Fighting Confirmation Bias

I was mentoring a first time founder the other day who asked me, “How do you know what advice to follow and what advice not to follow?” (For the record, it’s a little ”meta” to answer that question!). I talked about looking for patterns and common themes in the advice from others and exercising judgment about how to pick and choose from competing pieces of advice. But then he asked me how I fight confirmation bias when I’m exercising judgment and incoming advice.

Fighting confirmation bias is both incredibly important and incredibly difficult, and I’d never articulated my thoughts on that before, so I thought I’d do that here.

The way you have to train yourself to fight confirmation bias is to develop a routine or muscle around receiving a piece of advice that you don’t like. While the normal response is to dismiss it or argue against it, the muscle you have to build is to react to advice you don’t like by taking a beat and asking yourself, “Why don’t I like this advice?”

Is it that you think it’s factually wrong or is given on incomplete information? Is that it just disagrees with your world view? Or is it that you just hope it’s not true because it would mean bad things for you or your company? If it’s the latter, or something like it, it’s time to sit down and analyze the advice in the context of the question you asked. What happens if it is true? Why would it be true?

Under the headline of “hope is not a strategy,” doing that work gets you to a better place, because it’s in that work, in pausing to answer the question “Why don’t I like this advice,” that the hard work of fighting confirmation bias happens.

Should CEOs wade into Politics, Part III (From Tim Porthouse)

I’ve gotten to know a number of Bolster members over the last few years, and one who I have come to appreciate quite a bit is Tim Porthouse. I’m on Tim’s email list, and with his permission, I’m reprinting something he wrote in his newsletter this month on the topic of CEO engagement in politics and current events. As you may know, I’ve written a bunch on this topic lately, with two posts with the same title as this one, Should CEOs wade into Politics (part I here, part II here). Thanks to Tim for having such an articulate framework on this important subject.

Your Leadership Game: “No Comment.”

Should you speak up about news events/ politics?

Most of the time, I say, no!

Startup CEOs feel pressure to speak up on news events: Black Lives Matter, Abortion, LBGTQ+ rights, the conflict in Israel/Palestine, Trump vs. Biden. Many tell me they feel pressured to say something, but are deeply conflicted.

Like you, I am deeply distressed by wars, murder, restrictions on human rights, bias, and hate. But if we feel something, should we say something?

Before you speak up, ask the following questions:

1. Mission relevance. Is your startup’s success or mission on the line? Are customers or employees directly impacted? Example: It makes sense for Airbnb to advocate when a city tries to ban short-term rentals. It makes sense to advocate for your LBGTQ+ employees when a state tries to restrict their rights.

2. Moving the needle. Will speaking out change anything? If you “denounce” something or “take a stand,” what really happens? Example: If you have employees in a state banning abortion and you tell them your startup will support them as much as the law allows, this could create great peace of mind for employees. But if your startup does not operate in Ukraine or Russia, then denouncing Russia does little (and Russia does not care!)

3. Expertise. Do you have a deep understanding of the situation? It’s usually more complicated than it appears, especially at first. Once you speak out, you have painted yourself into a corner you will be forced to defend.

4. Precedence and equivalence. If you issue a statement about today’s news event, will you react to tomorrow’s event? Why not? Where do you draw the line?Someone will be offended that you spoke up about X but not Y.

5. Backlash. Are you ready to spend significant time engaging with those who disagree with you?It can get ugly quickly, and mistakes can be costly. Plus, the American public is tiring of business leaders commenting on the news.

6. Vicarious liability. Who are you speaking for? When you say, “Our startup denounces X”?Does the whole company denounce it? You don’t know, and probably not. Does the Leadership Team? They may feel pressured to support you. What you are really saying is, “I denounce X!” OK, great, then say it to your friends and family. Leave your startup to talk about business.

If your answers are “yes,” – then speak out.

If not, I recommend keeping quiet.

In my opinion, our job is to build great companies, not debate current events.

By not speaking out, you can say, “We don’t talk politics here.” You can shut down any two-sided arguments at work and say, “Let’s get back to work,”removing a big distraction. Remember when employees protested because Google was bidding for Pentagon contracts?

I realize that you will be challenged to make a statement, that, “Saying nothing is unacceptable/ complicit.” But whoever challenges you will only be satisfied if you support their view.

If you still want to speak out, I respect your choice. Some of you will be angry with me for writing this, and I accept that. I’m asking you to think carefully before you make a statement.

Announcing The Daily Bolster (You DO NOT want to miss this new Podcast)

I’m thrilled to announce The Daily Bolster — a quick-hitting podcast for startup leaders scaling their businesses. It’s the actionable insight you need to scale—in about 5 minutes. The first episode drops this coming Monday.

Our team created The Daily Bolster for folks in the startup world who — like me — want to hear from industry experts of all backgrounds, but don’t always have the time to listen to full length interviews, even at 2x speed (which usually ends up sounding like Alvin & The Chipmunks, anyway).

Instead, we’re getting straight to the point. GTTFP, as Brad says.

Starting next week, I will be joined every day by experienced operators and industry experts who share their real-world experiences and practical advice. Each day of the week, we’ll cover a different topic or theme:

- Monday: CEO Tips & Tricks

- Tuesday: Scaling Yourself & Your Team

- Wednesday: The View from the Board Room

- Thursday: Ask Bolster (this one will be more like 20-30 minutes to go deeper with someone)

The schedule is jam-packed with dynamic guests and punchy interviews. Whether you tune in every day, when you see a guest you’re especially interested in, or only on Tuesdays, we’re so excited to share these conversations with you.

In Week 1, I welcome Gainsight CEO Nick Mehta, board member extraordinaire and marketplace guru Cristina Miller, Union Square Ventures partner Fred Wilson, Helpscout CEO Nick Francis, and Bessemer Operating Partner and veteran CFO Jeff Epstein. They’ll share their practical advice and real-world experiences around professional development, company culture, startup strategy, and tips and tricks for executive growth.

Check out the season preview to learn more. You can also sign up for email notifications, to make sure you never miss an episode. The daily email will also include a pull quote and clips in case even the 5-minute version is too long for you.

You can subscribe to The Daily Bolster on these platforms: Bolster, YouTube, Apple, Google, Spotify, Amazon, Stitcher, Pandora, and Castbox, plus we’ll put each episode up on LinkedIn and Twitter. You should either follow me (T, LI) or Bolster (T, LI) on those to see the content.

Grow or Die

My cofounder Cathy wrote a great post on the Bolster blog back in January called Procrastinating Executive Development, in which she talks about the fact that even executives who appreciate the value of professional development usually don’t get to it because they’re too busy or don’t realize how important it is. I see this every day with CEOs and founders. Cathy had a well phrased but somewhat gentle ask at the end of her post:

My ask for all CEOs is this: give each of your executives the gift of feedback now, and hold each other accountable for continued growth and development to match the growth and development of your company.

Let me put it in starker terms:

Grow or Die.

Every executive, every professional, can scale further than they think is possible, and further than you think is possible. Most of us do have some ceiling somewhere…but it will take us years to find it (if we ever find it). The key to scaling is a growth mentality. You have to not just value development, you have to crave it, view it as essential, and prioritize it.

Startups are incredibly dynamic. You’re creating something out of nothing. Disrupting an industry. Revolutionizing something. Putting a dent in the universe. For a startup to succeed, it has to constantly put something in market, learn, calibrate, accelerate, maybe pivot, and most of all grow. How can a leader of a startup scale from one stage of life to the next without focusing on personal growth and development if the job changes from one quarter to the next?

I was lucky enough to have a great leadership team at my prior company, Return Path, over the course of 20 years. Within that long block of time with many executives, there was a particular period of time, roughly 2004-2012, that I jokingly refer to as the “golden age.” That’s when we grew the business from roughly $5mm in revenue to $50 or $60mm. The remarkable thing was that we executed that growth with the same group of 5-6 senior executives. A couple new people joined the team, and we struggled to get one executive role right, but by and large one core group took us from small to mid-sized. Why? We looked at each other — literally, in one meeting where we were talking about professional development — and said, “we have to commit to individual coaching, to team coaching, and to growth as leaders, or the company will outpace us and we’ll be roadkill.”

That set us on a path to focus on our own growth and development as leaders. We were constantly reading and sharing relevant articles, blog posts, and books. We engaged in a lot of coaching and development instruments like MBTI, TKI, and DISC. We learned the value of retrospectives, transparent 360s, and a steady diet of feedback. We challenged ourselves to do better. We worked at it. As one of the members of the Golden Age said of our work, “we went to the gym.”

The “Grow or Die” mantra is real. You can’t possibly be successful in today’s world if you’re not learning, if you don’t have a growth mentality. You are never the smartest person in the room. The minute you are convinced that you are…you’re screwed.

If you don’t believe me, look at the development of your business itself as a metaphor for your own development as a leader. What happens to your startup if it stops growing?

(You can find this post on the Bolster Blog here)

The quest for diversity in Tech leadership is stalling. Here’s why.

There’s been a growing cry for tech companies to add diversity to their leadership teams and boards, and for good reason. Those two groups are the most influential decision making bodies inside companies, and it’s been well documented that diverse teams, however you define diversity — diversity of demographics, thoughts, professional experience, lived experience — make better decisions.

Gender, racial, and ethnic representation in executive teams and in board rooms are not new topics. There’s been a steady drumbeat of them over the last decade, punctuated by some big newsworthy moments like the revelations about Harvey Weinstein and the tragic murder of George Floyd.

It’s also true that in people-focused organizations, and most tech companies claim to be just that, it’s beneficial to have different types of leaders in terms of role modeling and visibility across the company. As one younger woman on my team years ago said, “if you can see it…you can be it!”

My company Bolster is a platform for CEOs to efficiently build out their executive teams and boards. But while nearly every search starts with a diversity requirement, many don’t end that way.

Here’s why, and here’s what can be done about it.

For boards, the “why” is straightforward. Board searches are almost never a priority for CEOs. They’re viewed as optional. Bolster’s Board Benchmark study in 2021 indicated that only a third of private companies have independent directors at all;even later stage private companies only have independent directors two-thirds of the time. That same study indicated that 80% of companies had open Board seats. The comparable longitudinal study in 2022 indicated that the overwhelming majority of those open board seats were still open.

Independent directors are usually the key to diversity, as the overwhelming majority of founders and VCs are still white and male. It takes a lot of time and effort to recruit and hire and onboard new directors, and in the world of important versus urgent, it will always be merely important. Without prioritizing hiring independents, board diversity may be a lofty goal, but it’s also an empty promise. I wrote about my Rule of 1s here and in Startup Boards – I wish more CEOs and VCs took the practice of independent boards and board diversity seriously. The silver lining here is that when CEOs do end up prioritizing a search for an independent director, they are increasingly open to diverse directors, even if those people have less experience than they might want. That openness to directors who may never have been on a corporate board (but who are board-ready), who may be a CXO instead of a CEO, is key. Of the several dozen independent directors Bolster has helped match to companies in the past year, almost 70% of them are from demographic populations that are historically underrepresented in the boardroom.

Diversity is stalling for Senior Executive hiring for the opposite reason. Exec hires are usually urgent enough that CEOs prioritize them. And they frequently start their searches by talking about the importance of diversity. But Senior Executives are much more often hired for their resume than for competency or potential. Almost all executive searches start with some variation of this line, which I’m lifting directly from a prior post: “I want to hire the person who took XYZ Famous Company from where I am today to 10x where I am today.” The problem with that is simple. That person is no longer available to be hired. They have made a ton of money, and they have moved beyond that job in their career progression. So inevitably, the search moves on to look for the person who worked for that person, or even one more layer down…or the person who that person WAS before they took the job at XYZ Famous Company. Those people may or may not be easy to find or available, but they feel less risky. In the somewhat insular world of tech, those candidates are also far less likely to be diverse in background, experience, thought, or, yes, demographics.

Running a comprehensive executive search based on competencies, cultural fit, scale experience, and general industry or analogous industry experience is much harder. It takes time, patience, digging deeper to surface overlooked candidates or to check references, and probably a little more risk taking on the part of CEOs. And while CEOs may be willing to take some risk on a first-time independent director, fewer are willing to take a comparable level of risk on an unproven or less known executive hire.

For some CEOs, the answer is just to take more risk — or more to the point, recognize that any senior hire carries risk along a number of dimensions, so there’s no reason to prioritize your narrow view of resume pedigree over any critical vector. For others, the answer may be to bring the focus of diversity in senior hires to “second level” leaders like Managers, Directors, or VPs, where the perceived risk is lower, and the willingness to invest in training and mentorship is higher. Those people in turn can be promoted over time into more senior positions.

Not every executive or board hire has to be demographically diverse. Not every executive team or board has to have individual quotas for different identity groups, and diversity has many flavors to it. But without doing the work, tech CEOs will continue to bemoan the lack of diversity in their leadership ranks, and miss out on the benefits of diverse leadership, while not taking ownership for those efforts stalling.

Book Short: New to the Canon of Great CEO Books

Please go put Decide and Conquer: 44 Decisions that will Make or Break All Leaders by David Siegel on your reading list, or buy it. David’s book is up there on my list with Ben Horowitz’s The Hard Thing About Hard Things. It’s a totally different kind of book than Startup CEO, and in some ways a much better one in that there’s a great through-line or storyline, as David shares his leadership framework in the context of his journey of getting hired to replace founder Scott Heiferman as Meetup’s CEO after its acquisition by WeWork, including some juicy interactions with Adam Neumann, through the trials and tribulations of WeWork as a parent company, through COVID and its impact on an in-person meeting facilitator like Meetup, through to the sale of Meetup OUT of WeWork.

It’s hard to do the book justice with a quick write up. It’s incredibly concise. It’s clear. It’s witty. Most of all, it’s very human, and David shares a very human, common sense approach to leadership. I particularly like a device he uses to reinforce his main points and principles by bolding the key phrases every time they show up in the book: be kind, be confident, be bold, expand your options, focus on the long-term picture, be pragmatic, be honest, be speedy, do what’s right for the business, work for your people and they’ll work for you, be surprised only about being surprised. These all resonate with me so much.

One of the interesting things about the book is that David is a CEO, but not a founder (although he was sort of a re-founder in this case). A lot of CEO books talk about how to run a company, or give stories from the trials and tribulations thereof, but few focus on the elements of interviewing for the CEO job, or taking over the reins of a company in the midst of a turbulent flight. So the book is about getting the job, starting the job, doing a turnaround, leading a company through growth, a buy-out, and managing a company inside of another company. And because Meetup is such an iconic brand and business, it’s easy to understand a lot of the backdrop to David’s story.

I just met David for the first time a few weeks ago. We knew a bunch of people in common from his DoubleClick days. We instantly hit it off and traded copies of our books, and then were reading them at the same time trading emails about the parts that clicked. I just can’t recommend the book enough to any CEO or founder. In my view, it joins a pretty elite canon.

The Best Laid Plans, Part I

The Best Laid Plans, Part I

One of my readers asked me if I have a formula that I use to develop strategic plans. While every year and every situation is different, I do have a general outline that I’ve followed that has been pretty successful over the years at Return Path. There are three phases — input, analysis, and output. I’ll break this up into three postings over the next three weeks.

The Input Phase goes something like this:

Conduct stakeholder interviews with a few top clients, resellers, suppliers; Board of directors; and junior staff roundtables. Formal interviews set up in advance, with questions given ahead. Goal for customers: find out their view of the business today, how we’re serving them, what they’d like to see us do differently, what other products we could provide them. Goal for Board/staff: get their general take on the business and the market, current and future.

Conduct non-stakeholder interviews with a few industry experts who know the company at least a little bit. Goal: learn what they think about how we were doing today…and what they would do if they were CEO to grow the business in the future.

Re-skim a handful of classic business books and articles. Perennial favorite include Good to Great, Contrarian Thinking, and Crossing the Chasm.

Hold a solo visioning exercise. Take a day off, wander around Central Park. No phone, no email. Nothing but thinking about business, your career, where you want everything to head from a high level.

Hold senior staff brainstorming. Two-day off-site strategy session with senior team and maybe Board.

Next up: the Analysis Phase.

Momentum and Confidence: Everything Matters

As I stared at a dugout of dispirited 14 year old boys Saturday afternoon in our tournament championship game, I found myself talking to my fellow coach Mitch about a book I’d read a few years ago (turns out 14) called Confidence: How Winning Streaks and Losing Streaks Begin and End, written by HBS professor Rosabeth Moss Kantor. While that original blog post is pretty specific to something that was going on at that point in time in my prior company, the thinking in the book about momentum and the role it plays in our psychology, about sports, about business, and about life in general, is timeless.

Watching this team of teens go through ups and downs within an hour was incredibly stark and clear. In the first inning, we made three errors (just jitters from being in the championship…the Bulldogs are better than that!). Those opened the door for our opponent to post a few runs and take a quick lead. It was as if the wind had been taken out of our sails, as if all 11 kids just took a punch to the gut. They were shocked and pretty listless in the dugout, and nothing the coaches could do or say shook them out of it. They just *knew* they were going to lose, so why try? Their confidence was gone. It wasn’t until we staged our own big rally, later in the game, where all of a sudden, one, then two, then three base hits and the kids were going bananas, up at the fence of the dugout and screaming, cheering each other on and feeling all of a sudden like we could win the game.

The swing in momentum took about 5 minutes in each direction. And all that was involved was a couple quick negative/positive indicators/actions.

The bottom line is that we still lost the game 10-5. But the energy that came from a couple positive developments that stopped a downward spiral and started an upward one was palpable and instructive. As one of my other fellow coaches Jay said to the boys after the game, “Boys, the lesson from today is that Everything Matters. We lost 10-5, but when we were only down by 5 runs with the bases loaded, how much did we regret those couple of errors in the first inning? Without those, we would have been down by 2 runs with victory in reach.”

It’s the same in startups.

When you run a startup, you regularly take three punches to the gut in a row — a client cancels on you, you have a web site outage, an employee quits — and all of a sudden, you view the world through a dark lens of, as my long-time friend and Board member Scott Weiss used to say, WFIO, short for We’re F#%ked, It’s Over (pronounced whiff-ee-oh).

And then, the opposite happens, and it’s like the heavens part and the angels start singing a hallelujah chorus. You win a big new deal. You get unexpected positive press or a key blogger or tweet creates massive buzz for you. Your CFO pings you with the news that revenue is surprisingly high this month. WFIO is suddenly replaced with what I’ll call WGTWIA — We’re Going to Win It All (let’s pronounce it wig-twee-uh).

And what’s the difference? Probably nothing big. Probably a couple small things that just happened to break in the right or wrong direction at the right time. That call or email you decided not to return for a couple days until it was too late. That presentation you could have spent an extra 45 minutes perfecting instead of half-assing. That extra run through a new module of code you wrote to make sure it’s fully debugged. Just like a few silly errors in 14-year old baseball because you had the jitters early in a big game.

Everything Matters. In sports, in business, in life. Anything you think is a “throw away” can turn out in retrospect to have made the difference between winning and losing, between success and failure.

Normal People, Doing Wonderful Things

All three of our kids were at sleep-away camp for the past month, which was a first for us. A great, but weird, first! Our time “off” was bracketed by the absolutely amazing story of Come From Away. One of the first nights after the kids left, we saw the show on Broadway (Broadway show web site here, Wikipedia entry about the musical and story synopsis here). Then the last night before they came home, we saw Tom Brokaw’s ~45 minute documentary, entitled Operation Yellow Ribbon, which you can get to here or below.

https://youtu.be/jXbxoy4Mges

Come From Away is an amazing edge story to 9/11 that I’d never heard of before. It’s hard to believe there’s a 9/11 story that is this positive, funny, and incredibly heart-warming that isn’t better known. But thanks to the show, it is starting to be. It’s the story of the small town Gander in Newfoundland to which a large number of US-bound flights were diverted after the planes hit the World Trade Center and Pentagon. It’s the story of how a town of 9,000 people warmly absorbed over 7,000 stranded and upset passengers for 4-5 days before North American air traffic was flowing again following the attacks.

We were both on the edge of our seats for the entire 2 hour (with no intermission) show and were incredibly choked up the whole time…and had a hard time talking for a few minutes after. I’m sure for us, some of that is wrapped up in personal connection to 9/11, as our apartment was only 7 blocks north of the World Trade Center with a clear, 35th floor view of the site, and all that came with that. We didn’t lose anyone close to us in the attacks, but we knew dozens of second degree people lost; I had worked in one of the smaller World Trade Center buildings for a couple years earlier in my career; our neighborhood felt a bit like a military zone for a few weeks after the attacks; and we saw and smelled the smoke emanating from the site through Christmas of that year.

After seeing the show, we researched it a bit and found out just how close to real the portrayal was. So we watched the documentary. I always have a great association with Brokaw’s voice as the calm voice of objective but empathic journalism. He does such a great job of, to paraphrase him from the documentary, showing the juxtaposition of humanity at its darkest moment and its opposite.

Both the show and the documentary are worth watching, and I’m not sure the order of the two matters. But whatever order you take them in, put both on your list, even if you weren’t a New Yorker on 9/11.

My new Startup Board Mantra: 1-1-1

Last week, I blogged about Bolster’s Board Benchmark survey results, which really laid bare the lack of diversity on startup boards. There are signs that this is starting to change slowly — one big one is that of all the board searches we are running at Bolster, about ⅔ of them are open to taking on first-time directors; and almost all are committed to increasing diversity on their boards.

This is also something that I would expect to take some time to change. Boards are small. Independent seats aren’t necessarily easy to open up. Seats don’t turn over often. And they take a while to fill, as CEOs are thorough in their recruitment and selection process.

My new mantra for Startup Boards is simple: 1-1-1.

1 member of the management team.

Then 1 independent for every 1 investor.

Simply put, this means you should grow from having 1, to 2, to 3 independent directors as your board grows from 3, to 5, to 7 members.

Here are four tough conversations you may have to have along the way, with some suggestions on how to navigate them. All of these conversations need to come with a point of view of why independence and diversity matters to your company, a lot of empathy, and appreciation for the value the person brings to the table.

The conversation with your co-founder about only one founder/executive on the board. This one will be the most personally difficult, since you likely have a strong personal bond. Expect to hear things like “Aren’t we partners in this business?” and “How come my vote doesn’t count?” Just let your co-founder know that while of course they’re a key partner, the company has a limited number of board seats to fill — each one is a golden opportunity to get an outside perspective on your business and get really good mindshare of an industry expert and create a new brand ambassador. You already have 100% of the mindshare and ambassadorship your co-founder has to offer. You can make that person a board observer, you can make sure they’re in all the key board conversations, and you can even give the person some special voting right in your charter or by-laws if you need to. But do not put them on the board. It’s obviously easier to do this from the beginning as opposed to removing them from the board down the road, but at least try to have the conversation up front that someday, it’s going to happen (note this could be a different dynamic if the person is a founder but no longer active in the business).

The conversation with an existing VC about leaving the board to make room for new investors or an independent. This one will be less personally difficult but will require you to be very artful since the VC is likely contractually given a board seat – meaning you’ll have to get them to give it up voluntarily. You may also want to align with another VC on your board to help the conversation or process along. Depending on the circumstances at hand, your key points of logic could be one of the following: (1) you don’t own as high a percentage of the company as you once did, and I’d like to make room for the new lead investor to join the board without compromising our independents or making the board too big; or (2) I’d like to replace you with an independent director who brings operator perspective and comes from an underrepresented group – it’s important to me that we build a diverse board, and it’s not great that we have don’t have gender or race/ethnic diversity on our board in this day and age. As with a co-founder, you could change this person’s designation to a board observer so they’re still present for key conversations, you’re not changing their Information Rights, which are likely contractually given in your charter, and if required, you can give the person or firm some sort of special voting rights if there’s something they can no longer block (but which they have a contractual right to block) by losing their board vote.

The conversation with a new potential investor about not taking a board seat. If you have a big new lead investor writing a $40mm check into a growth round, you may not have a leg to stand on. But new investors who write smaller checks as you get larger, who might only be buying a 5-10% stake in the business…there, you might have some wiggle room to negotiate. Your best bet is to do it early in the process before you have a term sheet, and do it as an exploratory conversation. Otherwise, your talking points are the same as talking to an existing investor above. Investors are starting to realize the power of a diverse board, and may be open to this conversation. Some are making this a proactive practice, notably two of my long-time investors and directors Fred Wilson and Brad Feld (and some of their partners at Union Square Ventures and Foundry Group) — and those investors have also been willing to mentor the new, first time board members once they join.

The conversation with an existing independent director about leaving the board when their term is up. Perhaps you have an existing independent director who is not adding to the diversity of the board, but you already have a full board. Or perhaps your existing independent director isn’t doing a great job or has grown stale in the role. Once a director is fully vested, you have an easy opportunity to thank them graciously and publicly for their service, extend their option exercise period multiple years, and affirm that they’ll still take your call if you need help on something. You should set this expectation up front when you give the director their initial grant. If they ask why you’re not renewing them, you can simply say something like “We’d like to add some fresh outside perspective to the team.” One thing to think about, particularly for early stage companies, is only giving new directors a 1 or 2-year vest on their first option grant, so you can make sure they’re a high value director…and so you can have the option of an easy exit (or re-up) in a shorter period of time than a traditional 4-year vest.

The net of it is that as CEO of a venture-backed company, you wield an enormous amount of (mostly soft) power around the composition of your board – probably a lot more than you think. You just have to wield that power gently and focus on the importance of building a diverse board in terms of both experience and demographics.

The Startup Ecosystem Needs More Independent Board Members – That’s the Clearest Path to Having Better and More Diverse Boards

I love having independent directors on my Board. They are a great third leg of the stool alongside a CEO/Founder and VCs. They provide the same kind of pattern matching and outside point of view as VCs — but from a completely different perspective, that of an operator or industry expert. The good ones are CEOs or CXOs who aren’t afraid to challenge you. Equally important, they’re not afraid to challenge your VCs. At Return Path, I always had 2 or 3 independent directors at any given time to balance out VCs, and some have become great long term friends like Scott Petry, Jeff Epstein, and Scott Weiss. At Bolster, we’re already having a great experience with our first independent, Cristina Miller, and we’re about to add a second independent. And I’ve served as an independent director multiple times.

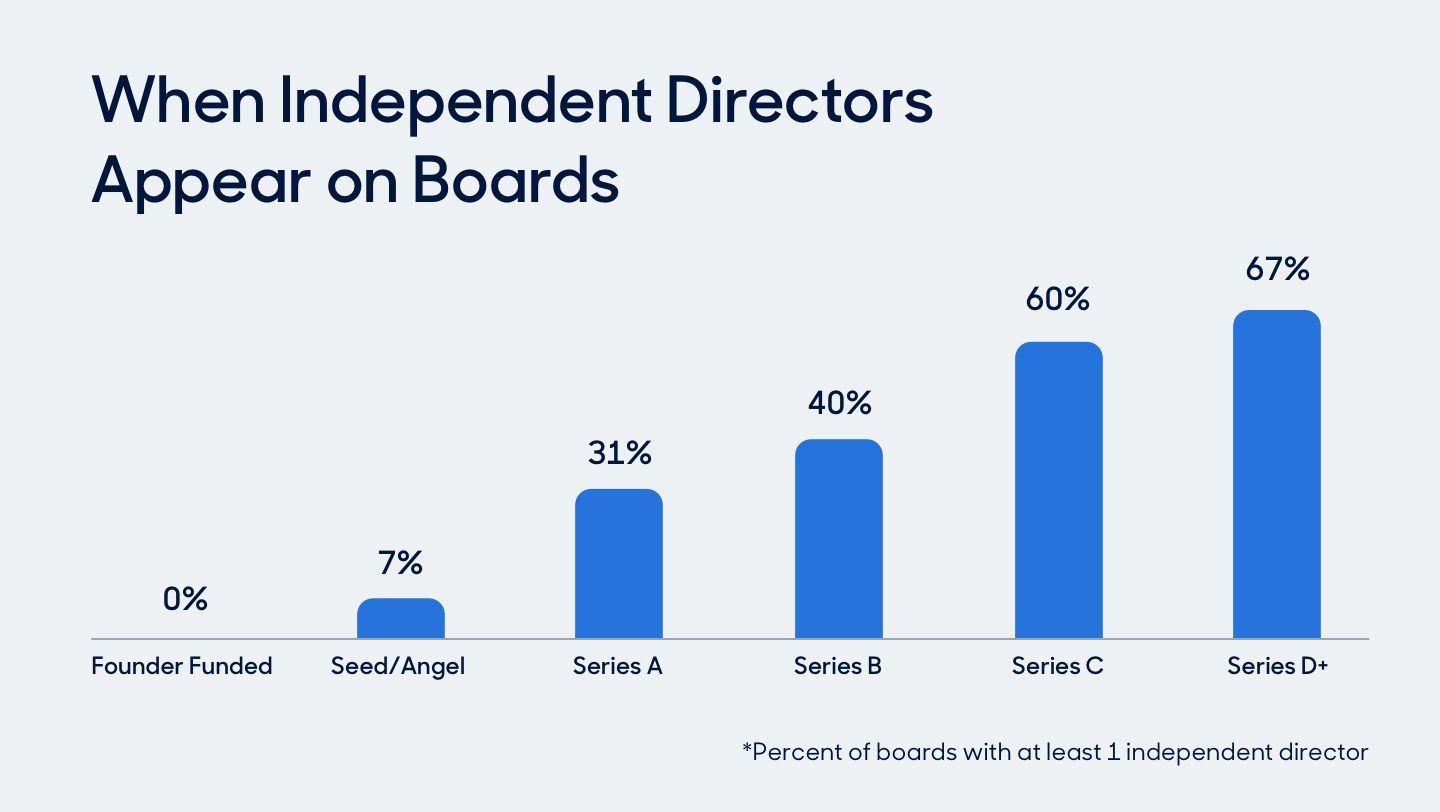

So as you can imagine, I was shocked by one of the headlines coming out of the Board Benchmark study we ran at Bolster across 250+ clients (detailed blog post with a bunch of charts and graphs) that only ⅓ of companies in the study have any independent directors. Even larger companies at the Series C and D levels only have independent directors 60% and 67% of the time. What a missed opportunity for so many companies.

Less surprising, though still sobering, were the numbers on diversity that came out of the study. 79% of the directors in the sample are white. 86% are men. 43% of boards are completely racially homogenous (most all-white) while 80% are mostly racially homogeneous (meaning only one diverse member); 56% are gender homogenous (most all men), while 87% are mostly gender homogenous (only one female). For an industry that is spending a lot of time talking about diversity in leadership teams and on boards, that’s disappointing.

Here’s the linkage of the two topics: The solution to the board diversity problem lies in having more independent directors, since management and VC board seats are often both “fixed” and non-diverse. Independent seats are the easiest to fill with diverse candidates. Conveniently, more independent directors also leads to higher quality boards.

In partnership with some DEI experts, our study also includes some suggested actionable tips for CEOs and board leaders, which I encourage you to read. There are really three simple (IMO) steps to having more diverse boards, and there is some good news in the Bolster study around these points:

- Add independent director seats. 50% of the companies in the survey either have or expect to have an independent board seat open within 12 months. That’s a good start, but honestly, I can’t imagine running any board without at least 1-2 independent directors (up to 3-4 for larger companies), starting on Day 1. Given that only ⅓ of companies in the sample have any independent board members at all, the 50% number feels quite low.

- Open the recruiting funnel to include first-time directors. Historically, companies have mainly targeted current or former CEOs or people who have board experience to be independent directors. That is a recipe to perpetuate having mostly white male board members. But Bolster has done a few dozen board searches so far, and 66% of those clients have expressed a willingness to take on first-time directors, as long as they are “board ready,” which we define as having been on any kind of board, not just a corporate board; having reported to a founder or CEO and had regular interaction with and presentations to a board; or having significant experience as a formal or informal advisor. Once you widen the funnel to include all candidates who meet those criteria, you can very easily have a diverse slate of highly qualified candidates. Bolster is a great source of these candidates (this is a real focal point for our business), but there are plenty of other online or search firm sources as well.

- Have the courage to limit the number of management/investor board members. Whether or not you can add independent board members may be a function of how many seats you have to play with in your corporate charter. Of course, you can add seats indefinitely, but there’s no reason to have a 7-person board for your Series A company. My rule of thumbs on this are simple: (a) Only one founder member of the management team on the Board – more than that is a waste of a valuable board slot; and (b) VCs should always be less than 50% of your board members, so as new ones roll on, old ones should roll off – or add a VC and an independent at the same time. Both of these take serious effort and courage, both are worth it, and both probably merit a longer blog post someday.

The Board Benchmark study also had a wealth of information about compensation for independent directors — cash vs. stock, what kind of stock, how much stock, vesting and acceleration provisions.

Here’s a Slideshare of the full survey results, in case this and/or the Bolster blog link isn’t detailed enough for you:

If you’re interested in learning more, the survey is free to take and all the granular results (including comp benchmarks) are available to benchmark against your company if you take it. Just email me if you’re interested at [email protected].