?”If you’re interested in letting your blog readers test their modalities, the link below will activate a quick 10 question quiz from our website that generates ones modality scores along how they compare with others. (It’s like Myers-Briggs applied to decision making.) http://www.wallacewashburn.com/quiz.shtml

In any case, if you are a sales, marketing, or client services professional (or even if you just play one on TV), Why People Don’t Buy Things is a quick, insightful read. Thanks for the quick response, Kim!

Introducing Bolster

As I mentioned earlier this summer, I’ve been working on a new startup the past few months with a group of long-time colleagues from Return Path. Today, we are officially launching the new company, which is called Bolster. The official press release is here.

Here’s the business concept. Bolster is a talent marketplace, but not just any talent marketplace. We are building a talent marketplace exclusively for what we call on-demand (or freelance) executives and board members. We are being really picky about curating awesome senior talent. And we are targeting the marketplace at the CEOs and HR leaders at venture- and PE-backed startups and scaleups. We’re not a search firm. We’re not trying to be Catalant or Upwork. We’re not a job board.

To keep both sides of the marketplace engaged with us, we are also building out suites of services for both sides – Members and Clients. For Members, our services will help them manage their careers as independent consultants. For Clients, our services will help them assess, benchmark and diversify their leadership teams and boards.

We have a somewhat interesting founding story, which you can read on our website here. But the key points are this. I have 7 co-founders, with whom I have worked for a collective 88 years — Andrea Ponchione, Jack Sinclair, Shawn Nussbaum, Cathy Hawley, Ken Takahashi, Jen Goldman, and Nick Badgett. We have three engineers with whom we’ve worked for several years who have been on board as contractors so far – Kayce Danna, Chris Paynes, and Chris Shealy. We have four primary investors, who I’ve also known and worked closely with for a collective 77 years — High Alpha and Scott Dorsey (another veteran of the email marketing business), Silicon Valley Bank and Melody Dippold, Union Square Ventures and Fred Wilson, and Costanoa Ventures and Greg Sands. Pretty much a Dream Team if there ever was one.

So how did our team and I get from Email Deliverability to Executive Talent Marketplace?

It’s more straightforward than you’d think. If you know me or Return Path, you know that our company was obsessed with culture, values, people, and leadership development. You know that we created a cool workforce development nonprofit, Path Forward, to help moms who have taken a career break to care raise kids get back to work. You know that I wrote a book for startup CEOs and have spent tons of time over the years mentoring and coaching CEOs. Our team has a passion for helping develop the startup ecosystem, we have a passion for helping people improve and grow their careers and have a positive impact on others, and we have a passion for helping companies have a broad and diverse talent pipeline, especially at the leadership level. Put all those things together and voila – you get Bolster!

There will be much more to come about Bolster and related topics in the weeks and months to come. I’ll cross-post anything I write for the Bolster blog here on OnlyOnce, and maybe occasionally a post from someone else. We have a few opening posts for Bolster that are probably running there today that I’ll post here over the next couple weeks.

If you’re interested in joining Bolster as an executive member or as a client, please go to www.bolster.com and sign up – the site is officially live as of today (although many aspects of the business are still in development, in beta, or manual).

Closer to the Front Lines, Part II

Closer to the Front Lines, II

Last year, I wrote about our sabbatical policy and how I had spent six weeks filling in for George when he was out. I just finished up filling in for Jack (our COO/CFO) while he was out on his. Although for a variety of reasons I wasn’t as deeply engaged with Jack’s team as I was last year with George’s, I did find some great benefits to working more directly with them.

In addition to the ones I wrote about last year, another discovery, or rather, reminder, that I got this time around was that the bigger the company gets and the more specialized skill sets become, there are an increasing number of jobs that I couldn’t step in and do in a pinch. I used to feel this way about all non-technical jobs in the early years of the company, but not so much any more.

Anyway, it’s always a busy time doing two jobs, and probably both jobs suffer a bit in the short term. But it’s a great experience overall for me as a leader. Anita’s sabbatical will also hit in 2010 — is everyone ready for me to run sales for half a quarter?

Symbolism in Action

Symbolism in Action

A couple months ago, I wrote about how the idiots who run the Big 3 US automakers in Detroit don’t have a clue about symbolism — the art or the science of it. Yesterday, I wrote about how I think the non-headcount cuts to G&A that we’re making at Return Path during these challenging economic times will be positive for the company in the long run. The two topics are closely related.

Obama announces on Day 1 that White House staffers who make more than $100k won’t be getting a pay raise this year. Presumably all of those people just started their jobs on January 20 and wouldn’t be eligible for a raise until 2010. Return Path cuts pilates classes in its Colorado office — an expense that must cost around $3,000/year. Practically speaking, it won’t make a difference to our budget one way or another. Microsoft lays off 1,400 people — a real number, certainly for those families — but that’s the equivalent of Return Path laying off 2 people.

Sometimes the symbolic is just that. It is something designed to send a signal to others, and not much more. You could argue that all three examples above mean nothing in reality, so they were just symbolic. A waste of time.

You can also make the argument that sometimes, when done right, symbolism turns into action as it motivates or serves as a catalyst for other changes. Obama’s cuts may be fictitious, but they set the tone for broader action across a 2mm person bureaucracy. Pilates in the office? Feels too excessive these days, even for a company obsessed with its employees and their well being, in an era where we’re cutting back other things that are more serious. Microsoft has gobs of cash and doesn’t need to worry about its future, but it wants to tell the other 99% of its employee population that it’s time to buckle down and fly straight. And they will.

Anyone who thinks the synbolic doesn’t influence the practical should think again. Or just talk to Caroline Kennedy about the impact of her admission that she hadn’t voted in years on her political ambitions.

Understanding the Drivers of Success

Understanding the Drivers of Success

Although generally business is great at Return Path and by almost any standard in the world has been consistently strong over the years, as everyone internally knows, the second part of 2012 and most of 2013 were not our finest years/quarters. We had a number of challenges scaling our business, many of which have since been addressed and improved significantly.

When I step back and reflect on “what went wrong” in the quarters where we came up short of our own expectations, I can come up with lots of specific answers around finer points of execution, and even a few abstracted ones around our industry, solutions, team, and processes. But one interesting answer I came up with recently was that the reason we faltered a bit was that we didn’t clearly understand the drivers of success in our business in the 1-2 years prior to things getting tough. And when I reflect back on our entire 14+ year history, I think that pattern has repeated itself a few times, so I’m going to conclude there’s something to it.

What does that mean? Well, a rising tide — success in your company — papers over a lot of challenges in the business, things that probably aren’t working well that you ignore because the general trend, numbers, and success are there. Similarly, a falling tide — when the going gets a little tough for you — quickly reveals the cracks in the foundation.

In our case, I think that while some of our success in 2010 and 2011 was due to our product, service, team, etc. — there were two other key drivers. One was the massive growth in social media and daily deal sites (huge users of email), which led to more rapid customer acquisition and more rapid customer expansion coupled with less customer churn. The second was the fact that the email filtering environment was undergoing a change, especially at Gmail and Yahoo, which caused more problems and disruption for our clients’ email programs than usual — the sweet spot of our solution.

While of course you always want to make hay while the sun shines, in both of these cases, a more careful analysis, even WHILE WE WERE MAKING HAY, would have led us to the conclusion that both of those trends were not only potentially short-term, but that the end of the trend could be a double negative — both the end of a specific positive (lots of new customers, lots more market need), and the beginning of a BROADER negative (more customer churn, reduced market need).

What are we going to do about this? I am going to more consistently apply one of our learning principles, the Post-Mortem –THE ART OF THE POST-MORTEM, to more general business performance issues instead of specific activities or incidents. But more important, I am going to make sure we do that when things are going well…not just when the going gets tough.

What are the drivers of success in your business? What would happen if they shifted tomorrow?

Please, Keep Not Calling (Thank You!)

Please, Keep Not Calling (Thank You!)

It’s been three years since the federal government passed one of its better pieces of legislation in recent memory, creating the Do Not Call Registry which is a free way of dramatically reducing junk phone solicitations. At the time, registrations were set to expire every three years. When I signed up my phone number, I stuck a note in my calendar for today (three years later) to renew my registration. I was planning on blogging about it to remind the rest of the world, too.

To my great surprise, when I went to the site today, I saw this note:

Your registration will not expire. Telephone numbers placed on the National Do Not Call Registry will remain on it permanently due to the Do-Not-Call Improvement Act of 2007, which became law in February 2008.

That’s two great pieces of legislation. What will they think of next?

Email Intelligence and the new Return Path

Welcome to the new Return Path.

For a tech company to grow and thrive in the 21st century it must be in a state of constant adaptation. We have been the global market leaders in email deliverability since my co-founder George Bilbrey coined that term back in 2002. In fact, back in 2008 we announced a major corporate reorganization, divesting ourselves of some legacy businesses in order to focus on deliverability as our core business.

Since then Return Path has grown tremendously thanks to that focus, but we have grown to the point where it’s time for us to redefine ourselves once again. Now we’re launching a new chapter in the company’s history to meet evolving needs in our marketplace. We’re establishing ourselves as the global market leaders in email intelligence. Read on and I’ll explain what that means and why it’s important.

What Return Path Released Today

We launched three new products today to improve inbox placement rate (the new Inbox Monitor, now including subscriber-level data), identify phishing attacks (Email Brand Monitor), and make it easier to understand subscriber engagement and benchmark your program against your competition (Inbox Insight, a groundbreaking new solution). We’ve also released an important research study conducted by David Daniels at The Relevancy Group.

The report’s findings parallel what we’ve been hearing more and more recently. Email marketers are struggling with two core problems that complicate their decision making: They have access to so much data, they can’t possibly analyze it fast enough or thoroughly enough to benefit from it; and too often they don’t have access to the data they really need.

Meanwhile they face new challenges in addition to the ones email marketers have been battling for years. It’s still hard to get to the inbox, and even to monitor how much mail isn’t getting there. It’s still hard to protect brands and their customers from phishing and spoofing, and even to see when mail streams are under attack. And it’s still hard to see engagement measurements, even as they become more important to marketing performance.

Email Intelligence is the Answer

Our solution to these problems is Email Intelligence. Email intelligence is the combination of data from across the email ecosystem, analytics that make it accessible and manageable, and insight that makes it actionable. Marketers need all of these to understand their email performance beyond deliverability. They need it to benchmark themselves against competitors, to gain a complete understanding of their subscribers’ experience, and to accurately track and report the full impact of their email programs. In fact, we have redefined our company’s mission statement to align with our shift from being the global leader in Email Deliverability to being the global leader in Email Intelligence:

We analyze email data and build solutions that generate insights for senders, mailbox providers, and users to ensure that inboxes contain only messages that users want

The products we are launching today, in combination with the rest of our Email Intelligence Solution for Marketers that’s been serving clients for a decade, will help meet these market needs, but we continue to look ahead to find solutions to bigger problems. I see our evolution into an Email Intelligence company as an opportunity to change the entire ecosystem, to make email better, more welcome, more effective, and more secure.

David’s researchoffers a unique view of marketers’ place in the ecosystem, where they want to get to, how much progress they’ve made, and how big a lead the top competitors have opened up against the rest. (It can also give you a sense of where your efforts stack up vs. the rest of the industry.) There are definitely some surprises, but for me the biggest takeaway was no surprise at all: The factors that separate the leaders are essentially the core components of what we define as Email Intelligence.

The Gift of Feedback, Part II

The Gift of Feedback, Part II

I’ve written a few times over the years about our 360 feedback process at Return Path. In Part I of this series in early 2008, I spelled out my development plan coming out of that year’s 360 live review process. I have my new plan now after this year’s process, and I thought I’d share it once again. This year I have four items to work on:

- Continue to develop the executive team. Manage the team more aggressively and intentionally. Upgrade existing people, push hard on next-level team development, and critically evaluate the organization every 3-6 months to see if the execs are scaling well enough or if they need to replaced or augmented

- Formalize junior staff interaction. Create more intentional feedback loops before/after meetings, including with the staff member if needed, and cultivate acceptance of transparency; get managers to do the same. Be extra skeptical about the feedback I’m getting, realizing that I may not get an accurate or complete picture

- Foster deeper engagement across the entire organization. Simplify/streamline company mission and balanced scorecard through a combination of deeper level maps/scorecards, maybe a higher level scorecard, and constant reinforcing communication. Drive multi-year planning process to be fun, touching the entire company, and culminating in a renewed enthusiasm

- Disrupt early and often, the right way. Introduce an element of productive disruption/creative destruction into the way I lead, noting item 2 around feedback loops

Thanks to everyone internally who contributed to this review. I appreciate your time and input. Onward!

Deals are not done until they are done

We were excited to close the sale of our Consumer Insights business last week to Edison, as I blogged about last week on the Return Path blog. But it brought back to mind the great Yogi Berra quote that “it ain’t over ’til it’s over.”

We’ve done lots of deals over our 18 year existence. Something like 12 or 13 acquisitions and 5 spin-offs or divestitures. And a very large number of equity and debt financings.

We’ve also had four deals that didn’t get done. One was an acquisition we were going to make that we pulled away from during due diligence because we found some things in due diligence that proved our acquisition thesis incorrect. We pulled the plug on that one relatively early. I’m sure it was painful for the target company, but the timing was mid-process, and that is what due diligence is for. One was a financing that we had pretty much ready to go right around the time the markets melted down in late 2008.

But the other two were deals that fell apart when they were literally at the goal line – all legal work done, Boards either approved or lined up to approve, press releases written. One was an acquisition we were planning to make, and the other was a divestiture. Both were horrible experiences. No one likes being left at the altar. The feeling in the moment is terrible, but the clean-up afterwards is tough, too. As one of my board members said at the time of one of these two incidents – “what do you do with all the guests and the food?”

What I learned from these two experiences, and they were very different from each other and also a while back now, is a few things:

- If you’re pulling out of a deal, give the bad news as early as possible, but absolutely give the news. We actually had one of the “fall apart at the goal line” deals where the other party literally didn’t show up for the closing and never returned a phone call after that. Amateur hour at its worst

- When you’re giving the bad news, do it as directly as possible – and offer as much constructive feedback as possible. Life is long, and there’s no reason to completely burn a relationship if you don’t have to

- Use the due diligence and documentation period to regularly pull up and ask if things are still on track. It’s easy in the heat and rapid pace of a deal to lose sight of the original thesis, economic justification, or some internal commitments. The time to remember those is not at the finish line

- Sellers should consider asking for a breakup fee in some situations. This is tough and of course cuts both ways – I wouldn’t want to agree to one as a buyer. But if you get into a process that’s likely to cause damage to your company if it doesn’t go through by virtue of the process itself, it’s a reasonable ask

But mostly, my general rule now is to be skeptical right up until the very last minute.

Because deals are not done until they are done.