I love stealing/borrowing other people’s good ideas for management and leadership when they’re made public, and I always encourage others to do so from me. I call it “plagiarizing with pride.” So I was intrigued when I saw a new way of doing all-hands meetings published by my friend Daniel Odio (DROdio) on his founder community called FounderCulture. You can see the original post here.

We’ve experimented with different formats and cadences for all-hands meetings over the years. They tend to vary with the size of the company and complexity of the material to cover. Larger companies usually fall into the rhythm of doing quarterly all-hands meetings sometime after the end of the quarter, usually around a Board meeting, with a quarterly recap and forecast for next quarter.

But for early stage companies, there’s no tried-and-true method. We struggled with that for a while at Bolster. Weekly felt too much. Quarterly felt like too little. It seemed weird for me or my co-founders to just have a meeting where we talked at everyone…and it also seemed weird to just host an “open mic night” type meeting. Then I saw DROdio’s video, and we adapted it. It’s working pretty well for us. Here’s what we do in what we’re calling our Open All-Hands Meeting:

We hold an all-hands meeting every Monday for :30

A different team member is responsible for being the host/chair/emcee for each meeting

We run the meeting off of a dedicated Trello board with specific columns of information. Everyone is invited to contribute to the Trello board in the days leading up to the meeting. The columns are:

Values-Kudos-Good News: Anyone can call out anyone for doing something that demonstrates one of the company’s values, that is just a big thank you, or that is some other piece of karmic goodness they want to share

Wins: All client wins are shown here with some detail, each in its own card with its owner highlighted

#MAD: This is where we trade items on which we Made A Decision during the prior week, big or small. We’ve always struggled with the best way to keep everyone informed on things like this…and this works really well for that purpose

Learnings/Product Ideas: Anyone can populate this with anything they want as they go about their work and either come across learnings or product ideas they want to share

Announcements: Pretty self-explanatory, any corporate announcement, new employee introductions, etc.

Swim Lane Updates: Each we, we ask one or two of our functional or project areas to do a deep dive update — Product, Finance, Sales, Marketing, Ops, etc. — and this is also where we’ll do product demos of newly released functionality

Permanent Items: this isn’t a column that’s read…it just warehouses things we want on the board like the schedule of hosts, schedule of swim lane updates, instructions for running the meeting, recordings of prior meetings

BOLSTER 2022: this isn’t a column that’s read…it contains our mission, values, strategy, and key strategic initiatives and metrics for the year

Archive: this isn’t a column that’s read…it just contains the prior week’s items

There’s a series of light integrations between Slack, Hubspot, and Trello to automatically populate Trello based on certain channels, keywords, and emojis. Every week, the board is automatically wiped clean after the meeting

The host moves the meeting from column to column and card to card, sometimes reading the cards, and sometimes asking the person who submitted the card to read it or give color commentary on it

I do jump in from time to time, as do some of my co-founders or our other leaders, to give extra commentary or amplify something or help connect the dots. But that’s about as formal as my role gets other than…

…when we do have a quarterly board book and board meeting, I host that one meeting and recap the meeting, ask other leaders to comment on specific topics, and facilitate Q&A on the materials we send out ahead of time. So I’m hosting 4 meetings per year

The host can add a personal touch to any meeting. Custom wallpaper for the Trello board. Asking everyone in the company who has a pet to send in a photo of the pet ahead of time and introducing their furry friends during the meeting. Playing intro or outro music to fit the occasion. Doing spot surveys or game show questions to keep things lively. Interviewing new team members. Asking everyone to do a one-sentence “here’s what I’m working on this week” at the end of the meeting

Finally, the host passes the baton from one person to the next each week. No one can escape this responsibility!

In addition to the Open All-Hands Meeting format, I send the company an email every Friday with some musings on the prior week. The content of these varies widely – from “what I did last week,” to “here’s something I saw that’s interesting,” to welcoming new team members with their bios, to customer testimonials. Sometimes other founders write these. They’re a good way to add a personal touch to the operating system of the company — and we also send these to our board and major shareholders every week so they, too, can keep a finger on the pulse.

These two things together are proving to be a good Operating System for keeping everyone informed, aligned, and connected on a weekly basis.

(This blog post was first published as an article in Entrepreneur Magazine on April 15.)

Creating strong boards can help propel a board forward. Weak and ineffective boards hold a company back.

As a CEO, one of the most important (yet overlooked) tools in the playbook is building and leading a board of directors. Throughout my 20+ years of entrepreneurship, I’ve led four companies (including Bolster, where I’m a co-founder and CEO today) and served on eight boards. I’ve learned that strong boards can help propel a company forward and I’ve also witnessed how weak and ineffective boards can hold companies back. Mediocre or mismanaged advice, plus lack of accountability, can do long-term damage to a business as well.

Drawing from personal experience and anecdotes from dozens of Bolster’s client CEOs, here are some tried and true “Seven Habits of Highly Effective Boards.”

Habit 1: Begin with the board in mind

A lot of CEOs treat board curation as an afterthought, which means that boards tend to consist largely of who happened to be in their network at the company’s inception: investors. CEOs also tend to treat their boards as a distraction or an annoyance. Both of these lines of thought are problematic.

Boards should be viewed as a CEO’s second team (along with their management team), as a strategic weapon that helps the company succeed and as an opportunity to bring new voices and perspectives. Research has shown the more independent and diverse a board is, the better it performs.

Habit 2: Be proactive about board recruiting

Devote as much focus to building a board as to building the executive team. This process is time-consuming and can’t be delegated to anyone else. Aspire to reach people who may feel out of reach. Asking someone to join the board is a big honor, so that ask becomes a good calling card. When recruiting, interview as many contenders as possible, don’t be afraid to reject those who aren’t a good fit and have finalists audition by attending a board meeting. Source broadly, too. Diversity is really important for many reasons; challenge any recruiter, agency or platform to surface diverse board candidates.

Habit 3: Keep your board balanced using the Rule of 1s

Whether it’s a three-person startup board or a seven-person scale-up board, it should include representation from all three director types: investors, management directors and independents. A few basic principles on board composition that work well are what I call the Rule of 1s: First, boards should include one, and only one member of the management team: the CEO. Even if co-founders or C-level managers are shareholders, don’t burn a board seat for a perspective that you have access to regularly. Second, for every new investor to the board, add one independent director, which is the biggest opportunity to introduce external perspectives. If your board gets too crowded with subsequent funding rounds, ask one or more investors to take observer seats to make space for independents. And don’t be afraid to change your board composition over time. Companies are dynamic and boards should be, too.

Habit 4: Cultivate mutual accountability and respect

While a board might seem intimidating, work past the power dynamic and push toward collaboration and mutual accountability. To ensure board members are prepared for meetings, keep commitments and leverage their networks, set the example by demonstrating preparation, consistency and reliability. By regularly delivering pre-read materials to the board several days in advance, the board will build a new habit. By soliciting feedback from board members after each meeting (and even offering them feedback), you’ll show the board that you’re listening. Over time, they’ll lean in, too.

Habit 5: Drive intellectually honest discussions

Even on the healthiest leadership teams, it can be scary to disagree with or challenge a sitting CEO (after all, they are still the one in charge!). But this power dynamic flips in a boardroom, which gives that group a unique opportunity to push and challenge business assumptions. While it may be tempting to look for board members with softer dispositions, it can be more beneficial to have tough, direct board members who aren’t afraid to express their opinions, but who are also good listeners and learners. My favorite discussions are conversations where I’m pushed to consider a different direction. It helps get more done, surfaces better ideas and increases the effectiveness of the company.

Habit 6: Lean in on strategic, lean out on tactics

Even board members who are talented operators have a hard time parachuting into any given situation and being super useful. Getting operational help requires a lot of regular engagement on a specific issue or area. But they must be strategically engaged and understand the fundamental dynamics and drivers of your business: economics, competition and ecosystem. This is an easy habit to reinforce in meetings. If board directors drift toward getting too tactically in the weeds, that’s great feedback to offer after the meeting.

Habit 7: Think outside the box

Good board members understand all the pieces on the chess table; great board members go one step further and pattern match to provide advice, history, context and anticipated consequences. This is an enormous benefit to CEOs focused on the minutiae of the day-to-day, particularly if a business operates in a trailblazing industry where many of the rules may not yet be written. As a CEO, if you’ve never seen something first hand before, it’s hard to get clarity and external perspectives, which is why it’s crucial that great board members bring pattern recognition and “out-of-the-box thinking” to their role.

At the end of the day, boards are there to support and direct a company. There’s no perfect formula, but by implementing these steps with a few healthy habits, CEOs can cultivate strong, dynamic boards for their companies.

The Three Signs of a Miserable Job (post, link), The Five Temptations of a CEO (post, link), and The Four Obsessions of an Extraordinary Executive (post, link) are all related around the topic of management.

Death by Meeting (post, link), The Five Dysfunctions of a Team (post, link), and Silos, Politics and Turf Wars, on the other hand, are all related around the topic of leading a team and healthy team dynamics. This latest book, which is the last of his six books for me, rounds out this topic nicely, in a fun “novel” format as is the case with his other books.

The book hammers home the theme of an executive team needing to first be a team and then second be a collection of group heads as a means of breaking down barriers that exist inside organizations. It also lays out a framework for creating high-level alignment inside a team. The framework may or may not be perfect — we are using a different one at Return Path (the Balanced Scorecard) that accomplishes most of the same things — but for those companies who don’t have one, it’s as good as any.

The most compelling point in the book, though is the point that teams often make the most progress, change the most, and do their best work when their backs are up against a wall. And the point Lencioni makes here is — “why wait for a crisis?”

At any rate, another good, quick book, and absolutely worth reading along with the others, particularly along with the other two closely related ones. I’m definitely sorry to be done with the series. We may try the “field guide” companion to The Five Dysfunctions and see how the practical exercises work out.

Getting Naked: A Business Fable About Shedding The Three Fears That Sabotage Client Loyalty (book, Kindle), is Patrick Lencion’s latest fable-on-the-go book, and it’s as good a read as all of his books (see list of the ones I’ve read and reviewed at the end of the post).

The book talks about the power of vulnerability as a character trait for those who provide service to clients in that they are rewarded with levels of client loyalty and intimacy. Besides cringing as I remembered my own personal experience as an overpaid and underqualified 21 year old analyst at how ridiculous some aspects of the management consulting industry are…the book really made me think. The challenge to the conventional wisdom of “never letting ‘em see you sweat” (we *think* vulnerability will hurt success, we *confuse* competence withego, etc.) is powerful. And although vulnerability is often uncomfortable, I believe Lencioni is 100% right – and more than he thinks.

First, the basic premise of the book is that consultants have three fears they need to overcome to achieve nirvana – those fears and the mitigation tactics are:

Fear of losing the business: mitigate by always consulting instead of selling, giving away the business, telling the kind truth, and directly addressing elephants in the room

Fear of being embarrassed: mitigate by asking dumb questions, making dumb suggestions, and celebrating your mistakes

Fear of feeling inferior: mitigate by taking a bullet for the client, making everything about the client, honoring the client’s work, and doing your share of the dirty work

But to my point about Lencioni being more right than he thinks…I’d like to extend the premise around vulnerability as a key to success beyond the world of consulting and client service into the world of leadership. Think about some of the language above applied to leading an organization or a team:

Telling the kind truth and directly addressing elephants in the room: If you’re not going to do this, who is? There is no place at the top of an organization or team for conflict avoidance

Asking dumb questions: How else do you learn what’s going on in your organization? How else can you get people talking instead of listening?

Making dumb suggestions: I’d refer to this more as “bringing an outside/higher level perspective to the dialog.” You never know when one of your seemingly dumb suggestions will connect the dots for your team in a way that they haven’t done yet on their own (e.g., the suggestions might not be so dumb after all)

Celebrating your mistakes: We’re all human. And as a leader, some of your people may build you up in their mind beyond what’s real and reasonable. Set a good example by noting when you’re wrong, noting your learnings, and not making the same mistake twice

Taking a bullet for your team, making everything about your team and honoring your team’s work: Management 101. Give credit out liberally. Take the blame for team failings.

Doing your share of the dirty work: An underreported quality of good leaders. Change the big heavy bottle on the water cooler. Wipe down the coffee machine. Order the pizza or push the beer cart around yourself. Again, we’re all human, leaders aren’t above doing their share to keep the community of the organization safe, fun, clean, well fed, etc.

There’s a really powerful message here. I hope this review at least scratches the surface of it.

The full book series roundup as far as OnlyOnce has gotten so far is:

Last week, I blogged about Bolster’s Board Benchmark survey results, which really laid bare the lack of diversity on startup boards. There are signs that this is starting to change slowly — one big one is that of all the board searches we are running at Bolster, about ⅔ of them are open to taking on first-time directors; and almost all are committed to increasing diversity on their boards.

This is also something that I would expect to take some time to change. Boards are small. Independent seats aren’t necessarily easy to open up. Seats don’t turn over often. And they take a while to fill, as CEOs are thorough in their recruitment and selection process.

My new mantra for Startup Boards is simple: 1-1-1.

1 member of the management team.

Then 1 independent for every 1 investor.

Simply put, this means you should grow from having 1, to 2, to 3 independent directors as your board grows from 3, to 5, to 7 members.

Here are four tough conversations you may have to have along the way, with some suggestions on how to navigate them. All of these conversations need to come with a point of view of why independence and diversity matters to your company, a lot of empathy, and appreciation for the value the person brings to the table.

The conversation with your co-founder about only one founder/executive on the board.This one will be the most personally difficult, since you likely have a strong personal bond. Expect to hear things like “Aren’t we partners in this business?” and “How come my vote doesn’t count?” Just let your co-founder know that while of course they’re a key partner, the company has a limited number of board seats to fill — each one is a golden opportunity to get an outside perspective on your business and get really good mindshare of an industry expert and create a new brand ambassador. You already have 100% of the mindshare and ambassadorship your co-founder has to offer. You can make that person a board observer, you can make sure they’re in all the key board conversations, and you can even give the person some special voting right in your charter or by-laws if you need to. But do not put them on the board. It’s obviously easier to do this from the beginning as opposed to removing them from the board down the road, but at least try to have the conversation up front that someday, it’s going to happen (note this could be a different dynamic if the person is a founder but no longer active in the business).

The conversation with an existing VC about leaving the board to make room for new investors or an independent. This one will be less personally difficult but will require you to be very artful since the VC is likely contractually given a board seat – meaning you’ll have to get them to give it up voluntarily. You may also want to align with another VC on your board to help the conversation or process along. Depending on the circumstances at hand, your key points of logic could be one of the following: (1) you don’t own as high a percentage of the company as you once did, and I’d like to make room for the new lead investor to join the board without compromising our independents or making the board too big; or (2) I’d like to replace you with an independent director who brings operator perspective and comes from an underrepresented group – it’s important to me that we build a diverse board, and it’s not great that we have don’t have gender or race/ethnic diversity on our board in this day and age. As with a co-founder, you could change this person’s designation to a board observer so they’re still present for key conversations, you’re not changing their Information Rights, which are likely contractually given in your charter, and if required, you can give the person or firm some sort of special voting rights if there’s something they can no longer block (but which they have a contractual right to block) by losing their board vote.

The conversation with a new potential investor about not taking a board seat. If you have a big new lead investor writing a $40mm check into a growth round, you may not have a leg to stand on. But new investors who write smaller checks as you get larger, who might only be buying a 5-10% stake in the business…there, you might have some wiggle room to negotiate. Your best bet is to do it early in the process before you have a term sheet, and do it as an exploratory conversation. Otherwise, your talking points are the same as talking to an existing investor above. Investors are starting to realize the power of a diverse board, and may be open to this conversation. Some are making this a proactive practice, notably two of my long-time investors and directors Fred Wilson and Brad Feld (and some of their partners at Union Square Ventures and Foundry Group) — and those investors have also been willing to mentor the new, first time board members once they join.

The conversation with an existing independent director about leaving the board when their term is up. Perhaps you have an existing independent director who is not adding to the diversity of the board, but you already have a full board. Or perhaps your existing independent director isn’t doing a great job or has grown stale in the role. Once a director is fully vested, you have an easy opportunity to thank them graciously and publicly for their service, extend their option exercise period multiple years, and affirm that they’ll still take your call if you need help on something. You should set this expectation up front when you give the director their initial grant. If they ask why you’re not renewing them, you can simply say something like “We’d like to add some fresh outside perspective to the team.” One thing to think about, particularly for early stage companies, is only giving new directors a 1 or 2-year vest on their first option grant, so you can make sure they’re a high value director…and so you can have the option of an easy exit (or re-up) in a shorter period of time than a traditional 4-year vest.

The net of it is that as CEO of a venture-backed company, you wield an enormous amount of (mostly soft) power around the composition of your board – probably a lot more than you think. You just have to wield that power gently and focus on the importance of building a diverse board in terms of both experience and demographics.

I keep expecting one of his books to be repetitive or boring, but Patrick Lencioni’s The Five Dysfunctions of a Team held my interest all the way through, as did his others. It builds nicely on the last one I read, Death by Meeting (post, link).

I’d say that over the 9 1/2 years we’ve been in business at Return Path, we’ve systematically improved the quality of our management team. Sometimes that’s because we’ve added or changed people, but mostly it’s because we’ve been deliberate about improving the way in which we work together. This particular book has a nice framework for spotting troubles on a team, and it both reassured me that we have done a nice job stamping out at least three of the dysfunctions in the model and fired me up that we still have some work to do to completely stamp out the final two (we’ve identified them and made progress, but we’re not quite there yet.

The dysfunctions make much more sense in context, but they are (in descending order of importance):

Absence of trust

Fear of conflict (everyone plays politically nice)

Lack of commitment (decisions don’t stick)

Avoidance of accountability

Inattention to results (individual ego vs. team success)

For those who are wondering, the two we’re still working on at the exec team level here are conflict and commitment. And the two are related. If you don’t produce engaged discussion about an issue and allow everyone to air their opinions, they will invariably be less bought into a decision (especially one they don’t agree with). But we’re getting there and will continue to work aggressively on it until we’ve rooted it out.

There’s one other interesting takeaway from the book that’s not part of the framework directly, which is that an executive has to be first and foremost a member of his/her team of peers, not the head of his/her department. That’s how successful teams get built. AND (this is key) this must trickle down in the organization as well. Everyone who manages a team of group heads or managers needs to make those people function well as a team first, then as managers of their own groups second.

At any rate, another quick gem of a book. I’m kind of sorry there’s only one left in the series.

I love having independent directors on my Board. They are a great third leg of the stool alongside a CEO/Founder and VCs. They provide the same kind of pattern matching and outside point of view as VCs — but from a completely different perspective, that of an operator or industry expert. The good ones are CEOs or CXOs who aren’t afraid to challenge you. Equally important, they’re not afraid to challenge your VCs. At Return Path, I always had 2 or 3 independent directors at any given time to balance out VCs, and some have become great long term friends like Scott Petry, Jeff Epstein, and Scott Weiss. At Bolster, we’re already having a great experience with our first independent, Cristina Miller, and we’re about to add a second independent. And I’ve served as an independent director multiple times.

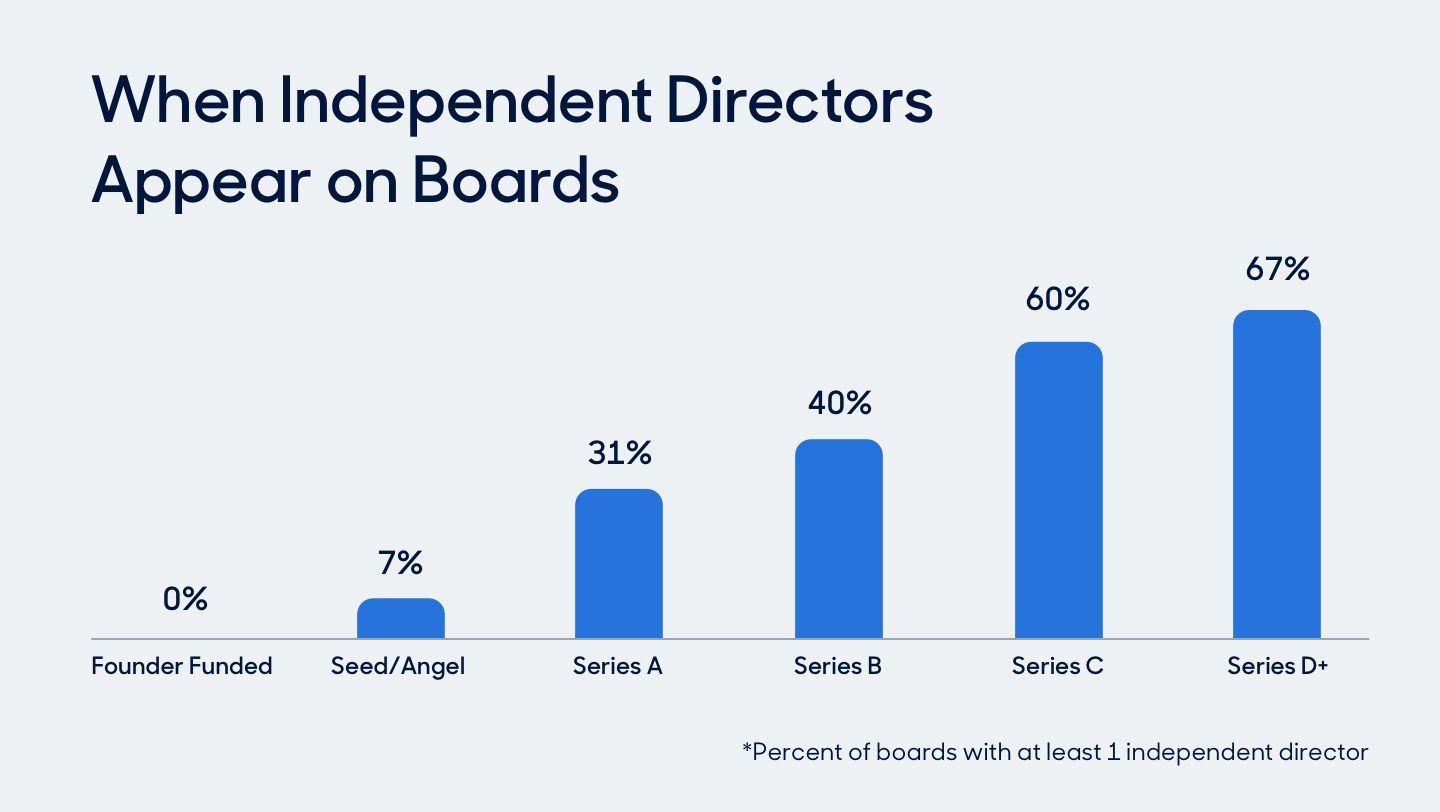

So as you can imagine, I was shocked by one of the headlines coming out of the Board Benchmark study we ran at Bolster across 250+ clients (detailed blog post with a bunch of charts and graphs) that only ⅓ of companies in the study have any independent directors. Even larger companies at the Series C and D levels only have independent directors 60% and 67% of the time. What a missed opportunity for so many companies.

Less surprising, though still sobering, were the numbers on diversity that came out of the study. 79% of the directors in the sample are white. 86% are men. 43% of boards are completely racially homogenous (most all-white) while 80% are mostly racially homogeneous (meaning only one diverse member); 56% are gender homogenous (most all men), while 87% are mostly gender homogenous (only one female). For an industry that is spending a lot of time talking about diversity in leadership teams and on boards, that’s disappointing.

Here’s the linkage of the two topics: The solution to the board diversity problem lies in having more independent directors, since management and VC board seats are often both “fixed” and non-diverse. Independent seats are the easiest to fill with diverse candidates. Conveniently, more independent directors also leads to higher quality boards.

In partnership with some DEI experts, our study also includes some suggested actionable tips for CEOs and board leaders, which I encourage you to read. There are really three simple (IMO) steps to having more diverse boards, and there is some good news in the Bolster study around these points:

Add independent director seats. 50% of the companies in the survey either have or expect to have an independent board seat open within 12 months. That’s a good start, but honestly, I can’t imagine running any board without at least 1-2 independent directors (up to 3-4 for larger companies), starting on Day 1. Given that only ⅓ of companies in the sample have any independent board members at all, the 50% number feels quite low.

Open the recruiting funnel to include first-time directors. Historically, companies have mainly targeted current or former CEOs or people who have board experience to be independent directors. That is a recipe to perpetuate having mostly white male board members. But Bolster has done a few dozen board searches so far, and 66% of those clients have expressed a willingness to take on first-time directors, as long as they are “board ready,” which we define as having been on any kind of board, not just a corporate board; having reported to a founder or CEO and had regular interaction with and presentations to a board; or having significant experience as a formal or informal advisor. Once you widen the funnel to include all candidates who meet those criteria, you can very easily have a diverse slate of highly qualified candidates. Bolster is a great source of these candidates (this is a real focal point for our business), but there are plenty of other online or search firm sources as well.

Have the courage to limit the number of management/investor board members. Whether or not you can add independent board members may be a function of how many seats you have to play with in your corporate charter. Of course, you can add seats indefinitely, but there’s no reason to have a 7-person board for your Series A company. My rule of thumbs on this are simple: (a) Only one founder member of the management team on the Board – more than that is a waste of a valuable board slot; and (b) VCs should always be less than 50% of your board members, so as new ones roll on, old ones should roll off – or add a VC and an independent at the same time. Both of these take serious effort and courage, both are worth it, and both probably merit a longer blog post someday.

The Board Benchmark study also had a wealth of information about compensation for independent directors — cash vs. stock, what kind of stock, how much stock, vesting and acceleration provisions.

Here’s a Slideshare of the full survey results, in case this and/or the Bolster blog link isn’t detailed enough for you:

If you’re interested in learning more, the survey is free to take and all the granular results (including comp benchmarks) are available to benchmark against your company if you take it. Just email me if you’re interested at [email protected].

Book Short: Steve Jobs and Lessons for CEOs and Founders

First, if you work in the internet, grew up during the rise of the PC, or are an avid consumer of Apple products, read the Walter Isaacson biography of Steve Jobs (book, kindle). It’s long but well worth it.

I know much has been written about the subject and the book, so I won’t be long or formal, but here are the things that struck me from my perspective as a founder and CEO, many taken from specific passages from the book:

In the annals of innovation, new ideas are only part of the equation. Execution is just as important. Man is that ever true. I’ve come up with some ideas over the years at Return Path, but hardly a majority or even a plurality of them. But I think of myself as innovative because I’ve led the organization to execute them. I also think innovation has as much to do with how work gets done as it does what work gets done.

There were some upsides to Jobs’s demanding and wounding behavior. People who were not crushed ended up being stronger. They did better work, out of both fear and an eagerness to please. I guess that’s an upside. But only in a dysfunctional sort of way.

When one reporter asked him immediately afterward why the (NeXT) machine was going to be so late, Jobs replied, “It’s not late. It’s five years ahead of its time.” Amen to that. Sometimes product deadlines are artificial and silly. There’s another great related quote (I forget where it’s from) that goes something like “The future is here…it’s just not evenly distributed yet.” New releases can be about delivering the future for the first time…or about distributing it more broadly.

People who know what they’re talking about don’t need PowerPoint.” Amen. See Powerpointless.

The mark of an innovative company is not only that it comes up with new ideas first, but also that it knows how to leapfrog when it finds itself behind. This is critical. You can’t always be first in everything. But ultimately, if you’re a good company, you can figure out how to recover when you’re not first. Exhibit A: Microsoft.

In order to institutionalize the lessons that he and his team were learning, Jobs started an in-house center called Apple University. He hired Joel Podolny, who was dean of the Yale School of Management, to compile a series of case studies analyzing important decisions the company had made, including the switch to the Intel microprocessor and the decision to open the Apple Stores. Top executives spent time teaching the cases to new employees, so that the Apple style of decision making would be embedded in the culture. This is one of the most emotionally intelligent things Jobs did, if you just read his actions in the book and know nothing else. Love the style or hate it – teaching it to the company reinforces a strong and consistent culture.

Some people say, “Give the customers what they want.” But that’s not my approach. Our job is to figure out what they’re going to want before they do. I think Henry Ford once said, “If I’d asked customers what they wanted, they would have told me, ‘A faster horse!’” People don’t know what they want until you show it to them. That’s why I never rely on market research. Our task is to read things that are not yet on the page. There’s always a tension between listening TO customers and innovating FOR them. Great companies have to do both, and know when to do which.

What drove me? I think most creative people want to express appreciation for being able to take advantage of the work that’s been done by others before us. I didn’t invent the language or mathematics I use. I make little of my own food, none of my own clothes. Everything I do depends on other members of our species and the shoulders that we stand on. And a lot of us want to contribute something back to our species and to add something to the flow. It’s about trying to express something in the only way that most of us know how—because we can’t write Bob Dylan songs or Tom Stoppard plays. We try to use the talents we do have to express our deep feelings, to show our appreciation of all the contributions that came before us, and to add something to that flow. That’s what has driven me. This is perhaps one of the best explanations I’ve ever heard of how creativity can be applied to non-creative (e.g., most business) jobs. I love this.

My board member Scott Weiss wrote a great post about the book as well and drew his own CEO lessons from it – also worth a read here.

Appropos of that, both Scott and I found out about Steve Jobs’ death at a Return Path Board dinner. Fred broke the news when he saw it on his phone, and we had a moment of silence. It was about as good a group as you can expect to be with upon hearing the news that an industry pioneer and icon has left us. Here’s to you, Steve. You may or may not have been a management role model, but your pursuit of perfection worked out well for your customers, and most important, you certainly had as much of an impact on society as just about anyone in business (or maybe all walks of life) that I can think of.

Over the years, I’ve had a list of nagging questions every time I’ve contemplated my board, but didn’t have anyone I could turn to who had deep, broad advice on this topic. Those questions were:

How big should my board be at this stage?

How many independent directors should I have?

What is the right profile of an independent director?

How many options should I give a board member?

How do I find the best, diverse, talent for my board openings?

That’s why Bolster is excited to announce the launch of our first CEO tool: Board Benchmarking. This application (which is free!) is the first of a series of tools that we’re designing to help CEOs understand the performance, design, and impact of themselves, their executive teams, and their boards. The results of this first application will shed light on the independence, diversity, and compensation of private company boards that’s never been available on a broad basis before.

Why are we starting with Board Benchmarking?

Increasing Board Diversity is top of mind right now… …and that means CEOs need to have a handle on three things at the same time to get it right: appropriate board size/number of independent seats, a talent pipeline that is diverse and well vetted, and clear compensation guidelines for independent directors. Diverse employee populations and customer bases start with having a diverse board and a CEO (you!) who is attuned to the benefits of diversity at the top. The longer you wait to prioritize diversity in the boardroom, the harder it becomes to change the makeup of your board. Culture becomes entrenched, recruiting becomes driven by referrals, and before you know it, everyone in an organization looks and thinks a little bit the same way. By capturing data on the diversity and composition of startup boards, we hope to offer an industry-wide snapshot to help CEOs start to have what can often be tricky conversations with their VCs about board size and composition as early as possible. And by pairing that with Bolster’s unique marketplace for diverse and vetted Board-ready talent, we hope to help CEOs slay all three dragons (number of independent seats, talent pipeline, and comp guidelines) at the same time.

Private company board composition is notoriously tricky to benchmark. Unlike public companies, which are required to disclose the identities and compensation packages for their boards of directors, private board structure tends to remain…well, private! While this makes sense from a regulatory perspective, it often means private companies CEOs are taking a shot in the dark when it comes to things like when to add independent directors and how much to pay them. By aggregating and anonymizing thousands of data points across hundreds of private companies, we hope to (for the first time ever) provide CEOs with a very real, in-the-moment look at how their board today stacks up against others in similar cohorts.

Filling an open board seat is a high-priority item for a CEO, and a tough one to get right. It’s said that good choices come from good options. Early benchmarking results show that half of startup CEOs expect to fill an open board position within the next 12 months. Just as it’s critically important to get the right executives around your (well, now virtual) table, it’s equally, if not even more important to build a board that effectively supports you, your company, and your customers. Every month that goes by with a board vacancy is another month where you’re potentially leaving valuable introductions and perspectives on the table. We hope that by exposing these board searches across such a broad subset of companies, we’ll also empower CEOs to take immediate next steps to fill those vacancies — including help recruiting multiple board candidates directly from the Bolster network.

As we conduct this survey over the next month, we’ll provide greater visibility into the size, composition, diversity, and director compensation of private company boards. We’re also establishing robust pipeline partnerships to amplify board-ready talent from organizations with diverse membership of African American, Hispanic/Latinx, and women orgs. So for anyone interested in adding qualified diverse talent to their boards, we’ll be ready.

Participants who complete the survey will receive early access to your benchmark results and a comprehensive guide to building and managing your Board of Directors.

In early Q1, we’ll invite all participants of our Board Benchmarking survey to log in to Bolster and view their results interactively. CEOs will be able to see how their own boards stack up compared to others in the VC portfolio network or other cohorts. VC partners will be able to see patterns across the entire portfolio.

Watch this space in the coming days and weeks for CEO-specific content about hiring Board members.

Brad Feld has been on my board for over a decade now, and when he and his partner Jason Mendelson told me about a new book they were writing a bunch of months ago called Venture Deals: Be Smarter Than Your Lawyer and Venture Capitalist, I took note. I thought, “Hmmm. I’d like to be smarter than my lawyer or venture capitalist.”

Then I read an advanced copy. I loved it. At first, I thought, I would really have benefited from this when I started Return Path way back when. Then as I finished reading it, I realized it’s just a great reference book even now, all these years and financings later. But as much as I enjoyed the early read, I felt like something was missing from the book, since its intended audience is entrepreneurs.

Brad and Jason took me up on my offer to participate in the book’s content a little bit, and they are including in the book a series of 50-75 sidebars called “The Entrepreneur’s Perspective” which I wrote and which they and others edited. For almost every topic and sub-topic in the book, I chime in, either building on, or disagreeing, with Brad and Jason’s view on the subject.

The book is now out. As Brad noted in his launch post, the book’s table of contents says a lot:

Bottom line: if you are an aspiring or actual entrepreneur, buy this book. Even if you’ve done a couple of financings, this is fantastic reference material, and Brad and Jason’s points of view on things are incredibly insightful beyond the facts. And I hope my small contributions to the book are useful for entrepreneurs as well.

Fred, Brad, and Jerry have done a bunch of postings recently, and threaten to do more, sharing the VC perspective on many aspects of startups and entrepreneurship. I thought it might be interesting to share the entrepreneur’s perspective on the same subjects. I’ll try to cross-post and keep pace, but I’m already a couple behind, and I can’t crank out postings as fast as these guys can! (For reference, Fred and Brad are on my board, and Jerry as Fred’s partner is an advisor to my company, Return Path.)

Topic 1: Boards of Directors. All three have many good points. Brad says that boards come in three flavors (working, reporting, and lame duck), and that small companies need working boards which include other entrepreneurs in the industry as well as management and investors. He also advises to take good care of directors and not let them get bored. Fred calls the good ones engaged boards (interactive, candid, engaged, passionate, and involved) and says that while you can have a good company without an engaged board and even with a bored bored on occasion, to have a great business you need an engaged board. Finally, Jerry says that you should pick your board carefully and build it with some diversity like you would a management team and to avoid people who will yes you.

I basically agree with all of these points, and would add the following four thoughts for entrepreneurs:

1. Building a board can be one of a CEO’s greatest trump cards. Without being even a little bit disingenuous, you can use the “I’m the CEO and would like to talk to you about a potential board seat with my company” as an entree to meet face to face with some of the most interesting, senior, brand-name people in your industry (turns out, flattery will occasionally get you somewhere). Use this card wisely and sparingly, and always be prepared to follow up on your meetings, but take full advantage of it as a way to network. You never know what opportunities you’ll uncover along the way.

2. Don’t think of managing your Board as a burden. Communicate early and often to your Board members and make sure all big conversations and debates are pre-wired in one-to-one conversations before Board meetings, and that debates are framed and researched properly in advance of meetings. Nail the basics (reporting, financial reviews, well-crafted and easy-to-read materials sent out several days before the meeting), so you can focus the valuable meeting time on strategy, not on the minutiae.

3. Figure out how to work differently with investor directors and outside directors. VCs who sit on your board have very different interests, time availability, and things to contribute than outside directors, especially non-retired industry executives. Not all directors are created equally, and you don’t have to behave as if they are.

4. Sit on a board yourself. There’s nothing like a real-live counterpoint to make you take a step back and think about how to build and run an effective board. Find something — another startup, a nonprofit, your high school or college alumni association — to join as a board member. Watch and learn.

All that said, the most important thing I’ve found in running a board is following Brad, Jerry, and Fred’s collective wisdom about fostering an engaged/working board. Definitely don’t let them get bored on you!