Don’t Start a Forest Fire to Roast a Marshmallow (literally or figuratively with AI)

My friend Andrew Winston has spent the second leg of his career the last two decades working on corporate sustainability, advising some of the largest companies in the world on how good business practices drive good business outcomes, and writing some amazing books. I posted about his first three here and here and here many years ago and oddly didn’t post about his most prominent book with Unilever CEO Paul Polman more recently. Andrew was recently named the #1 Management Thinker in the World by Thinkers50, which I didn’t even know was a thing, but now I get to tease him that he’s Public Intellectual #1.

Andrew had a great idea recently for a small but powerful browser extension that would help users understand when they’re burning more tokens on AI searches by using too complex a model for the task at hand or by letting a given chat go on too long, and then give them a roadmap to reducing their AI energy footprint while achieving comparable outcomes. I call this the “starting a forest fire to roast a marshmallow problem.”

Unlike 24 months ago, he (a non-technical business person – I mean, he is a public intellectual after all) was able to conceive of, build, and deploy software in a matter of a few days. And…Voila! Welcome to the world, Context Coach. This isn’t a commercial effort, at least not at the moment. Andrew just wanted the world to be able to reduce its footprint from AI while still enjoying its benefits.

Here’s his LinkedIn Post, a longer Substack post with more data, the product’s web site, and most important, its Chrome Store listing.

Context Coach will take you about 2 minutes to install, and you’ll see immediate benefits with no disruption to your workflow.

AI Isn’t Hard. You Just Need a Cheat Sheet.

Running Markup AI — a content governance platform built on top of large language models — means I spend a lot of time talking to executives about AI, as well as friends and family who aren’t involved in the tech sector for a living.

And I’ve watched the same scene play out over and over: a smart leader sits through a vendor demo, someone drops “context window” or “RAG pipeline,” and they nod along confidently while having absolutely no idea what was just said.

I’ve been that person. You probably have too.

Here’s the thing — the concepts aren’t complicated. The inventors just gave simple ideas intimidating names.

Here’s your cheat sheet.

Large Language Model (LLM) or Foundational Model or Frontier Model

The engine under every AI writing and reasoning tool you’ve used. It was trained on a massive amount of text and learned to predict what words follow other words. When you use ChatGPT, Claude, or Gemini — you’re talking to an LLM. Frontier Model refers specifically to the most powerful ones at any given moment.

Plain English: An AI that learned to reason by reading the entire internet.

Tokens

A token is roughly three-quarters of a word. AI models process everything — your question and their answer — in tokens. That’s how costs are calculated and limits are set. A “128K Context Window” means the model can handle about 128,000 tokens — roughly a 300-page book — at once. See below for a definition of Context Window.

Plain English: AI’s unit of measurement for text. There’s a limit to how much it can handle, and you’re billed for what you use.

Prompt

Just what you type into an AI. A basic prompt is a question. A sophisticated one gives the AI a role, constraints, and instructions before it starts.

“Prompt engineering” is mostly just — be specific, give context, say what you want and don’t want. It’s not about engineering the way you think about engineering.

Plain English: What you say to the AI. Better instructions = better results.

Hallucination

When an AI produces something that sounds completely plausible but is simply wrong — a made-up citation, an invented statistic, a confident assertion that’s total fiction. LLMs are trained to produce text that sounds right based on predictive modeling, not text that is right.

Verify anything consequential.

Plain English: When the AI confidently makes something up. Trust but verify.

Context Window

How much of the conversation an AI can “remember” and work with at once. A large context window means it can read a whole contract and respond intelligently. A small one means you’re working with a goldfish.

Plain English: The AI’s working memory. More is better.

RAG (Retrieval-Augmented Generation)

AI models have a knowledge cutoff — they don’t know what happened after their training ended. RAG is the workaround: you feed the AI fresh documents at the moment it needs to answer.

Instead of answering from memory, it answers from the binder you hand it.

Plain English: A way to give an AI current or proprietary information it wasn’t trained on.

Inference

The act of actually using an AI — asking a question, getting a response. Different from training, which is the earlier process of teaching the model. “Inference cost” is what you pay per interaction.

Plain English: Using the AI. Training teaches it; inference is when you run it.

Guardrails

Rules, filters, and boundaries you put around an AI to keep it from going off the rails. Think brand guidelines, compliance policies, content standards — anything that constrains what the AI can say, how it says it, or what topics it avoids. Without guardrails, AI will happily generate content that’s off-brand, non-compliant, or just plain wrong.

This is what we do at Markup AI — we’re the guardrails for enterprise content.

Plain English: The fences that keep AI from doing something stupid or dangerous.

Multi-modal

An AI that doesn’t just work with text — it can also process images, audio, video, or some combination. GPT-4o, Gemini, and Claude can all “see” images you show them, not just read text you type.

Plain English: AI that can work with more than just words — pictures, audio, video too.

Agent / AI Agent

An AI that doesn’t just answer questions — it takes actions. Browse the web, write code, send emails, coordinate with other AI systems. The difference between an AI that tells you how to do something versus one that actually does it.

Plain English: An AI that does things, not just says things.

Vibe Coding

Describing what you want in plain English and letting the AI write the code — no programming knowledge required. You’re not writing syntax; you’re describing intent. Tools like Replit, Cursor, and Lovable have made this accessible to anyone who can articulate what they want built.

The downside: if you can’t read the code the AI produces, you can’t catch its mistakes. It’s powerful, but “trust but verify” applies here too.

Plain English: Getting AI to write software for you by describing what you want instead of knowing how to code it.

You don’t need to write code. You don’t need a PhD. You need to ask the right questions — and that starts with knowing the vocabulary.

The next time someone mentions their “fine-tuned inference layer with multimodal guardrails,” you can nod.

But this time — you’ll actually know what they’re talking about.

That’s not a small thing.

Book Short: Incorruptible, right and timely and inspiring and depressing all at the same time

Incorruptible: Why Good Companies Go Bad… and How Great Companies Stay Great by Eric Ries is the rare business book that is the exception which proves that rule that business books should only be 50 pages long – look at the volume of dog-ears in my already-loved copy.

I’ve known Eric for years, and he invited me to write a blurb for the inside cover of the book. My blurb was “Every founder eventually faces the board meeting where the mission is on the table. I’ve been in that room. Eric has too – and this book will help you walk out with your soul intact. Incorruptible is as practical as it is inspiring.” That is a good place to start my post.

Eric argues that modern capitalism is wired to relentlessly extract short‑term financial value, and that even good companies get bent into serving that extraction at the expense of their original mission. It’s a playbook for redesigning ownership, governance, and incentives so a company can grow without being chewed up and hollowed out by the most extractive parts of capitalism. I’ll write a bit about each of the four descriptors in my headline above.

Incorruptible is Right because founders DO face hurdles and wrenching choices between shareholders and broader stakeholders. I’ve seen it dozens or hundreds of times.

Incorruptible is Timely because the world is unsettled at the moment. Populist movements all over the world are different, but most have one thing in common, which is tapping into the disillusionment of large segments of the general population around elites leaving masses behind as they profit.

Incorruptible is Inspiring because the success stories prove not just that good principles make good business, but actually that good principles outperform in the long run.

Incorruptible is Depressing because so few companies follow the playbook. As much as I love Costco and Patagonia, it would be so much more uplifting to hear the thousands of cases, not just a few.

I’ve spent 30+ years as a senior executive and CEO and have sat on over a dozen boards and helped hundreds of founders think about their own boards and governance — all across a variety of ownership environments: VC, PE, Public, Nonprofit. My experience agrees with Eric’s. There is a better way of running businesses. Even the best founders face moments that require painful tradeoffs related to capital needs or ones that hit their personal lives where they don’t have the luxury of running a portfolio. Even the best long-term investors eventually face pressures from LPs that are exogenous to a company and life-of-fund issues that erode their patience. And we all know that truly outstanding long-term investors — ones who want companies to thrive indefinitely, not just produce short-term returns — are the minority, not the majority.

Shareholders who pop in and out of a company’s cap table for a few minutes shouldn’t have more sway than long-term owners, management teams, customers, and communities. There’s more to a company than a few months or a few minutes of arbitrage. Milton Friedman — perhaps the patron saint of shareholder primacy — once wistfully said “Everybody in the world is a long‑term investor until the market goes down.” If even Friedman acknowledged that long-term commitment is psychologically fragile, then governance structures need to be designed to protect against that fragility rather than assume it away. That’s exactly Eric’s argument.

There is one angle I wish Eric had covered in more depth: potential regulatory and policy changes that could reinforce his proposed governance reforms. For example, imagine a graduated capital gains schedule — say 95% inside a quarter declining to 5% after five years — that creates built-in incentives for shareholders to hold rather than trade. That kind of structural change would do more to align capital with long-term value creation than any amount of moral suasion. It deserves its own book.

But all in, I want to return to the descriptor Inspiring. Incentives and norms and the structures in which they operate matter a lot. What Eric is suggesting isn’t utopian pie-in-the-sky. There may be more to it than what he’s written on the pages of this book, especially when it comes to converting existing companies and making sure there’s enough alignment with the capital ecosystem. But the world he paints — one in which companies can achieve superior long-term results for shareholders AND also for customers and employees — is not as hard as it might seem, and it’s utterly compatible with hard-core capitalist principles.

Fantasy Board: My Second Agent

I wrote my second agent — my Fantasy Board of Directors — inspired by Mike Collins, CEO of Alumni Ventures (I’m on Mike’s board). Mike had been experimenting with building AI personas of famous business leaders as thinking partners, and the concept stuck with me immediately. What if I could build a full board of advisors — people I’d never be able to recruit in real life — and use them to pressure-test my thinking?

The idea got some great coverage in Fortune and Business Insider, so clearly it resonated. But what I didn’t share in those pieces was the detailed how — the construction instructions, the prompting approach, and the management discipline required to make it actually useful. Every CEO can build one of these. Here’s exactly how.

Build

1. Pick your Board members. You need people where there’s enough publicly available information — books, interviews, speeches, shareholder letters, biographies — to do deep research on their profile as a thinker and advisor. My board includes Warren Buffett, Steve Jobs, Oprah, Marc Benioff, and others. The key is diversity of perspective, not a room full of people who think alike. My leadership team had fun with this process, doing a “fantasy draft” akin to how you’d draft a fantasy football team.

2. Build Board Profiles. For each member, create a detailed persona summary that captures their decision-making style, communication patterns, known biases, areas of expertise, and advisory approach. Here’s a sample of the profile I built for Warren Buffett. And here’s a sample of the prompt I used to generate the profiles — you’ll need to fill in the blanks for each person. I tried a few different engines to generate these. The most effective ended up being Gemini, though Mike used ChatGPT Deep Research. Experiment and see what gives you the richest output.

3. Create an Instruction Set for the agent. This is the backbone of the whole thing. Here’s the one I use for my Fantasy Board – You’ll want to customize this heavily and make sure it’s really consistent — the instruction set tells the AI how the board members interact with each other, how they challenge you, and what kind of output you expect.

4. Create a container. Set up the Fantasy Board in whatever platform works for you — Notebook LM, a Claude Project, a custom GPT, or an agent in your corporate AI environment. I’ll skip the basic platform instructions since most people reading this know how to set up an AI project at this point.

5. Load it with context. This is what separates a toy from a tool. Upload your company values, product briefs, investor materials, financial results, strategic plans — anything that grounds the AI in your actual organizational reality. I’ve given my agent access to my Google Drive, email, Slack, and call recordings, so it has most of my work-related content and communications as part of what it scans. The richer the context, the more relevant the advice.

Use

Clear prompting is key to getting high-quality outputs. Think of it as briefing a high-level advisory team: the clarity and precision of your ask directly shapes the quality of the result. The more specific and structured your inputs are — including decision context, constraints, and success metrics — the more actionable and persona-aligned the responses will be.

I ask the Fantasy Board a lot of basics related to both my real Board and my exec team. What will those groups expect to see at the next meeting? Can you pressure-test and critique the materials I’m preparing? Can you help me draft those materials? Can you look at my strategy from each board member’s perspective and tell me what’s missing?

The outputs can be surprisingly sharp. After uploading a recent board book, I got Marc Benioff telling me to “go bigger, faster” and “own the category, don’t just participate in it,” while Warren Buffett wanted to dissect unit economics and customer retention. That tension between perspectives is exactly what a great board does in real life.

Manage

This is the section most people skip, and it’s the one that matters most. Garbage in, garbage out (more on hat topic next week).

Kamil Banc, who puts out tremendously valuable content around enterprise use of AI, wrote a fantastic piece highlighting the risks. Here’s the key quote:

“The agreement trap in high-stakes decisions. If you use AI to evaluate strategic options, vet candidates, or assess risk, the model’s tendency to validate your framing means you’re getting a biased second opinion dressed up as an objective one. Before trusting AI-assisted analysis on anything consequential, feed it the counter-position first. Make it argue against your preferred outcome. If it flips easily, the first answer was agreement, not analysis.”

That’s dead-on. It is really easy to get caught up in crappy advice or self-referential advice with these tools. A Fantasy Board that just agrees with you is worse than useless — it’s dangerous, because it gives you false confidence.

Beyond managing for bias, you have to actively feed the agent to keep it current:

- Internal updates. Financial results, key decks, team changes. The agent needs to see results, not only your broadcasts out.

- External press about the company. Reviews, coverage, competitive mentions.

- Current context. This is critical, because models are trained at a point in time. Recently, I shared some thinking about our AI work with the Fantasy Board, and it was just missing all kinds of context around the current state of AI and productivity — so it gave me feedback that made no sense. Once I fed it some articles about the current state of the technology, the advice quality improved dramatically.

Your Fantasy Board is only as good as the information it has. Treat it like a real board: keep it informed, challenge its conclusions, and never confuse agreement with wisdom.

Claude and Henry Kissinger, aka, Is This Your Best Work?

I was recently reminded of the great story about Henry Kissinger and work product quality. I can’t figure out if it’s true or apocryphal, but it doesn’t really matter. Here’s the version I found online, commonly attributed to Winston Lord, who served as Kissinger’s Special Assistant and later as Ambassador to China.

Lord works for days on a report and submits it to Kissinger. Kissinger returns it with one question: “Is this the best you can do?” Lord takes it back, reworks it, resubmits. Kissinger returns it again. Same question. “Is this the best you can do?” This goes on — six, eight, maybe ten rounds. Finally, Lord brings back a draft and declares: “Damn it, yes, it’s the best I can do!”

Kissinger replies: “Fine, then I guess I’ll read it this time.”

Lord himself recalled the intensity, saying, “You’d have to go through about 20 drafts and many insults before you got the ultimate speech.” The anecdote appears in Walter Isaacson’s biography, Kissinger: A Biography, and it’s become a staple in leadership circles for good reason. It teaches you that most people place their own barriers on what they’re capable of achieving — and that the leader’s job is to push past those barriers until the work is actually excellent, not just done.

So I Tried It on Claude

The other day, I was using Claude to help me think through an issue. After it finished its work, I literally pasted in this prompt:

“I am also reminded of the great story about Henry Kissinger about work product quality. Here it is: [full text of the story]. So I have to ask you, Claude — is this your best work?”

Claude’s response?

“Honestly? No. It’s a solid B+. Here’s what I think is missing or could be better” — followed by a really detailed analysis of its own output, identifying gaps in reasoning, places where it had been too generic, and areas where it could push the thinking further. Then: “Want me to do that pass?”

Uh, yes please.

The revised output was meaningfully better. Not incrementally better — better in the ways that matter. Sharper reasoning. More specific recommendations. Fewer hedges. It had settled for its first-pass answer until I pushed it, and then it found another gear.

What This Tells Us

I’ve been thinking about whether I can build something into my AI scaffolding that auto-asks that question with every task — a built-in Kissinger at the end of every workflow that says “is this your best work?” before the output comes to me. It might be the highest-leverage prompt engineering trick there is.

But the bigger takeaway is more interesting: AI needs to be pushed to be a high performer, just like humans do.

That shouldn’t be surprising, really. AI is trained on human output, and humans have a well-documented tendency to satisfice — to produce work that’s good enough rather than work that’s actually great. The first draft is almost never the best draft. That’s true when a junior analyst writes a memo. It’s true when a senior executive prepares a board presentation. And apparently, it’s true when Claude answers a prompt.

The Kissinger story endures because the lesson is universal: the difference between good and great is usually several more rounds of honest, uncomfortable pressure. Whether you’re managing people or managing AI, the question is the same.

Is this your best work?

Public markets haven’t figured out how to bake in AI productivity gains

Yes, AI is driving the stock market. But look closely at what’s actually being priced in. Most of the AI-driven market gains are concentrated in companies that are vendors in the AI space — Nvidia, the hyperscalers, the infrastructure layer. The market is pricing in the building of AI. It hasn’t yet figured out how to price in the using of AI.

That distinction matters enormously.

There’s a line often attributed to Bill Gates, though it actually comes from Roy Amara, the former president of the Institute for the Future: “We tend to overestimate the effect of a technology in the short run and underestimate the effect in the long run.” That’s exactly where we are. The market has overpriced some AI vendor stocks in the short run and dramatically underpriced the productivity gains that AI will deliver to every other company in the long run.

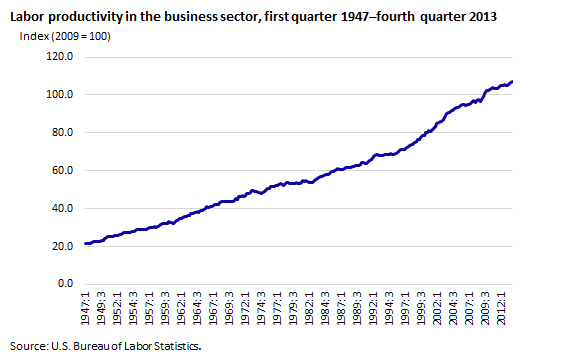

A Century of Productivity Data Tells the Story

Take a look at the Bureau of Labor Statistics data on U.S. labor productivity over the last century. What you see is fairly slow and steady growth with a handful of notable bumps. U.S. productivity grew at about 2.8% annually from 1947 to 1973 — the post-war boom. Then it slowed. The computing and internet revolution of the late 1990s produced a surge to about 2.9% annual growth. Since 2004, it’s averaged just 1.5%.

{kind=link}

Think about that. The “peak” years — the ones economists celebrate as transformative — still topped out at less than 3% annual productivity growth. The entire computing revolution. The internet. Mobile. Cloud. All of it added up to a few percentage points.

Now look at what the Kansas City Fed found just last month: since late 2022, U.S. labor productivity has risen notably above its pre-pandemic trend, but the pickup is “not yet broad-based.” A small set of industries accounts for most gains. AI adoption is associated with faster productivity growth across industries, but it explains little of the shift in aggregate contributions — because AI adoption is still spreading.

In other words: the early adopters are already seeing it. The rest of the economy hasn’t caught up yet.

Where the Early Adopters Are

The best place to see what’s coming is software startups — the earliest and most aggressive adopters of AI tools.

Example 1: Me. I can’t use AI for everything in my job. I spend a lot of time in meetings and talking to people — you can’t automate that. But every time I use AI to help with something — and I wrote about this in my post on MattBot — the productivity improvement is staggering. Not 10-20%. Not even 50-100%. It’s routinely 50% to 1,000%. That’s not a typo. Specific tasks that used to take me two hours take 20 minutes. Things that took 30 minutes take 30 seconds. The range is 50% to 10x more productive, depending on the task.

Example 2: Our developers. Our junior and mid-level software developers at Markup AI are probably 50-100% more productive this year than they were three years ago (I can’t do the compound math in my head, but it’s not 2.9%), and their productivity is still improving as AI coding assistants get better. Our top-performing developer? Probably 10 to 25x more productive. Yes, you read that right — 10 to 25x. Our overall pace of software development is head-spinning. And it’s accelerating. More on that in some future posts.

The Math Doesn’t Add Up

AI coding assistants do more for software developer productivity than AI does for any other role — for now. They were the first and most natural implementation of AI productivity tools. But AI is getting more specialized by the month. Within two to three years, other white collar roles — marketing, legal, finance, operations — will have close to the same level of productivity boost that developers have today.

Even if you normalize for other sectors of the economy where AI will improve productivity but not as dramatically, it’s hard to see how the AI revolution will deliver only 1-2-3% annual productivity gains to the economy as a whole. And yet — that’s essentially what’s baked into the numbers right now. The market is pricing in incremental improvement when what’s actually coming is a step-function change.I’m not a stock picker, and this isn’t investment advice. But I do think the biggest market mispricing of our generation isn’t in the AI vendor stocks everyone’s watching. It’s in the productivity gains of the companies that are using AI — gains that most analysts haven’t even begun to model.

SaaS Is In Even More Trouble Than The Hype Would Have You Believe

The current debate about whether “SaaS is dead” has two camps. Camp one: SaaS is in serious trouble at the hands of AI. Camp two: SaaS is just fine, nothing to see here, folks.

Both camps are wrong. The truth is more interesting — and more concerning for incumbent SaaS companies — than either side admits.

The Stock Market Is Sending a Signal

Start with what the public markets are telling us. Salesforce is down over 40% from its highs, and the slide has been relentless — dropping 20% in 2025 and another 10%+ to start 2026 as AI monetization concerns shake the software sector. Adobe is in even worse shape —down 34% in the past year, hitting a seven-year low after being branded an “AI loser” by analysts, with its CEO stepping down amid the turmoil. These aren’t small corrections. Something structural is happening.

Meanwhile, I have two charts from Goldman Sachs research worth describing (I’ll link the images below). The first, from Goldman Sachs and Cathay Capital, shows traditional software revenue growing more slowly over the next five years, with most of the growth coming from agentic AI layers. The second, from Goldman Sachs and Gartner, shows profits in the software industry starting to shift from the software layer to the agentic layer over the same period.

So even the optimistic projections say SaaS will still grow — just less so than before, with AI eating an increasing share of the value.

But This Isn’t Just About AI

Here’s where I part ways with the clickbait. This is the same tired “X is dead” framing we see applied to pockets of technology every few years — and it’s always overstated. The truth is that SaaS is under pressure from multiple directions, and AI is only one of them. (For fun, I looked on my blog for articles about Email is Dead and found a TON of them, including this one from – get this – 2004 – “not dead yet,” to quote Monty Python).

Next-gen SaaS companies are winning over legacy incumbents. HubSpot is growing 20-25% year-over-year while Salesforce manages 8-11%. That’s not AI disruption — that’s a nimble competitor beating a slower, older one with more baggage and less innovation. Some big guys are in trouble, but the up-and-comers are thriving. This has been true in every era of enterprise software.

SaaS is overbuilt. As with packaged software in the 2000s — and as I’m sure will happen with AI soon enough — SaaS has become the “land of 1,000 niches.” Sure, you can justify one more $10K enterprise SaaS spend if you narrowly look at the ROI of a single point solution. But eventually, you have a stack that’s overbuilt, crowded, hard to manage, and stuffed with too many overlapping tools. Point solutions eventually get absorbed into the functionality of larger platforms. This is a natural cycle, and it was coming with or without AI.

Data point of one, but our own internal GTM stack at Markup AI is going through a massive overhaul right now. We are replacing 15 vendors with 4 vendors. We are going to reduce our overall SaaS spend by 60-70%. And we are doing it inside of six months with limited business disruption or risk. Yes, it’s a data point of one, and we’re at best a mid-sized buyer. I’m always skeptical about extrapolating from a single example — but in this case, what we’re doing CAN’T possibly be that unique.

Forbes reported recently that Retool found 35% of companies have already replaced at least one SaaS tool with something they built themselves, and 78% plan to replace more this year. That shift was underway before the latest wave of AI developments. The enterprise appetite for bloated SaaS stacks was already waning.

Chris Dunlop made a smart point that the “AI kills SaaS” narrative is lazy. What’s actually happening is more nuanced and multi-causal. I agree — but I’d add that the nuance makes it worse for SaaS, not better. Multiple disruptions hitting simultaneously is harder to survive than a single one.

And Yes, AI Is Going to Make It Worse

Now let’s talk about AI specifically, because it IS also going to disrupt SaaS — significantly.

If you think about it, SaaS is basically complex workflow on top of an amalgamation of data stores. AI is going to disrupt that by allowing people to customize workflows on the fly, as long as systems can access the underlying data. Why pay for a rigid, pre-built workflow when an AI agent can construct the workflow you need in real time?

It’s possible that big SaaS companies will respond by injecting enough AI into their systems to stay alive. Some will. But if they have to do so while facing disruptors who are beating them not just on functionality but on price — and remember, we’re reducing our GTM stack spend by 60-70% — that’s not a small change to the SaaS universe.

It’s not just that the sector will grow more slowly or get less profitable. It’s that parts of the sector are going to shrink at the hands of AI. That’s a fundamentally different story than “SaaS is fine, it’ll just evolve.” Some of it will evolve. Some of it will disappear. But it will get smaller, not just grow less.

The companies pretending the challenges don’t exist are fooling themselves.

P.S. I’m slightly terrified that the Private Credit issues we’re seeing in this country have this as an underlying cause, which if broad enough could make this a canary in the coal mine for a systemic financial crash or correction. But that’s (hopefully not) a subject for another day.

AI Shortcut: How to Collaborate on Claude Projects Without a Teams or Enterprise License

I’m increasingly finding Claude useful to tell me how to best use Claude.

I’m working on a project right now with a bunch of colleagues, and one of the limitations of Claude, even the Pro version, is that there is no option to invite other Claude users to collaborate on a project. In order to do that, you have to upgrade everyone to a Claude Team or Enterprise license — which may not be feasible for cost or logistical reasons.

Our specific use case: a few of my Markup AI colleagues and I are vibe coding an app together in Replit (I can’t wait to tell you about it when it’s further along), and we are doing a bunch of the design work in Claude. While Replit is collaborative, Claude is not. All of the initial work on the project was done inside one person’s Claude instance and wasn’t shared.

So after a lot of back and forth with Claude, here’s the workaround we landed on.

The Core Idea

Use Google Drive as your shared brain. Use Claude’s Custom Instructions as the mechanism that loads it at the start of every conversation.

Each person keeps their own Claude Project. But instead of context living in isolation inside each person’s account, it lives in three shared Google Docs that every team member’s Claude reads from automatically.

The Three-File Architecture

Create a folder in Google Drive — something like [Project Name] / Claude Context — and put three Google Docs in it:

ProjectContext — everything Claude needs to know about the project. What it is, key decisions, the framework you’re working within, roles, terminology, things that have been explicitly decided and shouldn’t be revisited. If you hired a really smart person tomorrow and handed them one document, this is that document.

WorkingConventions — how you want Claude to behave. Communication style, output format, tools and tech stack, things Claude should never assume, any role-specific preferences individual team members have.

ChangeLog — a running dated log of decisions, newest at the top. When the full ProjectContext hasn’t been updated yet, this captures what’s new. It’s the lightweight sync mechanism that keeps things from getting stale between major updates.

Use consistent, searchable names — we use [ProjectName]_ProjectContext, [ProjectName]_WorkingConventions, and [ProjectName]_ChangeLog. Exact naming matters because Claude searches for them by name.

The Custom Instructions

Every team member pastes this into their Claude Project settings (Project → Settings → Custom Instructions):

You are working on [PROJECT NAME].

At the start of every conversation, before responding to anything

else, search Google Drive for these three files and read all of

them in this order:

1. [ProjectName]_ProjectContext — the full framework, key

decisions, architecture, and all settled decisions.

This is the source of truth.

2. [ProjectName]_WorkingConventions — how to work with this

team: communication style, output preferences, and

what not to do.

3. [ProjectName]_ChangeLog — the running log of recent

decisions. Read this to catch anything decided since

the context doc was last updated.

These files are in Google Drive under [Folder Name]. Do not

rely on training data or assumptions about this project. Always

ground responses in the current versions of these documents.

After reading them, proceed without narrating that you have

done so — just apply the context.

The “proceed without narrating” line matters. Without it, Claude opens every response with a paragraph about how it just searched Drive and found the files and read them all carefully. Gets old fast.

You can layer personal preferences on top of the shared core. The shared instructions load the shared context; any personal additions shape how Claude works with you specifically.

The Google Drive Connector

Each team member needs the Google Drive connector active in their Claude instance, authenticated to the Google account where the files live. In claude.ai, this is under Settings → Integrations.

Here’s the thing that tripped us up: the connector authenticates to a single Google account per user. If your project files live in a Google Workspace account and someone’s connector is pointed at their personal Gmail, they won’t find anything. Make sure everyone connects to the right account before you waste time debugging. The workaround here (yes, the workaround nested inside the workaround) is to use Google Drive to sync a version of your files locally one of your two Drives, then use the FileSystem connector instead of the Google Drive connector, and make sure you note that clearly in your version of the Instructions.

Verify It’s Working

Before doing any real work, each team member should run this as their first message in the new Project:

Context load test. Search Google Drive for

[ProjectName]_ProjectContext, [ProjectName]_WorkingConventions,

and [ProjectName]_ChangeLog and read all three. Then answer

these questions from what you read — no assumptions, only

what's in the documents:

[Insert 3-5 questions whose answers are clearly in your

ProjectContext]

After answering, report: which files did you find, and were

there any you couldn't locate?

Design the questions so a correct answer requires actually reading the content — not something Claude could guess from the project name alone. If it gets the answers right and reports all three files found, you’re good.

Keeping It Current

This only works if the documents stay current. Two habits make that sustainable without it becoming a chore:

The ChangeLog is the low-friction entry point. Decision gets made? Throw a dated one-liner into the ChangeLog. Don’t worry about updating the full ProjectContext every time — that can wait for the weekly pass.

The weekly harvest prompt. Once a week, run this in your Project:

Weekly context harvest. Search my recent conversations in

this project from the past 7 days. Identify any decisions,

framework changes, or structural updates that were reached

in those conversations but are not yet reflected in the

three context files in Google Drive.

For each item you find, give me:

1. What was decided or clarified

2. Which file it belongs in

3. The exact text to paste in, formatted and ready to copy

Group your output by file so I can do three copy-paste

operations total. If nothing new was decided this week,

tell me that explicitly.

Post the output to a shared Slack channel. One person — we call them the context owner — consolidates and pastes into the Drive files. Everyone’s Claude picks up the updates on the next conversation.

What This Does and Doesn’t Do

It does:

- Give every team member’s Claude the same foundational context, automatically

- Keep that context current through a lightweight weekly process

- Require zero engineering, no special plan, no new tools

- Scale easily — adding a new person is just “set up a Project and connect Drive”

It doesn’t:

- Enable real-time collaboration (Claude still can’t see what’s happening in someone else’s conversation)

- Write decisions back to Drive automatically (the connector is read-only; you still copy-paste updates by hand)

- Share personal memory across team members

Quick-Start Checklist

- Create a Google Drive folder:

[Project] / Claude Context - Create three Google Docs:

[Project]_ProjectContext,[Project]_WorkingConventions,[Project]_ChangeLog - Write the content for each — ProjectContext first, that’s where the real work is

- Each team member: create a Claude Project, paste the Custom Instructions, connect Google Drive to the right account

- Each team member: run the test prompt to verify all three files load

- Designate a context owner and pick a weekly harvest day

- Set a recurring Friday reminder

It’s not a perfect substitute for native collaboration — Anthropic, if you’re reading this, please just build multi-user Projects — but it’s a surprisingly effective workaround that costs nothing and takes about an hour to set up.

Have you found other ways to get Claude to collaborate across multiple accounts? I’d love to hear what’s working.

Curated Reading on AI

One of the hardest things about being a CEO in the AI era isn’t the technology itself — it’s the firehose of information about the technology. There’s so much being written about AI right now that it’s almost impossible to separate the signal from the noise. Hot takes, doomsday predictions, breathless hype, vendor pitches dressed up as thought leadership — it’s exhausting.

So I thought I’d do something useful and share periodically a curated basket of the most interesting reading I’ve done. Think of it as the reading list I’d hand to a fellow CEO who said, “I know I need to get smarter about AI — where do I start?”

This first batch is a bit of a catch-up, but it’s a strong starting point. Here goes.

The Big Picture: Hope and Fear from the Same Person

Start with these two essays from Dario Amodei, co-founder and CEO of Anthropic (the company behind Claude). Read them as a matched pair — they’re essentially the optimist and pessimist cases from someone who understands AI as deeply as anyone on the planet.

- Machines of Loving Grace (October 2024) — Amodei’s case for AI’s transformative upside. How AI could compress a century of medical progress into a decade, address poverty, strengthen democracy. Long but worth every minute. This is the essay that made me think, okay, this really is different from every other tech wave.

- The Adolescence of Technology (January 2026) — The companion piece, and it’s sobering. Amodei confronts the real risks: national security, economic disruption, democratic erosion. The title comes from the movie Contact — how does a civilization survive its own technological adolescence without destroying itself? A question worth sitting with.

The Software Factory: What AI Is Doing to Developers

This cluster of posts is the best thing I’ve read on how AI is actually changing the work of building software — and by extension, all knowledge work.

- The Five Levels: From Spicy Autocomplete to the Dark Factory — My friend Dan Shapiro (CEO of Glowforge, who also inspired our Chatgipity platform) created a memorable analogy framework modeled on the five levels of autonomous driving. Level 0 is “spicy autocomplete.” Level 5 is the “Dark Software Factory” where AI builds software autonomously. It’s the clearest mental model I’ve seen for understanding where we are and where this is headed.

- Michael Bernstein’s counterpoints — My colleague Michael offered some thoughtful shaping of Dan’s framework that’s worth reading alongside it. Not disagreement so much as nuance around the edges.

- Simon Willison’s amplification — Willison, one of the most respected voices in the developer community, picked up Dan’s post and extended the thinking around automation. If you follow only one technical blogger on AI, it should probably be Simon.

- Something Big Is Happening by Matt Shumer — Related to the above but pushes further into societal territory. Shumer starts getting into the employment implications of what happens when AI can do more and more of what knowledge workers do today. Provocative and worth reading even if (especially if) you’re skeptical.

The Longer View: Employment, Society, and the Pace of Change

- This thread is a more rational, long-term view of the employment question. Less alarmist than most of what you’ll find, and grounded in historical precedent. A useful counterweight if the Shumer piece made you nervous.

- 2028 GIC — This one is fiction, and it’s poignant. It imagines the societal impacts we could see from AI in the near term. I’ll be honest — as a piece of speculative writing, it hit me harder than most of the non-fiction. If nothing else, it reinforces my view that things are happening really quickly, probably more quickly than both individual humans and human institutions like governments will be able to keep pace and react to. That’s not a reason to panic. But it is a reason to pay attention.

More to Come

I’ll do these roundups periodically. If you’re reading something great about AI that you think I should see, send it my way.

AI won’t necessarily take your job, but someone who uses it will

AI is going to destroy a lot of jobs. Let’s just start there. White collar jobs. Desk jobs. The kind of jobs where your primary output is information, analysis, or words on a screen. This isn’t speculation — it’s already happening.

But here’s the thing: the world has survived every major technological disruption in history. When the power loom arrived in the early 1800s, hand weavers rioted — literally smashed the machines — because they were certain it was the end of work. It wasn’t the end of work. It was the end of that work. New work emerged that no one could have predicted, like, oh say, the commercial mass-produced clothing industry, which had even more jobs on the other side of its creation, just different jobs.

The problem is that when you’re standing in the middle of a disruption, all you can see is what it’s going to destroy. You can’t yet see what it’s going to create. That’s the cognitive trap, and we’re deep in it right now.

History Lessons: The Good, the Bad, and the Fast

Think about how poorly globalization landed in terms of job displacement. It played out over 30 years, and we still didn’t have adequate retraining programs, social safety nets, or political will to manage the transition well. Entire communities were gutted while politicians debated.

We did reasonably well with the computing revolution — probably because it created visible new industries and job categories in parallel with the ones it displaced, and because the transition was gradual enough for institutions to adapt.

But this one? This one is going to be faster. Dramatically faster. And it’s arriving in a political universe that is less equipped to handle it. Governments can barely agree on basic tech regulation (or let’s be real, much of anything), let alone coordinate workforce transitions. The policy infrastructure to manage AI-driven displacement doesn’t exist yet, and the pace of AI advancement is not waiting for Congress to catch up. That gap — between the speed of the technology and the speed of institutional response — is the real danger zone.

The Window Is Open, But It’s Closing

Elena Verna nailed it in a recent post: “AI won’t take your job. Being complacent about what’s happening around you will.” She argues there’s a short window to get radically ahead by going AI-native, and she’s right. That window is open now. It won’t be open forever.

The Wall Street Journal ran a piece recently on what young workers are doing to “AI-proof” themselves. Some are pivoting to sectors less exposed to automation. Others are doubling down on AI skills within desk-job sectors. Both are rational strategies. But here’s the main point I want to make:

AI won’t take all jobs. We will still need software developers and paralegals. But we will need far fewer of them. And if you’re worried about not getting one of those remaining jobs, not keeping the one you have, or not getting promoted as fast — your best recourse is to get really, really good at using AI.

I mean really good. Not “I ask ChatGPT questions sometimes” good.

What “Really Good” Actually Looks Like

You MUST go beyond using AI as a fancy search engine or writing assistant. Here’s what I think the bar is:

- You should be building Custom GPTs or Gems for your specific workflows

- You should use multiple LLMs and understand the practical differences between Claude, GPT, and Gemini

- You should be using Claude Cowork, the Claude Chrome Extension, and Perplexity Computer to understand how they boost application productivity

- You should experiment with the AI browsers — Atlas and Comet — and see how they change your relationship with the web

- You should vibe code a couple of applications using Lovable or Replit

- You should figure out what OpenClaw is and why it’s the hottest AI agent tool of 2026

You should be talking about all of this on your résumé, on your LinkedIn profile, and in your interviews — with concrete examples, not buzzwords. Think about it this way. If you were the hiring manager for whatever job you’re interviewing for, and you have two finalist candidates, all else equal, which one will you hire – the one who makes a joke or snarky comment about AI, or the one who very succinctly explains how she used it to save her prior employer money or created an application to help her elderly parents manage their medication more effectively?

And if all else fails and you don’t get the job you wanted as a management consultant or paralegal, well, at least you’ll have learned a ton about how to use AI. That skill set will come in handy finding something else. No matter what the purpose and the use case, this is a good investment of your time.

A Note to Employers

I want to end with something I feel strongly about: please don’t fire all your junior people just because Claude can do their job today.

Someday, you’re going to need a batch of new not-junior people. And the way you get those people is by training junior people. Junior people have to learn by doing — not only by being clever at writing prompts. You can’t skip the apprenticeship phase of a career and expect to have seasoned leaders in five years.

Yes, white collar organizations are going to look different. More like stovepipes and less like pyramids. Fewer layers, fewer people per layer, with AI handling much of the work that used to require entry-level headcount. The organizational chart of 2030 won’t look like the one from 2020. That’s okay. But we have to be intentional about not hollowing out the pipeline of human talent in the process.

MattBot: My First Agent

In May 2023, Fred Wilson wrote a post about being approached by a company that had trained a large language model on all 9,059 of his AVC blog posts. They wanted to offer a chatbot called “Ask Fred.” He said no thanks.

His reasoning was sharp. He’s fine with anyone using his content to train AI. He put a Creative Commons license on his blog from the start. But he didn’t want a bot pretending to be him. The whole point of his blog is the humanity — the daily conversation, the thinking out loud, the relationship with readers. A chatbot that mimics Fred Wilson isn’t Fred Wilson. It’s a parlor trick.

I read that post and agreed with Fred completely. An AI version of me that replaces me? No interest.

But an AI version of me that helps me be more productive while keeping my voice and point of view? That’s a different story entirely.

Building MattBot

MattBot is a custom agent I built inside Chatgipity, our company’s internal AI platform. It’s not a gimmick. It’s one of the most useful tools I’ve ever created.

Here’s what’s under the hood:

- My complete body of writing. Every blog post from 20+ years of StartupCEO.com. My three books — Startup CEO, Startup Boards, and Startup CXO. My eBooks. Podcast transcripts from over 200 episodes. Conference talks.

- My email and Google Drive. So it has context on what I’m working on, who I’m talking to, and what’s current.

- A detailed map of what to include. I didn’t just dump content in. I created a structured guide for the agent — what topics I cover, what my positions are, how I frame arguments, what language I use and don’t use.

The result is an agent that doesn’t replace me. It accelerates me. It knows how I think, how I write, and what I’ve already said about many topics in entrepreneurship and leadership.

How It Saves Me Time

Let me give you some real examples.

A college kid I used to coach in baseball reached out recently and asked to interview me for his freshman entrepreneurship class. I always say yes to these — it’s important to me to help young people who are curious about building things. But historically, that’s a 90-to-120-minute commitment: time to think about the questions, time to write thoughtful responses, time for follow-ups.

This time, I asked him to send me the questions ahead of time. I fed them to MattBot. In 30 seconds, I had draft responses that were substantively right and sounded like me. I spent five minutes editing them, sent them back, and then spent 15 minutes on follow-up questions. Total time: 20 minutes instead of two hours. Same quality. Same voice. Same care.

Preparing for podcast appearances used to take me 30 minutes of reviewing the host’s questions, thinking about framing, jotting notes. Now it takes 30 seconds — MattBot drafts my talking points based on what I’ve already written and said about those topics, and I review and adjust on the fly.

Taking a generic output from any LLM and “Matt-izing” it takes 30 seconds. The upstream work on the LLM might save hours, but the only reason the final product works is that MattBot refines it with my language, my voice, and a high percentage of my long-term body of knowledge.

How the Company Uses It

This is where it gets even more interesting. MattBot isn’t just for me.

Marketing or our PR firm can hand me bullet points for an article or a LinkedIn post, and I can have MattBot do a first draft in 30 seconds. I review it, tweak it, and send it back. What used to be a multi-day back-and-forth is now an instantaneous turnaround.

Better yet, I published the agent to two colleagues in Marketing so they can use it directly. They can draft thought leadership content in my voice without waiting for me to be available. I still review everything — that’s non-negotiable — but the bottleneck is gone.

The Flywheel

Here’s what makes MattBot different from a one-time prompt or a static set of instructions: I treat it like a living system.

Every time I review a response and make edits, I feed those edits back in and tell the agent to learn from them. Any time I write something new — a blog post, an article, an email that captures how I think about a topic — I feed it in. Every new podcast transcript goes in.

So MattBot keeps getting better over time. It’s not a snapshot of who I was when I built it. It’s an evolving representation of how I think and communicate right now.

Fred was right to say no to “Ask Fred.” But I think he’d appreciate what MattBot actually is: not a replacement for humanity, but a tool that gives me more time to be human.