The quest for diversity in Tech leadership is stalling. Here’s why.

There’s been a growing cry for tech companies to add diversity to their leadership teams and boards, and for good reason. Those two groups are the most influential decision making bodies inside companies, and it’s been well documented that diverse teams, however you define diversity — diversity of demographics, thoughts, professional experience, lived experience — make better decisions.

Gender, racial, and ethnic representation in executive teams and in board rooms are not new topics. There’s been a steady drumbeat of them over the last decade, punctuated by some big newsworthy moments like the revelations about Harvey Weinstein and the tragic murder of George Floyd.

It’s also true that in people-focused organizations, and most tech companies claim to be just that, it’s beneficial to have different types of leaders in terms of role modeling and visibility across the company. As one younger woman on my team years ago said, “if you can see it…you can be it!”

My company Bolster is a platform for CEOs to efficiently build out their executive teams and boards. But while nearly every search starts with a diversity requirement, many don’t end that way.

Here’s why, and here’s what can be done about it.

For boards, the “why” is straightforward. Board searches are almost never a priority for CEOs. They’re viewed as optional. Bolster’s Board Benchmark study in 2021 indicated that only a third of private companies have independent directors at all;even later stage private companies only have independent directors two-thirds of the time. That same study indicated that 80% of companies had open Board seats. The comparable longitudinal study in 2022 indicated that the overwhelming majority of those open board seats were still open.

Independent directors are usually the key to diversity, as the overwhelming majority of founders and VCs are still white and male. It takes a lot of time and effort to recruit and hire and onboard new directors, and in the world of important versus urgent, it will always be merely important. Without prioritizing hiring independents, board diversity may be a lofty goal, but it’s also an empty promise. I wrote about my Rule of 1s here and in Startup Boards – I wish more CEOs and VCs took the practice of independent boards and board diversity seriously. The silver lining here is that when CEOs do end up prioritizing a search for an independent director, they are increasingly open to diverse directors, even if those people have less experience than they might want. That openness to directors who may never have been on a corporate board (but who are board-ready), who may be a CXO instead of a CEO, is key. Of the several dozen independent directors Bolster has helped match to companies in the past year, almost 70% of them are from demographic populations that are historically underrepresented in the boardroom.

Diversity is stalling for Senior Executive hiring for the opposite reason. Exec hires are usually urgent enough that CEOs prioritize them. And they frequently start their searches by talking about the importance of diversity. But Senior Executives are much more often hired for their resume than for competency or potential. Almost all executive searches start with some variation of this line, which I’m lifting directly from a prior post: “I want to hire the person who took XYZ Famous Company from where I am today to 10x where I am today.” The problem with that is simple. That person is no longer available to be hired. They have made a ton of money, and they have moved beyond that job in their career progression. So inevitably, the search moves on to look for the person who worked for that person, or even one more layer down…or the person who that person WAS before they took the job at XYZ Famous Company. Those people may or may not be easy to find or available, but they feel less risky. In the somewhat insular world of tech, those candidates are also far less likely to be diverse in background, experience, thought, or, yes, demographics.

Running a comprehensive executive search based on competencies, cultural fit, scale experience, and general industry or analogous industry experience is much harder. It takes time, patience, digging deeper to surface overlooked candidates or to check references, and probably a little more risk taking on the part of CEOs. And while CEOs may be willing to take some risk on a first-time independent director, fewer are willing to take a comparable level of risk on an unproven or less known executive hire.

For some CEOs, the answer is just to take more risk — or more to the point, recognize that any senior hire carries risk along a number of dimensions, so there’s no reason to prioritize your narrow view of resume pedigree over any critical vector. For others, the answer may be to bring the focus of diversity in senior hires to “second level” leaders like Managers, Directors, or VPs, where the perceived risk is lower, and the willingness to invest in training and mentorship is higher. Those people in turn can be promoted over time into more senior positions.

Not every executive or board hire has to be demographically diverse. Not every executive team or board has to have individual quotas for different identity groups, and diversity has many flavors to it. But without doing the work, tech CEOs will continue to bemoan the lack of diversity in their leadership ranks, and miss out on the benefits of diverse leadership, while not taking ownership for those efforts stalling.

What Does Great Look Like in a Chief People Officer?

This is the second post in the series…. the first one When to hire your first Chief People Officer is here).

While all CXOs are important to a company, the Chief People Officer is the one role you don’t want to get wrong because People Ops impacts every facet of a company. If you hire the wrong people—even one wrong person—you’ll regret it, and so will everyone else in your company. If you short-change the onboarding process you’ll create tons of work for others in the company to answer questions, teach people the systems, and help them get up to speed quickly—not to mention the frustration of the new hire. And of course, if you or your employees do anything illegal, discriminatory, or harassing, you’ll end up in legal trouble and you’ll lose—big time. So, it’s not enough, if you’re expanding rapidly, to “just get a Chief People Officer,” you need to hire a great Chief People Officer and I have found that great Chief People Officers do three things particularly well:

The most important characteristic or attribute of a great Chief People Officer is that they believe their function is strategic. In Startup CXO Chief People Officer Cathy Hawtrey wrote about the ways in which HR/People can be a strategic function and not just a tactical corporate function. It’s true of most functions, but for whatever reason, (likely past experience), HR leaders frequently don’t view themselves or their functions as strategic, which is not only a huge missed opportunity but maybe says something more important about the confidence level of the Chief People Officer. If that’s their frame of reference, then they will likely be tactical managers, they’ll keep the trains running on time, but you won’t be able to anticipate the changing talent landscape, much less be strategic about it. If they believe they can move the needle on the business by improving engagement and productivity and efficiency, if they believe they can make the executive team more effective by helping you with team facilitation and coaching…they can do anything.

A second important characteristic of the Chief People Officer is courage—they have the courage to call you (you, the CEO) out on things directly and firmly when they see you doing or saying anything that is a bit off. It could be around language, inclusion, values, authenticity, or anything else, but they don’t let it slide or ignore it. The CPO, along with you, are the principal stewards of the company’s values and culture. Even the best CEOs benefit from having a watchdog from time to time.

A third critical trait of a great Chief People Officer is that they think about investment in People in terms of ROI. It’s one thing to run a killer recruiting function and fill seats efficiently, with high quality, as asked. It’s an entirely different thing to start the recruiting process by asking if the role is needed, at that level and compensation band, or whether there are other people, fractional people, contractors, or shifts in lower value activities that could be put to work instead. Only heads of People with deep understandings of the business can transform the function from a gatekeeper/”no” role into a business accelerator.

A great Chief People Officer is all of these things—strategic, courageous, and financially astute. Above all, great Chief people Officers know that they are the role model within a company and that their behavior, their language, their inclusiveness is setting the tone and providing a template for others to follow.

(You can find this post on the Bolster Blog here)

Book Shorts: Summer Reading

I read a ton of books. I usually blog about business books, at least the good ones. I almost never blog about fiction or non-business/non-fiction books, but I had a good “what did you read this summer” conversation the other night with my CEO Forum, so I thought I’d post super quick snippets about my summer reading list, none of which was business-related.

If you have kids, don’t read Sheryl Sandberg and Adam Grant’s Option B: Facing Adversity, Building Resilience, and Finding Joy unless you’re prepared to cry or at least be choked up. A lot. It is a tough story to read, even if you already know the story. But it does have a number of VERY good themes and thoughts about what creates resilience (spoiler alert – my favorite key to resilience is having hope) that are wonderful for personal as well as professional lives.

Underground Airlines, by Ben Winters, is a member of a genre I love – alternative historical fiction. This book is set in contemporary America – except that its version of America never had a Civil War and therefore still has four slave states. It’s a solid caper in its own right, but it’s a chillingly realistic portrayal of what slavery and slave states would be like today and what America would be like with them.

Hillbilly Elegy, by J.D. Vance, is the story of Appalachia and white working class Americans as told by someone who “escaped” from there and became a marine, then a Yale-educated lawyer. It explains a lot about the struggles of millions of Americans that are easy for so many of us to ignore or have a cartoonish view of. It explains, indirectly, a lot about the 2016 presidential election.

Everybody Lies: Big Data, New Data, and What the Internet Can Tell Us About Who We Really Are, written by Seth Stephens-Davidowitz, was like a cross between Nate Silver’s The Signal and The Noise and Levitt & Dubner’s Freakonomics. It’s full of interesting factoids derived from internet data. Probably the most interesting thing about it is how even the most basic data (common search terms) are proving to be great grist for the big data mill.

P.J. O’Rourke’s How the Hell Did This Happen? was a lot like the rest of P.J. O’Rourke’s books, but this time his crusty sarcasm is pointed at the last election in a compilation of articles written at various points during the campaign and after. It didn’t feel to me as funny as his older books. But that could also be because the subject was so depressing. The final chapter was much less funny and much more insightful, not that it provides us with a roadmap out of the mess we’re in.

Sapiens: A Brief History of Humankind, by Noah Harari, is a bit of a rambling history of our species. It was a good read and lots of interesting nuggets about biology, evolution, and history, though it had a tendency to meander a bit. It reminded me a bit of various Richard Dawkins books (I blogged a list of them and one related business topic here), so if you’re into that genre, this wouldn’t be bad to pick up…although it’s probably higher level and less scientific than Dawkins if that’s what you’re used to.

Finally, I finished up the fourth book in the massive Robert Caro quadrilogy biography of Lyndon Johnson (full series here). I have written a couple times over the years about my long-term reading project on American presidential biographies, probably now in its 12th or 13th year. I’m working my way forward from George Washington, and I usually read a couple on each president, as well as occasional other related books along the way. I’ve probably read well over 100 meaty tomes as part of this journey, but none as meaty as what must have been 3000+ pages on LBJ. The good news: What a fascinating read. LBJ was probably (with the possible exception of Jefferson) the most complex character to ever hold the office. Also, I’d say that both Volumes 3 and 4 stand alone as interesting books on their own – Volume 3 as a braoder history of the Senate and Civil Rights; Volume 4 as a slice of time around Kennedy’s assassination and Johnson’s assumption of power. The bad news: I got to the end of Vol 4 and realized that there’s a Vol 5 that isn’t even published yet.

That’s it for summer reading…now back to school!

Momentum and Confidence: Everything Matters

As I stared at a dugout of dispirited 14 year old boys Saturday afternoon in our tournament championship game, I found myself talking to my fellow coach Mitch about a book I’d read a few years ago (turns out 14) called Confidence: How Winning Streaks and Losing Streaks Begin and End, written by HBS professor Rosabeth Moss Kantor. While that original blog post is pretty specific to something that was going on at that point in time in my prior company, the thinking in the book about momentum and the role it plays in our psychology, about sports, about business, and about life in general, is timeless.

Watching this team of teens go through ups and downs within an hour was incredibly stark and clear. In the first inning, we made three errors (just jitters from being in the championship…the Bulldogs are better than that!). Those opened the door for our opponent to post a few runs and take a quick lead. It was as if the wind had been taken out of our sails, as if all 11 kids just took a punch to the gut. They were shocked and pretty listless in the dugout, and nothing the coaches could do or say shook them out of it. They just *knew* they were going to lose, so why try? Their confidence was gone. It wasn’t until we staged our own big rally, later in the game, where all of a sudden, one, then two, then three base hits and the kids were going bananas, up at the fence of the dugout and screaming, cheering each other on and feeling all of a sudden like we could win the game.

The swing in momentum took about 5 minutes in each direction. And all that was involved was a couple quick negative/positive indicators/actions.

The bottom line is that we still lost the game 10-5. But the energy that came from a couple positive developments that stopped a downward spiral and started an upward one was palpable and instructive. As one of my other fellow coaches Jay said to the boys after the game, “Boys, the lesson from today is that Everything Matters. We lost 10-5, but when we were only down by 5 runs with the bases loaded, how much did we regret those couple of errors in the first inning? Without those, we would have been down by 2 runs with victory in reach.”

It’s the same in startups.

When you run a startup, you regularly take three punches to the gut in a row — a client cancels on you, you have a web site outage, an employee quits — and all of a sudden, you view the world through a dark lens of, as my long-time friend and Board member Scott Weiss used to say, WFIO, short for We’re F#%ked, It’s Over (pronounced whiff-ee-oh).

And then, the opposite happens, and it’s like the heavens part and the angels start singing a hallelujah chorus. You win a big new deal. You get unexpected positive press or a key blogger or tweet creates massive buzz for you. Your CFO pings you with the news that revenue is surprisingly high this month. WFIO is suddenly replaced with what I’ll call WGTWIA — We’re Going to Win It All (let’s pronounce it wig-twee-uh).

And what’s the difference? Probably nothing big. Probably a couple small things that just happened to break in the right or wrong direction at the right time. That call or email you decided not to return for a couple days until it was too late. That presentation you could have spent an extra 45 minutes perfecting instead of half-assing. That extra run through a new module of code you wrote to make sure it’s fully debugged. Just like a few silly errors in 14-year old baseball because you had the jitters early in a big game.

Everything Matters. In sports, in business, in life. Anything you think is a “throw away” can turn out in retrospect to have made the difference between winning and losing, between success and failure.

My new Startup Board Mantra: 1-1-1

Last week, I blogged about Bolster’s Board Benchmark survey results, which really laid bare the lack of diversity on startup boards. There are signs that this is starting to change slowly — one big one is that of all the board searches we are running at Bolster, about ⅔ of them are open to taking on first-time directors; and almost all are committed to increasing diversity on their boards.

This is also something that I would expect to take some time to change. Boards are small. Independent seats aren’t necessarily easy to open up. Seats don’t turn over often. And they take a while to fill, as CEOs are thorough in their recruitment and selection process.

My new mantra for Startup Boards is simple: 1-1-1.

1 member of the management team.

Then 1 independent for every 1 investor.

Simply put, this means you should grow from having 1, to 2, to 3 independent directors as your board grows from 3, to 5, to 7 members.

Here are four tough conversations you may have to have along the way, with some suggestions on how to navigate them. All of these conversations need to come with a point of view of why independence and diversity matters to your company, a lot of empathy, and appreciation for the value the person brings to the table.

The conversation with your co-founder about only one founder/executive on the board. This one will be the most personally difficult, since you likely have a strong personal bond. Expect to hear things like “Aren’t we partners in this business?” and “How come my vote doesn’t count?” Just let your co-founder know that while of course they’re a key partner, the company has a limited number of board seats to fill — each one is a golden opportunity to get an outside perspective on your business and get really good mindshare of an industry expert and create a new brand ambassador. You already have 100% of the mindshare and ambassadorship your co-founder has to offer. You can make that person a board observer, you can make sure they’re in all the key board conversations, and you can even give the person some special voting right in your charter or by-laws if you need to. But do not put them on the board. It’s obviously easier to do this from the beginning as opposed to removing them from the board down the road, but at least try to have the conversation up front that someday, it’s going to happen (note this could be a different dynamic if the person is a founder but no longer active in the business).

The conversation with an existing VC about leaving the board to make room for new investors or an independent. This one will be less personally difficult but will require you to be very artful since the VC is likely contractually given a board seat – meaning you’ll have to get them to give it up voluntarily. You may also want to align with another VC on your board to help the conversation or process along. Depending on the circumstances at hand, your key points of logic could be one of the following: (1) you don’t own as high a percentage of the company as you once did, and I’d like to make room for the new lead investor to join the board without compromising our independents or making the board too big; or (2) I’d like to replace you with an independent director who brings operator perspective and comes from an underrepresented group – it’s important to me that we build a diverse board, and it’s not great that we have don’t have gender or race/ethnic diversity on our board in this day and age. As with a co-founder, you could change this person’s designation to a board observer so they’re still present for key conversations, you’re not changing their Information Rights, which are likely contractually given in your charter, and if required, you can give the person or firm some sort of special voting rights if there’s something they can no longer block (but which they have a contractual right to block) by losing their board vote.

The conversation with a new potential investor about not taking a board seat. If you have a big new lead investor writing a $40mm check into a growth round, you may not have a leg to stand on. But new investors who write smaller checks as you get larger, who might only be buying a 5-10% stake in the business…there, you might have some wiggle room to negotiate. Your best bet is to do it early in the process before you have a term sheet, and do it as an exploratory conversation. Otherwise, your talking points are the same as talking to an existing investor above. Investors are starting to realize the power of a diverse board, and may be open to this conversation. Some are making this a proactive practice, notably two of my long-time investors and directors Fred Wilson and Brad Feld (and some of their partners at Union Square Ventures and Foundry Group) — and those investors have also been willing to mentor the new, first time board members once they join.

The conversation with an existing independent director about leaving the board when their term is up. Perhaps you have an existing independent director who is not adding to the diversity of the board, but you already have a full board. Or perhaps your existing independent director isn’t doing a great job or has grown stale in the role. Once a director is fully vested, you have an easy opportunity to thank them graciously and publicly for their service, extend their option exercise period multiple years, and affirm that they’ll still take your call if you need help on something. You should set this expectation up front when you give the director their initial grant. If they ask why you’re not renewing them, you can simply say something like “We’d like to add some fresh outside perspective to the team.” One thing to think about, particularly for early stage companies, is only giving new directors a 1 or 2-year vest on their first option grant, so you can make sure they’re a high value director…and so you can have the option of an easy exit (or re-up) in a shorter period of time than a traditional 4-year vest.

The net of it is that as CEO of a venture-backed company, you wield an enormous amount of (mostly soft) power around the composition of your board – probably a lot more than you think. You just have to wield that power gently and focus on the importance of building a diverse board in terms of both experience and demographics.

The Startup Ecosystem Needs More Independent Board Members – That’s the Clearest Path to Having Better and More Diverse Boards

I love having independent directors on my Board. They are a great third leg of the stool alongside a CEO/Founder and VCs. They provide the same kind of pattern matching and outside point of view as VCs — but from a completely different perspective, that of an operator or industry expert. The good ones are CEOs or CXOs who aren’t afraid to challenge you. Equally important, they’re not afraid to challenge your VCs. At Return Path, I always had 2 or 3 independent directors at any given time to balance out VCs, and some have become great long term friends like Scott Petry, Jeff Epstein, and Scott Weiss. At Bolster, we’re already having a great experience with our first independent, Cristina Miller, and we’re about to add a second independent. And I’ve served as an independent director multiple times.

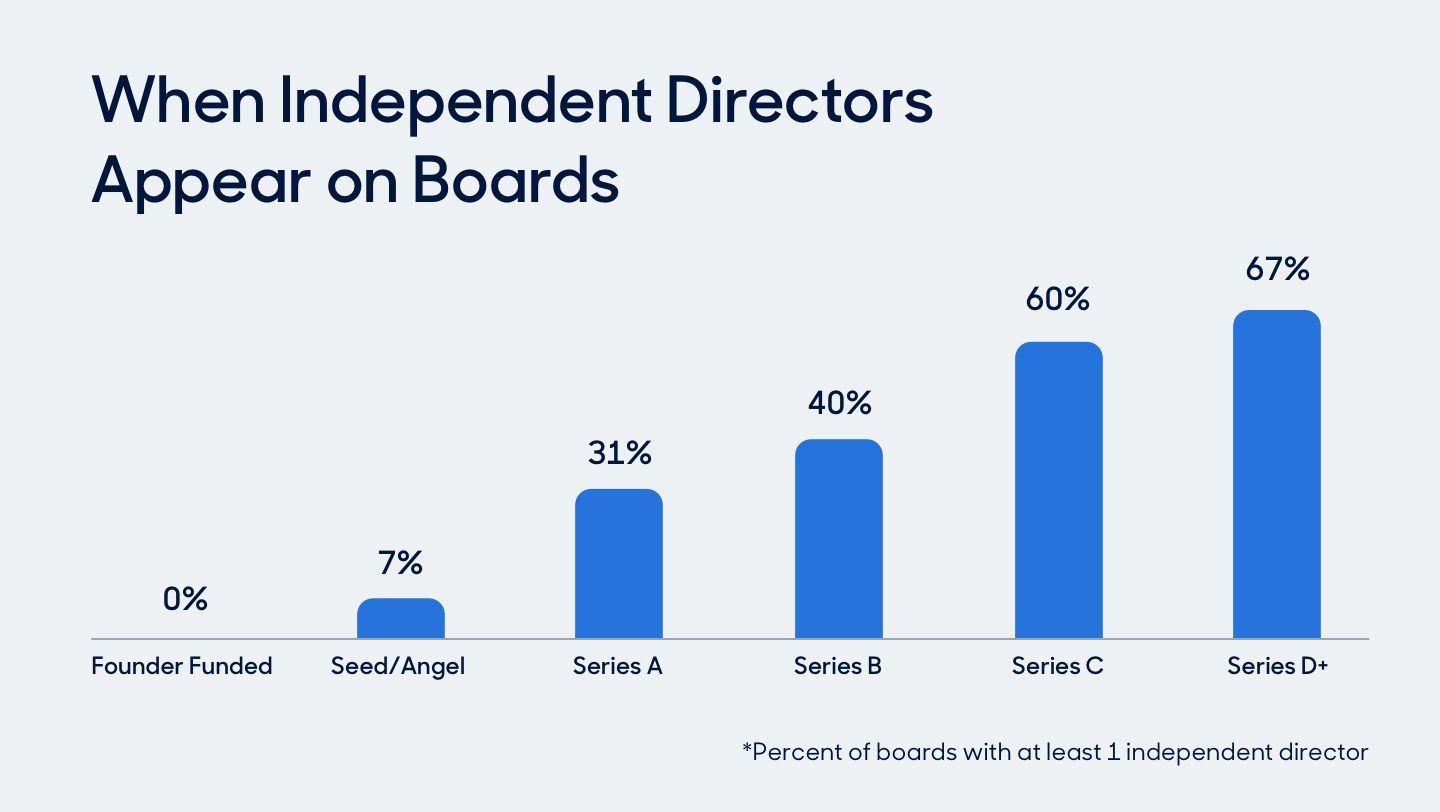

So as you can imagine, I was shocked by one of the headlines coming out of the Board Benchmark study we ran at Bolster across 250+ clients (detailed blog post with a bunch of charts and graphs) that only ⅓ of companies in the study have any independent directors. Even larger companies at the Series C and D levels only have independent directors 60% and 67% of the time. What a missed opportunity for so many companies.

Less surprising, though still sobering, were the numbers on diversity that came out of the study. 79% of the directors in the sample are white. 86% are men. 43% of boards are completely racially homogenous (most all-white) while 80% are mostly racially homogeneous (meaning only one diverse member); 56% are gender homogenous (most all men), while 87% are mostly gender homogenous (only one female). For an industry that is spending a lot of time talking about diversity in leadership teams and on boards, that’s disappointing.

Here’s the linkage of the two topics: The solution to the board diversity problem lies in having more independent directors, since management and VC board seats are often both “fixed” and non-diverse. Independent seats are the easiest to fill with diverse candidates. Conveniently, more independent directors also leads to higher quality boards.

In partnership with some DEI experts, our study also includes some suggested actionable tips for CEOs and board leaders, which I encourage you to read. There are really three simple (IMO) steps to having more diverse boards, and there is some good news in the Bolster study around these points:

- Add independent director seats. 50% of the companies in the survey either have or expect to have an independent board seat open within 12 months. That’s a good start, but honestly, I can’t imagine running any board without at least 1-2 independent directors (up to 3-4 for larger companies), starting on Day 1. Given that only ⅓ of companies in the sample have any independent board members at all, the 50% number feels quite low.

- Open the recruiting funnel to include first-time directors. Historically, companies have mainly targeted current or former CEOs or people who have board experience to be independent directors. That is a recipe to perpetuate having mostly white male board members. But Bolster has done a few dozen board searches so far, and 66% of those clients have expressed a willingness to take on first-time directors, as long as they are “board ready,” which we define as having been on any kind of board, not just a corporate board; having reported to a founder or CEO and had regular interaction with and presentations to a board; or having significant experience as a formal or informal advisor. Once you widen the funnel to include all candidates who meet those criteria, you can very easily have a diverse slate of highly qualified candidates. Bolster is a great source of these candidates (this is a real focal point for our business), but there are plenty of other online or search firm sources as well.

- Have the courage to limit the number of management/investor board members. Whether or not you can add independent board members may be a function of how many seats you have to play with in your corporate charter. Of course, you can add seats indefinitely, but there’s no reason to have a 7-person board for your Series A company. My rule of thumbs on this are simple: (a) Only one founder member of the management team on the Board – more than that is a waste of a valuable board slot; and (b) VCs should always be less than 50% of your board members, so as new ones roll on, old ones should roll off – or add a VC and an independent at the same time. Both of these take serious effort and courage, both are worth it, and both probably merit a longer blog post someday.

The Board Benchmark study also had a wealth of information about compensation for independent directors — cash vs. stock, what kind of stock, how much stock, vesting and acceleration provisions.

Here’s a Slideshare of the full survey results, in case this and/or the Bolster blog link isn’t detailed enough for you:

If you’re interested in learning more, the survey is free to take and all the granular results (including comp benchmarks) are available to benchmark against your company if you take it. Just email me if you’re interested at [email protected].

Bolster’s Founding Manifesto

(This post also appeared on Bolster.com and builds on last week’s post where I introduced my new startup, Bolster)

Welcome to Bolster, the on-demand executive talent marketplace. We are creating a platform that is the new way to scale an executive team and board.

support, boost, strengthen, fortify, solidify, reinforce, augment, reinvigorate, enhance, improve, invigorate, energize, spur, expand, galvanize, underpin, deepen, complement

We believe that startups and scaleups are not average companies. Their rapid growth means their appetite for talent constantly outstrips their budget — and that they can’t spend months searching for it. Their dynamic industries dictate that they keep pace with bigger and better funded competitors. Their leadership teams — the people and the roles — are always changing. Their CEOs spend a ton of time hiring and coaching their leaders and shaping the complexion and direction of the team. They stress out about big expensive new executive hires when sometimes they just need to level-up an existing manager or “try before they buy.” Their Boards frequently jump in to help, but those efforts can be a little ad hoc and inefficient.

We believe that experienced executives working as consultants is the wave of the future. The number of career executives who work flexibly and on-demand for a living is skyrocketing in recent years. People are more often “between things” and are interested in plugging into shorter-term engagements while continuing to look for their next full-time role. People are retiring younger, yet wanting to keep contributing. And even fully-employed execs like to advise companies and serve on Boards. Whether these people are career consultants or are looking for a “side hustle” or just to pay something forward to a future generation of leaders, they all have two common problems: finding work is time consuming and they’re often not good at or don’t like doing it; and managing their back office, everything from insurance to legal to tax to marketing, is a drain on time that could otherwise be spent with clients or family.

We believe that a new kind of talent marketplace is needed to meet the unique and complex requirements of both audiences — the freelance, or flexible, seasoned executive, and the startup or scaleup CEO who thinks holistically about his or her leadership team and carefully tends them like a garden. We are building a platform to make instant, tailored, vetted matches between talent and companies without the randomness of a job board and without the theater, long lead times, and cost, of a full service agency

Service marketplaces like ours work best when they help their stakeholders solve other meaningful, related problems.In this case, we believe that the need for back office services will help executive consultants focus on more important things. And we believe that CEOs need lightweight and dynamic support in thinking through the composition and skills required of their executive teams both today and 6-18 months in the future.

That is the essence of the business we are building. A business to quickly match awesome companies with awesome freelance executives and to help both sides be better at what they do. We are here to make it easier for you to:

- Bolster your executive team. For our Clients, our pledge to you is that we will quickly and cost-effectively fill the gaps in your leadership ranks (whether interim, fractional, advisory, board, or project-based) with trusted, curated talent, and that we will give you a platform to evaluate your overall leadership team and help you think through your future needs as your company evolves. Think of us as a shortcut to scaling your leadership team.

- Bolster your board. The best boards are the ones with multiple independent directors who come from diverse backgrounds with diverse points of view. We also pledge to our Clients that we will find great matches to help fill out their boardrooms as their strategic advisory needs change over time.

- Bolster your work. For our Members, our pledge to you is that we will find you the right kind of interesting clients and help you manage your back office so you can focus on your work (and all the other important things in your life!).

- Bolster your portfolio. For our Portfolio Partners, VC and PE board members, our pledge to you is that we will make it easier for you and your firm to both drive successful on-demand executive placements for your portfolio company CEOs, and to manage and expand your firm’s network of flexible executive talent.

We are an experienced team of entrepreneurs and operators who have scaled multiple businesses throughout our careers. All of us worked together as part of the leadership team at Return Path, a leading email technology company that we scaled from 0 to $100mm in revenue and 500 employees in 12 locations around the world while winning numerous Employer of Choice awards. All of us have independent experience scaling other businesses, small and large, public and private. All of us have experience being on-demand executives as well — whether interim, fractional, advisory, project-based, or board roles, we know the landscape of both our members and our clients.

We’ve all dealt with the stress of having product-market fit and market opportunities but not being able to capitalize on those opportunities because we were missing key talent. And we’ve tried everything from executive search firms (expensive, time-consuming, and slow), to leveling up people (will they be able to grow into the role?), to leaning in to our board (hit or miss, inefficient). Heck, we’ve been desperate enough to follow up on the “my cousin’s boyfriend has an uncle, and he might know someone” lead.

We believe there is a better way for startups and scaleups to find executive talent. Along the way, I published a book about scaling startups called Startup CEO: A Field Guide to Scaling Up Your Business that has sold over 40,000 copies to CEOs around the world. And our whole team is working on a new book called Startup CXO: A Field Guide to Scaling Up Your Teams, which is coming out in early 2021. Our team has a maniacal focus on helping startup teams scale and flourish and on helping leaders develop into the best version of themselves. That’s what we’re all about.

Plus, we have an amazing group of investors behind us who know how to grow businesses like ours and have incredible reach into the startup and scaleup world. More about that later. For now, we are excited to soft launch Bolster and begin unleashing the power of on-demand executive talent to our Clients. Thank you for being on this journey with us. If you’re interested in the somewhat unusual story of how the company was founded, it’s here.

Startup CEO, Second Edition Teaser: The Importance of Authentic Leadership in Changing Times

As I mentioned the other day, the second edition of Startup CEO is out. This post is a teaser for the content in one of the new chapters in this edition on Authentic Leadership.

As I mentioned last week, the book went to press early in the COVID-19 pandemic and prior to all the protests around racial injustice surrounding the George Floyd killing, so nothing in it specifically addresses any of those issues. In some ways, though, that may be better at the moment since the book is more about frameworks and principles than about specific responses to current events. Two of those principles, which are timeless and transcend turmoil, uncertainty, time and place, are creating space to think and reflect and being intentional in your actions. In a world in which CEOs are increasingly called upon to deal with more than traditional business (pricing, strategy, go-to market approaches, team building, etc.) it’s imperative to approach and solve challenging situations from a foundation that doesn’t waver.

At Return Path our values were the foundation that provided a lens through which we made every decision. Well, not every decision, only the good ones. When we strayed from our core values, that got us into trouble. The other principle, outlined in Chapter 1 of the Second Edition, is leading an organization authentically.

Let me provide a couple concrete examples of what I mean by “Authentic Leadership” since the term can be interpreted many ways.

One example is to avoid what I call the “Say-Do” gap. This is obviously a very different thread than talking about how the company relates to the outside world and current events. But in some ways, it’s even more important. A leader can’t truly be trusted and followed by their team without being very cognizant of, and hopefully avoiding close to 100%, any gap between the things they say or policies they create, and the things they do. There is no faster way to generate muscle-pulling eyerolls on your team than to create a policy or a value and promptly not follow it.

I’ll give you an example that just drove me nuts early in my career here, though there are others in the book. I worked for a company that had an expense policy – one of those old school policies that included things like “you can spend up to $10 on a taxi home if you work past 8 pm unless it’s summer when it’s still light out at 8 pm” (or something like that). Anyway, the policy stipulated a max an employee could spend on a hotel for a business trip, but the CEO (who was an employee) didn’t follow that policy 100% of the time. When called out on it, did the CEO apologize and say they would follow the policy just like everyone else? No, the CEO changed the policy in the employee handbook so that it read “blah blah blah, other than the CEO, President, or CFO, who may spend a higher dollar amount at his discretion.”

What does that say about the CEO? How engaged are employees likely to be, how much effort are they willing to devote to the company if there are special rules for the executives? You can make any rule you want — as you probably know if you have read a bunch of my posts or my book over the years, I’m a proponent of rule-light environments — but you can’t make rules for everyone else that you aren’t willing to follow yourself unless you own the whole company and don’t care what anyone thinks about you or says about you behind your back.

Beyond avoiding the Say-Do Gap, this new chapter of the book on Authentic Leadership also talks about how CEOs respond to current events in today’s increasingly politicized and polarized world. This has always felt to me like a losing proposition for most CEOs, which I talk about quite a bit in the book. When the world is polarized, whatever you do as CEO, whatever position you take on things, is bound to upset, alienate, or infuriate some nontrivial percentage of your workforce. I even give some examples in the book of how I focused on using the company’s best interests and the company’s values as guideposts for reacting (or not reacting) to politically divisive or charged issues like guns or “religious liberty” laws. I say this noting that there are some people who *believe* that their side of an issue like this is right, and the other side is wrong, but the issues have some element of nuance to them.

Today’s world feels a bit different, and I’m not sure what I would be doing if I was leading a known, scaled enterprise at this stage in the game. The largely peaceful protests around all aspects of racial injustice in America in the wake of the murder of George Floyd — and the brutality and senselessness of that murder itself — have caused a tidal wave of dialog reaching all corners of the country and the world. The root of this issue doesn’t feel to me like one that has a lot of nuance or a second side to the argument. After all, what reasonable person is out there arguing that George Floyd’s death was called for, or even that black Americans don’t have a deep-seeded and widespread reasonable claim to inequality…even if their view of what to do about it differs?

I *think* what I would be doing in a broader leadership role today is figuring out what my organization could be doing to help reduce or eliminate structural racial inequality where we could based on our business, as opposed to driving my organization to take a specific political stand. I know for sure that I wouldn’t solicit feedback from a select group of people only, but I would create a space where voices from across the organization (and stakeholders outside of it as well) could be heard. That’s not a solution, but a start, and in challenging times making a little bit of headway can lead to a cascading effect. It can, if you keep the momentum.

And, in line with “authentic leadership,” it’s okay to admit that you don’t have the answers, that you might not even know the questions to ask. But doing nothing, or operating in a “business as usual” way won’t make your company stronger, won’t open up new opportunities, won’t generate new ideas, and won’t sit well with your employees, who are very much thinking about these issues.

So, in today’s challenging times I would follow my own advice, be thoughtful and reflective, and intentional in searching for common solutions. I’d try to avoid “mob mentality” pressure — but I would also be listening carefully to my stakeholders and to my own conscience.

In the coming weeks, I’ll write posts that get into some of the other topics I cover in the book, but none of them will be as good as reading the full thing!

State of Colorado COVID-19 Innovation Response Team, Part VII – Retrospective

(This is the seventh and final post in a series documenting the work I did in Colorado on the Governor’s COVID-19 Innovation Response Team – IRT. Other posts in order are 1, 2, 3, 4, 5, and 6.)

I’ll start the final post in this series by sharing the overview and retrospective deck that we created my last day and the two days after. Governor Polis is going to share this with the National Governors Association in case other states are interested in our model or learnings. This pdf, which you’re welcome to download or just view in SlideShare, is a good overview of what we did and where things stood as of Saturday, March 28, noting that by the time you’re reading this post, half of it may be obsolete!

I am normally a small government guy. But not when this kind of thing hits. This whole thing calls for consistent national government response to the disease – potentially even global government coordination at a level we’ve never seen before (let alone the level that’s fashionable these days). I’m not sure I’d want a Chinese style lockdown (although that may prove to have been effective), but South Korea’s pattern of learning from SARS and MERS, bulking way up on labs, reagents, epidemiologists, ventilators, etc., and then passing legislation that allows for deeply intrusive tracking in case of a public health emergency like this seems to be the way to go.

Certainly, leaving responses up to individual states, counties, and cities is a problem. It’s inefficient and on average ineffective, although I think our group made some extraordinary progress on a few fronts. But the scale of the effort in an individual state of 6mm people with the associated resources just pales in comparison to what a strong federal response would be. Of course…the federal government has to actually believe in the need for a rapid and comprehensive response and have the wherewithal to pull it off for that to work.

As for our federal government’s economic responses, that’s a different story. At some point, the government literally won’t be able to afford to fill in the economic holes left behind by the virus (you could argue that we can’t even afford the $2T we’ve already ponied up since we are terrible at saving money when times are good and run huge deficits even then). I’m not sure what will happen then.

But government aside, I hope the response across the country and the world is enough to take the edge off this disease long enough for supply chains and healthcare systems to be able to properly respond. I hope that people who have the means will continue to support local businesses and individual/freelance service providers like housekeepers, gardeners, music teachers, tutors, and coaches through this stretch, even if those people aren’t able to provide those services. And I hope all the people who are on the ground working the problem – from frontline healthcare workers to my new friends in the Colorado state government and on the volunteer side – get the recognition they deserve for the extraordinary efforts they are undertaking to drive solutions and get everyone through this.

Special thanks to Governor Polis and his staff for the opportunity to do this work, to Brad for roping me into it and then letting me rope him into leading the private sector side, and to Kacey, Kyle, and Sarah, my new friends, for making it all work and for continuing the work after I left.

State of Colorado COVID-19 Innovation Response Team, Part VI – How This Compared to Running a Company

(This is the sixth post in a series documenting the work I did in Colorado on the Governor’s COVID-19 Innovation Response Team – IRT. Other posts in order are 1, 2, 3, 4, and 5.)

As these posts have been running, a few people have asked me to quickly compare this experience to the experience of being a Startup CEO. And that’s an interesting way to think about it. In a lot of ways, the couple of weeks of getting the IRT up and running felt like starting up a new business, only a lot more intense. Following the outline of sections in Startup CEO: a field guide to scaling up your business…

Part One: Storytelling. The whole timeframe was super compressed. It took us 2 days to be able to spend 4 hours writing our initial pitch deck defining scope, structure, and staffing request – and that was while we were working hard on our first two workstreams. In a startup environment, that process would have taken much longer, involved more customer discovery and product/market fit research and spending 100% of our time on that. But then we got our “approval and funding” in about 45 minutes – that would have taken weeks and involved dozens of pitch meetings. In terms of creating the organization’s Mission, Vision, and Values, we didn’t even bother, although I think it helped that the three of us were generally on the same page with how to work and that urgency was the essence of our job. The larger emergency operations team that we were more or less embedded in also had a very clear set of values and operating principles on display…although we didn’t actually go read them, I think they were in sync with our view of our team’s mission and principles. In terms of “bringing our story to life,” that was wholly unnecessary!

Part Two: Building The Company’s Human Capital. Like a startup, getting it right with the first handful of employees means everything. In this case, the first two deputies on the team, handpicked by the Governor’s staff, were awesome and critical. Bringing someone in from the private sector to run a public sector team only works when the rest of the team is incredibly knowledgeable about how the machinery of state government works. And in the end, I think Sarah will be a better leader for the team than I was because she had a combination of private and public sector experience (and within her public sector experience, she had a lot of emergency response experience). In general, the recruiting process was soooo different than private sector and public sector normally are. The first two team members handpicked the best people they knew in other relevant parts of the government. People were brought onto the team after one short phone call. Other state departments heads loaned their people willingly. No such thing as a comp negotiation or a reference check. There were a bunch of other things under the “Human Capital” heading that are interesting notes/comparables as well. First, feedback in a compressed-timeframe emergency is something that you absolutely can’t skip – and you can’t wait for a formal process either. Our team was pretty good about giving feedback at least daily in a semi-structured way as well as in the moment. We didn’t really have time to get into things like career pathing and compensation and firing. We did, after about 6 days at the suggestion of Kacey, our Chief of Staff, move the team to almost entirely remote (other than leadership and occasional critical meetings). This worked surprisingly well for a workforce probably unaccustomed to remote work. The rest of the world is also learning how to do a lot of that now, too.

Part Three: Execution. This whole experience was 97% execution. In fact, we had a hard time finding time for things like strategy and planning because there was a crushing amount of work to do (welcome to emergency response), and a small team to do it. We didn’t have to worry about raising money, budgeting, forecasting, reporting, and some of the other major execution steps in the private sector. We did do a good job of creating goals and milestones for our workstreams, but even that took a couple of weeks, and in retrospect, I wish we’d been able to do some of those sooner. In terms of how our work got done, we were very conscious of creating daily meeting routines to structure our day and work – but there was no such thing as even a weekly meeting (let alone monthly strategics or quarterly offsites!), only daily meetings, multiple times per day. One thing that was interesting – I talk in the book about being deliberate and consistent with your platforms, especially around communication. Channel proliferation is a real issue today (much more so than when I wrote the book), but we had an interesting mismatch at the beginning. The public sector team was used to email, text, and Google hangouts for comms. Nothing else. The private sector team used those things but was a lot more comfortable with Trello, Zoom, and Slack. Thank goodness both teams used G-Suite and not a mix of that and LiveOffice. But getting everyone on the team to converge on a couple systems is a work in progress and was messy, as evidenced in this great moment where Kacey was holding a laptop up to an actual whiteboard to show one of our private sector teams how she was thinking about something.

Part Four: Building and Leading a Board of Directors. This is kind of N/A, although the proxy for it in our case on the IRT was the leadership structure of the Emergency Operations Center and then the Governor and the part of his cabinet that was keyed into the emergency response. In this regard, the main differences between the private sector and public sector were speed/formality (no room for formality when you’re meeting daily or at a moment’s notice!), and, interesting, the need for integration. A company reports to its board on how it’s doing. This team had to use its “board” to make sure it was integrating with other state agencies and initiatives. In this way, the team functioned more like a business unit within a company than an actual company.

Part Five: Managing Yourself So You can Manage Others. This was obviously critical…and obviously quite difficult. And within the overall Emergency Operations Center (outside of our team, the real emergency professionals), there were people, including leaders, who were working 7 days/week for multiple weeks on end, and long days, too. At one point, the EOC leader posted this note on the wall, and he frequently took time in daily briefings to encourage everyone to take a day or two off and take care of themselves physically. He role-modeled that behavior as well. You can only run a sprint for so long. Once it becomes clear it’s a marathon, well, you know.

Stay tuned for the final post in the series tomorrow…

What Job is Your Customer Hiring You to Do?

My friend George, one of our co-founders at Return Path (according to him, the best looking of the three), has a wonderful and simple framing question for thinking about product strategy: what job is your customer hiring you to do? No matter what I’m working on, I am finding George’s wisdom as relevant as ever, maybe even more so since I am still learning the new context.

Why is this a useful question to ask? It seems really simple – maybe even too simple to drive strategy, doesn’t it?

It’s very easy in technology and content businesses (maybe other spaces too) to get caught up in a landslide of features and topics. In a dynamic world of competition and feature parity, product roadmaps can easily get cluttered. They can also get cluttered by product teams who have their own view of what should be the next feature, module, or content widget. Sometimes looking at product usage data is helpful, but sometimes it produces more noise than signal because it can easily miss the “why” or change day to day.

And once a product is mature, it can be very difficult to understand which of its many elements — even if they are all used — are the ones truly driving the most value for customers. It’s easy to assume it’s the newest, the slickest, the ones that are generating the most buzz. It’s even easier to assume that when it comes to content. But sometimes it’s now. Sometimes it’s the legacy part of the product. Sometimes it’s a small side feature you don’t focus on. Sometimes it’s something you used to do but don’t really do any more!

By asking customers the simple question — what are you hiring us to do for you? — you can start to get to the heart of the matter, the heart of what your strategy should be. Peeling the onion once you understand that and getting into the specifics of the different tasks or jobs your customer does that derive from your main point of value, as George would say, “jobs to be done,” is much more straightforward. When defining a Job to Be Done:

- Focus on a functional job (not an emotional one, e.g, “I need to look smart to the boss”)

- Try to ensure that you are looking at the whole job, not just a piece of the job. It’s easy to get too narrow in your definition

- Make sure it is the customer’s definition of the job, not yours

There’s always a role and a need for innovative product owners to help define a space, define value, demonstrate it for customers. This framework is meant to be additive to a high functioning product owner’s job, it can never replace it.

(As a small post-script, Friday December 6 marks 20 years since we started Return Path…a fitting day to post a bit of a tribute to George!)