Startup CXO: the Sequel to Startup CEO

As I finished up my work on the Second Edition of Startup CEO: A Field Guide to Scaling Up Your Business and started working on a new startup, my colleagues and I started envisioning a new book as a sequel or companion to Startup CEO that is going to be published on June 9 with our same publisher, Wiley & Sons. The book is called Startup CXO: A Field Guide to Scaling Up Your Company’s Critical Functions and Teams.

Simply put, the first book left me with the nagging feeling that it wasn’t enough to only help CEOs excel, because starting and scaling a business is a collective effort. What about the other critical leadership functions that are needed to grow a company? If you’re leading HR, or Finance, or Marketing, or any key function inside a startup, what resources are available to you? What should you be thinking about? What does ‘great’ look like? What challenges lurk around the corner as you scale your function that you might not be focused on today? If you’re a CEO who has never managed all these functions before, what should you be looking for when you hire and manage all these people? If you’re an aspiring executive, from entry-level to manager to director, what do you need to think about as you grow your career and develop your skills?

Startup CXO is a “book of books,” with one section for each major function inside a company. Each section is be composed of 15-20 discrete short chapters outlining the key “playbooks” for each functional role in the company – Chief People Officer, Chief Financial Officer, Chief Marketing Officer, Chief Revenue Officer, etc., hence the title Startup CXO – which is a generally accepted label in the startup ecosystem for “Chief ____ Officer.”

Here are the front and back covers of the book, with some great endorsements we’re so proud of on the back.

This is an important topic to write about at this particular time because America’s “startup revolution” continues to gather steam. There are only increasing numbers of venture capital investors, seed funds, and accelerators supporting increasing numbers of entrepreneurial ventures. While there are a number of books in the marketplace about CEOs and leadership, and some about individual functional disciplines (lots of books about the topic of Sales, the topic of Product Development), there are very few books that are practical how-to guides for any individual function, and NONE that wrap all these functions into a compendium that can be used by a whole startup executive team. Very simply, each section of this book serves as a how-to guide for a given executive, and taken together, the book will be a good how-to guide for startup executive teams in general.

Startup CXO has my name on it as principal author, and I’m writing parts of it, but I can’t even pretend to write it on my own, so the book has a large number of contributors who have the experience, credibility, and expertise to share something of value with others in their specific functional disciplines — most of my Bolster co-founders are writing sections, and the others are being written by former Return Path executive colleagues — Jack Sinclair, Cathy Hawley, Ken Takahashi, Anita Absey, George Bilbrey, Dennis Dayman, Nick Badgett, Shawn Nussbaum, and Holly Enneking.

Startup CXO is also pretty closely related to Bolster’s business, since we are in the business of helping assess and place on-demand CXO talent, and as such, the final section of the book has a series of chapters written by Bolster members who are career Fractional Executives about their experience as a Fractional CXO.

The book is available for pre-order now at Amazon and Barnes & Noble.

Oh, and stay tuned for a third book in the series (kind of) due out late this year. More on that over the summer as the project takes shape!

How to get the most out of working with a CEO Mentor or CEO Coach

(This is the third in a series of three posts on this topic.)

In previous posts (here, here) , I talked about the difference between Mentors and Coaches and also how to select the right ones for you. Once you’ve selected a Mentor or Coach, here are some tips to get the most out of your engagement.

Starting to work with a CEO Mentor is fairly easy. Give them some materials to help understand your business, and then come prepared to every session with a list of 1-2 topics that are keeping you up at night where you want to benefit from the person’s experience.

Kicking off a CEO Coach engagement is more in-depth. I always recommend starting to work with a CEO Coach by doing a DEEP 360. Not one that’s a bland anonymous survey instrument, but one that involves the Coach doing 15-20 in-depth interviews with a wide range of people from team to Board to others in the organization to people you’ve worked with outside the organization, including some non-professional contacts. Let the Coach really learn about you from others. The reason for this is that, although you may have an area of development that you want to focus on (like I did when I met Marc), you may actually need help in other areas a lot more acutely.

In general, I’d say these are a few good rules of thumb for getting the most out of your Coach or Mentor relationship and sessions of work together:

- Do your homework. If you have an assignment to read an article, take a survey, or just write something up, either do it or cancel the next meeting or it will be a waste of everyone’s time

- Be present. Step away from your desk. Turn off email. Silence your phone. These are some of the most valuable times for your own personal development and growth, and they are few and far between when you get to be a CEO. Treasure them

- Bring your whole self. Even if your coach is a full 5 on the Shrink-to-Management Consultant scale I mentioned above, people are people, and you’re no exception. You have a bad day at home — it will show through at work and it will impact your Coach conversations (maybe less so your Mentor ones). Don’t ignore it. Mention it up front

- Don’t bullshit. You know when you’re wrong about something or have made a mistake. You may or may not be great about admitting it publicly, or even admitting it to yourself. ADMIT IT TO YOUR COACH. Otherwise, why bother having one?

- Encourage primary data collection. The biggest place I’ve seen coaching relationships fail is when the Coach or Mentor only has access to a single point of information about what’s happening in the organization — you. Even if you’re not in full-on 360 mode, encourage your Coach or Mentor to spend time with others in the organization or on your board here and there and have a direct line of communication with them. If they don’t and all they’re working off is your perspective on situations, their output will be severely limited or subject to their own conjecture. Especially if you can’t get the prior bullet point right (garbage in, garbage out!)

- Make it your agenda even if it means changing on the fly. You may be working on an analysis of your team’s Myers-Briggs profile with your Coach – and that’s the topic of your next meeting – but right before the meeting, you learn that one of your CXOs is resigning. Change the agenda. It’s ok. It’s your time, make it work for you

- Learn to fish. At the end of the day, a good CEO Coach should offer you ways of thinking about things, ways of being, ways of learning in your organization, processes to give you the ability to do some elements of this by yourself – not just answering questions for you. Sports trainers are useful for an athlete’s entire career to push them harder in workouts, but they also teach athletes how to work out on their own

- Reality check the advice. Make sure to test the strategies that Coaches or Mentors are giving you against your organization. All strategies won’t work in all organizations. These conversations should offer a variety of strategies – you can pick one or pick none and do something totally different. The value isn’t in being told what to do, it is in going through the process of deciding what to do for YOUR organization with some expert inputs and reflections on other experiences

- Close the loop. I’ve written before about how to solicit feedback as a CEO. To make sure your coaching work is effective, be sure to include feedback loops with your key stakeholders (team and board) on the things you’re working on with your CEO Coach

It’s worth the money. CEO Coaches can be really expensive. Like really, really expensive. $500-1,500/hour expensive. CEO Mentors can be free and informal, but sometimes they charge as well or ask for advisor equity grants. Even if you have a thin balance sheet, don’t be shy about adding the expense, and you shouldn’t pay for this personally. Adding 10-20% to the cost of your compensation will potentially make you twice as effective a CEO. If your board doesn’t support the expense…well, then you may have a different problem.

There’s a lot written publicly about this topic. Jason Lemkin at SaaStr has a particularly good post that really puts a fine point on it. And the coaching team at Beyond CEO Coaching a new boutique coaching firm specializing in coaching black CEOs, writes in “Who are you not to be great?”, “You can play it safe and reduce your risks and likely the rewards, or you can go big. We at Beyond CEO Coaching want to help you to go big.”

By the way, this entire framework applies to non-CEOs as well. Every professional would benefit from having a Coach and a Mentor in their life, even if those aren’t paid consultants but more senior colleagues or members of the company’s People Team. Sometimes a Mentor and a Coach are one and the same…sometimes they are not.

Thanks to a large number of Bolster members I know personally who are CEO Coaches and Mentors for reviewing these posts — Chad Dickerson, Bob Cramer, Tim Porthouse, Marc Maltz, Lynne Waldera, Dave Karnstedt, and Mariquita Blumberg.

My new Startup Board Mantra: 1-1-1

Last week, I blogged about Bolster’s Board Benchmark survey results, which really laid bare the lack of diversity on startup boards. There are signs that this is starting to change slowly — one big one is that of all the board searches we are running at Bolster, about ⅔ of them are open to taking on first-time directors; and almost all are committed to increasing diversity on their boards.

This is also something that I would expect to take some time to change. Boards are small. Independent seats aren’t necessarily easy to open up. Seats don’t turn over often. And they take a while to fill, as CEOs are thorough in their recruitment and selection process.

My new mantra for Startup Boards is simple: 1-1-1.

1 member of the management team.

Then 1 independent for every 1 investor.

Simply put, this means you should grow from having 1, to 2, to 3 independent directors as your board grows from 3, to 5, to 7 members.

Here are four tough conversations you may have to have along the way, with some suggestions on how to navigate them. All of these conversations need to come with a point of view of why independence and diversity matters to your company, a lot of empathy, and appreciation for the value the person brings to the table.

The conversation with your co-founder about only one founder/executive on the board. This one will be the most personally difficult, since you likely have a strong personal bond. Expect to hear things like “Aren’t we partners in this business?” and “How come my vote doesn’t count?” Just let your co-founder know that while of course they’re a key partner, the company has a limited number of board seats to fill — each one is a golden opportunity to get an outside perspective on your business and get really good mindshare of an industry expert and create a new brand ambassador. You already have 100% of the mindshare and ambassadorship your co-founder has to offer. You can make that person a board observer, you can make sure they’re in all the key board conversations, and you can even give the person some special voting right in your charter or by-laws if you need to. But do not put them on the board. It’s obviously easier to do this from the beginning as opposed to removing them from the board down the road, but at least try to have the conversation up front that someday, it’s going to happen (note this could be a different dynamic if the person is a founder but no longer active in the business).

The conversation with an existing VC about leaving the board to make room for new investors or an independent. This one will be less personally difficult but will require you to be very artful since the VC is likely contractually given a board seat – meaning you’ll have to get them to give it up voluntarily. You may also want to align with another VC on your board to help the conversation or process along. Depending on the circumstances at hand, your key points of logic could be one of the following: (1) you don’t own as high a percentage of the company as you once did, and I’d like to make room for the new lead investor to join the board without compromising our independents or making the board too big; or (2) I’d like to replace you with an independent director who brings operator perspective and comes from an underrepresented group – it’s important to me that we build a diverse board, and it’s not great that we have don’t have gender or race/ethnic diversity on our board in this day and age. As with a co-founder, you could change this person’s designation to a board observer so they’re still present for key conversations, you’re not changing their Information Rights, which are likely contractually given in your charter, and if required, you can give the person or firm some sort of special voting rights if there’s something they can no longer block (but which they have a contractual right to block) by losing their board vote.

The conversation with a new potential investor about not taking a board seat. If you have a big new lead investor writing a $40mm check into a growth round, you may not have a leg to stand on. But new investors who write smaller checks as you get larger, who might only be buying a 5-10% stake in the business…there, you might have some wiggle room to negotiate. Your best bet is to do it early in the process before you have a term sheet, and do it as an exploratory conversation. Otherwise, your talking points are the same as talking to an existing investor above. Investors are starting to realize the power of a diverse board, and may be open to this conversation. Some are making this a proactive practice, notably two of my long-time investors and directors Fred Wilson and Brad Feld (and some of their partners at Union Square Ventures and Foundry Group) — and those investors have also been willing to mentor the new, first time board members once they join.

The conversation with an existing independent director about leaving the board when their term is up. Perhaps you have an existing independent director who is not adding to the diversity of the board, but you already have a full board. Or perhaps your existing independent director isn’t doing a great job or has grown stale in the role. Once a director is fully vested, you have an easy opportunity to thank them graciously and publicly for their service, extend their option exercise period multiple years, and affirm that they’ll still take your call if you need help on something. You should set this expectation up front when you give the director their initial grant. If they ask why you’re not renewing them, you can simply say something like “We’d like to add some fresh outside perspective to the team.” One thing to think about, particularly for early stage companies, is only giving new directors a 1 or 2-year vest on their first option grant, so you can make sure they’re a high value director…and so you can have the option of an easy exit (or re-up) in a shorter period of time than a traditional 4-year vest.

The net of it is that as CEO of a venture-backed company, you wield an enormous amount of (mostly soft) power around the composition of your board – probably a lot more than you think. You just have to wield that power gently and focus on the importance of building a diverse board in terms of both experience and demographics.

The Startup Ecosystem Needs More Independent Board Members – That’s the Clearest Path to Having Better and More Diverse Boards

I love having independent directors on my Board. They are a great third leg of the stool alongside a CEO/Founder and VCs. They provide the same kind of pattern matching and outside point of view as VCs — but from a completely different perspective, that of an operator or industry expert. The good ones are CEOs or CXOs who aren’t afraid to challenge you. Equally important, they’re not afraid to challenge your VCs. At Return Path, I always had 2 or 3 independent directors at any given time to balance out VCs, and some have become great long term friends like Scott Petry, Jeff Epstein, and Scott Weiss. At Bolster, we’re already having a great experience with our first independent, Cristina Miller, and we’re about to add a second independent. And I’ve served as an independent director multiple times.

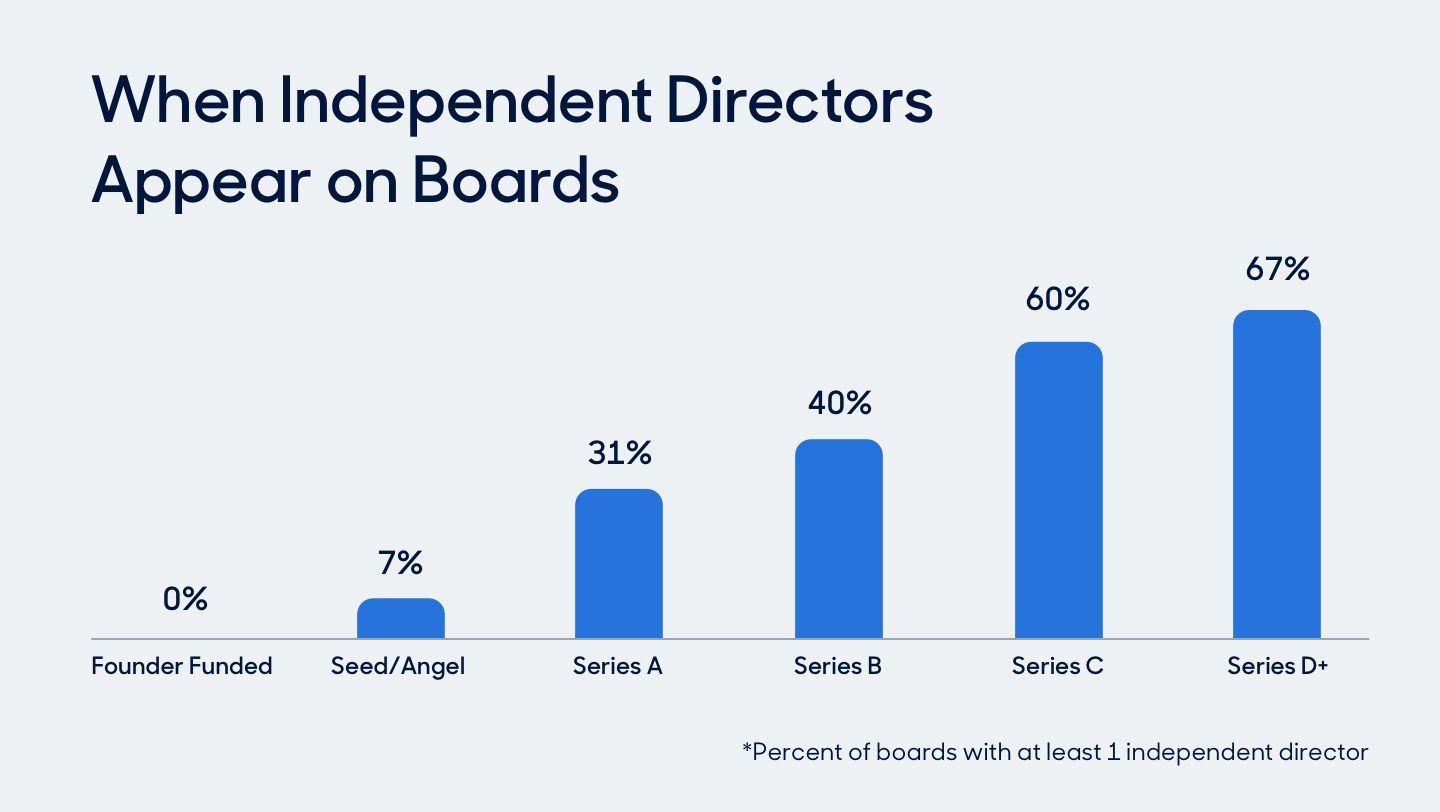

So as you can imagine, I was shocked by one of the headlines coming out of the Board Benchmark study we ran at Bolster across 250+ clients (detailed blog post with a bunch of charts and graphs) that only ⅓ of companies in the study have any independent directors. Even larger companies at the Series C and D levels only have independent directors 60% and 67% of the time. What a missed opportunity for so many companies.

Less surprising, though still sobering, were the numbers on diversity that came out of the study. 79% of the directors in the sample are white. 86% are men. 43% of boards are completely racially homogenous (most all-white) while 80% are mostly racially homogeneous (meaning only one diverse member); 56% are gender homogenous (most all men), while 87% are mostly gender homogenous (only one female). For an industry that is spending a lot of time talking about diversity in leadership teams and on boards, that’s disappointing.

Here’s the linkage of the two topics: The solution to the board diversity problem lies in having more independent directors, since management and VC board seats are often both “fixed” and non-diverse. Independent seats are the easiest to fill with diverse candidates. Conveniently, more independent directors also leads to higher quality boards.

In partnership with some DEI experts, our study also includes some suggested actionable tips for CEOs and board leaders, which I encourage you to read. There are really three simple (IMO) steps to having more diverse boards, and there is some good news in the Bolster study around these points:

- Add independent director seats. 50% of the companies in the survey either have or expect to have an independent board seat open within 12 months. That’s a good start, but honestly, I can’t imagine running any board without at least 1-2 independent directors (up to 3-4 for larger companies), starting on Day 1. Given that only ⅓ of companies in the sample have any independent board members at all, the 50% number feels quite low.

- Open the recruiting funnel to include first-time directors. Historically, companies have mainly targeted current or former CEOs or people who have board experience to be independent directors. That is a recipe to perpetuate having mostly white male board members. But Bolster has done a few dozen board searches so far, and 66% of those clients have expressed a willingness to take on first-time directors, as long as they are “board ready,” which we define as having been on any kind of board, not just a corporate board; having reported to a founder or CEO and had regular interaction with and presentations to a board; or having significant experience as a formal or informal advisor. Once you widen the funnel to include all candidates who meet those criteria, you can very easily have a diverse slate of highly qualified candidates. Bolster is a great source of these candidates (this is a real focal point for our business), but there are plenty of other online or search firm sources as well.

- Have the courage to limit the number of management/investor board members. Whether or not you can add independent board members may be a function of how many seats you have to play with in your corporate charter. Of course, you can add seats indefinitely, but there’s no reason to have a 7-person board for your Series A company. My rule of thumbs on this are simple: (a) Only one founder member of the management team on the Board – more than that is a waste of a valuable board slot; and (b) VCs should always be less than 50% of your board members, so as new ones roll on, old ones should roll off – or add a VC and an independent at the same time. Both of these take serious effort and courage, both are worth it, and both probably merit a longer blog post someday.

The Board Benchmark study also had a wealth of information about compensation for independent directors — cash vs. stock, what kind of stock, how much stock, vesting and acceleration provisions.

Here’s a Slideshare of the full survey results, in case this and/or the Bolster blog link isn’t detailed enough for you:

If you’re interested in learning more, the survey is free to take and all the granular results (including comp benchmarks) are available to benchmark against your company if you take it. Just email me if you’re interested at [email protected].

Should CEOs wade into Politics?

This question has been on my mind for years. In the wake of Georgia passing its new voting regulations, a many of America’s large company CEOs are taking some kind of vocal stance (Coca Cola) or even action (Major League Baseball) on the matter. Senate Majority Leader Mitch McConnell told CEOs to “stay the hell out of politics” and proceeded to walk that comment back a little bit the following day. The debate isn’t new, but it’s getting uglier, like so much of public discourse in America.

Former American Express CEO Harvey Golub wrote an op-ed earlier this week in The Wall Street Journal entitled Politics is Risky Business for CEOs (behind a paywall), the subhead of which sums up what my point of view has always been on this topic historically — “It’s imprudent to weigh in on issues that don’t directly affect the company.” His argument has a few main points:

- CEOs may have opinions, but when they speak, they speak for and represent their companies, and unless they’re speaking about an issue that effects their organization, they should have Board approval before opening their mouths

- Whatever CEOs say about something political will by definition upset many of their employees and customers in this polarized environment (I agree with this point a lot of the time and wrote about it in the second edition of Startup CEO)

- There’s a slippery slope – comment on one thing, you have to comment on all things, and everything descends from there

So if you’re with Harvey Golub on this point, you draw the boundaries around what “directly affects” the company — things like employment law, the regulatory regime in your industry, corporate tax rates, and the like.

The Economist weighed in on this today with an article entitled CEO activism in America is risky business (also behind a paywall, sorry) that has a similar perspective with some of the same concerns – it’s unclear who is speaking when a CEO delivers a political message, messages can backfire or alienate stakeholders, and it’s unclear that investors care.

The other side of the debate is probably best represented by Paul Polman, longtime Unilever CEO, who put climate change, inequality, and other ESG-oriented topics at the center of his corporate agenda and did so both because he believed they were morally right AND that they would make for good business. Unilever’s business results under Polman’s leadership were transformational, growing his stock price almost 300% in 10 years and outpaced their peers, all as a “slow growth” CPG company. Paul’s thinking on the subject is going to be well documented in his forthcoming book, Net Positive: How Courageous Companies Thrive by Giving More Than They Take, which he is co-authoring with my good friend Andrew Winston and which will come out later this year.

While I still believe that on a number of issues in current events, CEOs face a lose-lose proposition by wading into politics, I’m increasingly moving towards the Paul Polman side of the debate…but not in an absolute way. As I’ve been wrestling with this topic, at first, I thought the definition of what to weigh in on had to come down to a definition of what is morally right. And that felt like I was back in a lose-lose loop since many social wedge issues have people on both sides of them claiming to be morally right — so a CEO weighing in on that kind of issue would be doomed to alienate a big percentage of stakeholders no matter what point of view he or she espouses.

But I’m not sure Paul and Andrew are absolutists, and that’s the aha for me. I believe their point is that CEOs need to weigh in on the things that directly affect their companies AND ALSO weigh in on the things that indirectly affect their companies.

So if you eliminate morality from the framework, where do you draw the line between things that have indirect effects on companies and which ones do not? If I back up my scope just a little bit, I quickly get to a place where I have a different and broader definition of what matters to the functioning of my industry, or to the functioning of commerce in general without necessarily getting into social wedge issues. For want of another framework on this, I landed on the one written up by Tom Friedman and Michael Mandelbaum in That Used to be Us: How America Fell Behind in the World It Invented and How We Can Come Back, which I summarized in this post a bunch of years ago — that America has lost its way a bit in the last 20-40 years because we have strayed from the five-point formula that has made us competitive for the bulk of our history:

- Providing excellent public education for more and more Americans

- Building and continually modernizing our infrastructure

- Keeping America’s doors to immigration open

- Government support for basic research and development

- Implementation of necessary regulations on private economic activity

So those are some good things to keep in mind as indirectly impacting commercial interests and American competitiveness in an increasingly global world, and therefore are appropriate for CEOs to weigh in on. And yes, I realize immigration is a little more controversial than the other topics on the list, but even most of the anti-immigration people I know in business are still pro legal immigration, and even in favor of expanding it in some ways.

And that brings us back to Georgia and the different points of view about whether or not CEOs should weigh in on specific pieces of legislation like that. Do voting rights directly impact a company’s business? Not most companies. But what about indirect impact? I believe that having a high functioning democracy that values truth, trust, and as widespread legal voter participation as possible is central to the success of businesses in America, and that at the moment, we are dangerously close to not having a high functioning democracy with those values.

I have not, as Mitch McConnell said, “read the whole damn bill,” but it doesn’t take a con law scholar to note that some pieces of it which I have read — no giving food or water to people in voting lines, reduced voting hours, and giving the state legislature the unilateral ability to fire or supersede the secretary of state and local election officials if they don’t like an election’s results — aren’t measures designed to improve the health and functioning of our democracy. They are measures designed to change the rules of the game and make it harder to vote and harder for incumbents to lose. That is especially true when proponents of this bill and similar ones in other states keep nakedly exposing the truth when they say that Republicans will lose more elections if it’s easier for more people to vote, instead of thinking about what policies they should adopt in order to win a majority of all votes.

And for that reason, because of that bill, I am moving my position on the general topic of whether or not CEOs should wade into politics from the “direct impact” argument to the “indirect impact” one — and including in that list of indirect impacts improving the strength of our democracy by, among other things, making it as easy as possible for as many Americans to vote as possible and making the administration of elections as free as possible from politicians, without compromising on the principle of minimizing or eliminating actual fraud in elections, which by all accounts is incredibly rare anyway.

How to Select a CEO Mentor or CEO Coach

(This is the second in a series of three posts on this topic.)

In a previous post, I shared the difference between CEO Mentors and CEO Coaches. I’ll share with you here how to select the Mentors and Coach who are right for you. First, you need to find candidates. Whether you’re talking about CEO Coaches or CEO Mentors or both, getting referrals from trusted sources is the best way to go about this. Those trusted sources could be your VC or independent board members, friends, fellow CEOs — or of course Bolster, where we have a significant number of Coaches and Mentors and have made it our business to vet and vouch for them.

Selecting a CEO Mentor is literally like selecting a teacher but at a vocational school, not at a research university. You want to select someone who has done something several times or for several years; done it really well; documented it in some organized way (at least mentally); and can articulate what they did, why, what worked and what didn’t, and help you apply it to your situation. Do you want to be taught how to be an electrician by someone with a PhD in Electrical Engineering, or by someone who has been a master electrician for 20 years? Fit matters mostly around values. It’s hard to get advice from someone whose values are quite different, as their experiences and their metrics for what did and didn’t work won’t apply well to yours. Fit is a lot less around personality, although you have to be able to get along and communicate with the person at a basic level Find someone with the right experience set that you can learn from RIGHT NOW. Or at least this year. Maybe the person is the right mentor next year, maybe not. Depends on what you need. For example, if you’re running a $10mm revenue DTC company, find someone who has scaled a company in the DTC or adjacent eCommerce space to at least $25-50mm.

Although I’ve been very international in getting mentoring as a CEO over the years, I’ve never hired a formal CEO Mentor. Several people, from my dad to my independent directors to the members of my CEO Forum have played that role for me at different times over the years. Knowing what I know now, I’m working with CEO Mentors who have experience with talent marketplaces at different scale, since this is a new industry for me.

Selecting a CEO Coach is different. I got lucky in my selection of a CEO Coach almost 20 years ago. My board member Fred Wilson told me I needed to work with one, I naively rolled my eyes and said ok, he introduced me to Marc Maltz, I told Marc something like “I need a coach because clearly I need to learn how to manage my Board better,” and for some reason, he decided to take the assignment. I got lucky because Marc ended up being exactly the right coach for me, going on 20 years now, but I didn’t know that at the time.

Selecting a CEO Coach is all about who you “click with” personality wise, and what you need in order to be pushed to grow developmentally. CEO Coaches come on a spectrum ranging from what I would call “Quasi-Psychiatrist” on one end, to “Quasi-Management Consultant” on the other end. The former can be incredibly helpful — just note that you will find yourself talking about your thoughts, feelings, and family of origin a fair bit as a means of uncovering problems and solutions. The latter can be helpful as well — just note that you will find yourself talking about business strategy and having someone hold up the proverbial mirror so you can see you the way other people see you as the CEO, quite a bit. There is no right or wrong universal answer here to what makes someone the right choice for you. For me, if one end of the spectrum is a 1 and the other is a 5, I prefer working with people who are in the 3-4 range.

Therapy and coaching are different, though. A good CEO Coach who is a 1 will refer clients to therapy if they see the need. While coaching can “feel” therapeutic, and actually may be therapeutic, it is not a replacement for therapy. The differences between the 1s and the 5s are not just style differences but also really what you want the content of the coaching to be. A 1 is going to help you discover and drive to your leadership style. A 5 is going to help you align those decisions to how you actually act, what approaches you bring to the organization and how you address challenges. Some CEO Coaches can move back and forth between all of these, but knowing where you sit with your needs relative to the coach’s natural style when you pick a coach is critical.

I know CEOs who have shown tremendous growth as humans and leaders with Coaches who are 1s and Coaches who are 5s. A good CEO Coach is someone you can work with literally forever.

I always encourage CEOs to interview multiple Coaches and specifically ask them what their coaching process is like and what their coaching philosophy is. How do they typically start engagements. How structured or unstructured are they in their work? Check references and ask some of their other CEO clients what it’s been like to work with them. This is all true to a much lesser extent with Mentors. In both cases, you should probably do a test session or two before signing up for a longer-term engagement. You wouldn’t buy a car without taking it for a test drive. This is an even more consequential decision.

And in both cases, there should be no ego in the process. You should never feel like you’re being sold by a CEO Coach or CEO Mentor. And they shouldn’t feel hurt by you picking someone else, either. Alignment and chemistry are so critical – there is no way to have that with every person, and the good professionals in this industry should know that.

The bottom line is that hiring a CEO Mentor is low risk. If it’s not working out, you stop engaging. Hiring a CEO Coach is a longer-term decision, and it’s worth having couple of sessions with a coach before making the commitment.

Next post in the series coming: How to get the most out of working with a CEO Mentor or CEO Coach

The Difference Between a CEO Coach and a CEO Mentor and Why Every CEO Needs Both

(This is the first in a series of three posts on this topic.)

Harry Potter was lucky. He had, in Albus Dumbledore, the ultimate wise elder, in his corner. Someone who could teach him how to be a better human being (er, wizard), how to be more proficient with his wand and spells, how to think strategically and defeat the bad guys.

All of us would benefit from having an Albus Dumbledore in our lives. But most of us don’t — and most of the people we’d call on to be that wise elder in our corner aren’t capable of the full range of advice and counsel that Dumbledore is.

Why work with a Coach or a Mentor? I’ll start this post with a quick argument in favor of CEO Coaches and Mentors (sometimes called Advisors). Even as a 20-something first-time CEO years ago, I was deeply skeptical of the value of a Coach, but that was in 1999 or 2000 when coaches weren’t so commonplace. Now that their value seems much more obvious, and there are so many amazing Mentors and Coaches available, I’m surprised by how many CEOs I speak to still seem skeptical about their value. Just think — the world’s greatest athletes, the ones who get paid zillions of dollars because they are the best in the world at something, use MULTIPLE coaches DAILY to perfect their craft and keep them focused. Why should Rafael Nadal or Serena Williams have a trainer and a coach, but not you?

I’ve benefited over the years from the advice of more people than I can ever count or thank. But when it comes to being a CEO, I have leveraged the counsel of a CEO Coach or Mentor principally in three different areas:

- Functional topics on the craft of being a CEO from the lofty “how to run a board meeting” to the nitty gritty details of “how to do a layoff”

- Developmental/behavioral topics like “how I show up as a leader in the organization,” or “how to be a better listener”

- Team Effectiveness topics like “how do I get the most out of my leadership team,” or “why doesn’t Person X trust Person Y and how does that impact team performance?”

In some unusual circumstances, you can find a person who does all three of these things for you and can scale as you and your company grow. But for the most part, getting all three of these things requires engaging two different people, and maybe even more mentors.

What’s the difference between a CEO Mentor and a CEO Coach? Counsel on Item 1 above — what I would call CEO Mentorship — almost certainly requires someone to have been a CEO — preferably multiple times, or for a long period of time, or through multiple stages of company growth, or two or three of those qualifiers. This is the kind of person who can literally teach you how to do CEO things. These people are super busy, they won’t have open ended amounts of time for you, but you should expect sage wisdom and answers when you need them. And you can have more than one of them at a time, or change them out as your company evolves and your needs change.

Counsel on items 2 and 3 — what I would call CEO Coaching — frequently come together in a professional who is and has been for a while, a coach. The person might have had a significant career in business before becoming a coach but wasn’t necessarily a CEO. The person probably has some kind of academic grounding, like a Master’s degree in Organizational Development or Industrial Psychology, or a Certificate in Coaching. This is the kind of person who can do things for you and your team like facilitate meetings, run assessments like Myers-Briggs or DISC, and coach other leaders on your team. This person is dedicated to helping you be the best leader, professional, and CEO that you can be and must be both empathetic and comfortable pushing you hard.

Sometimes you get mentorship and coaching in the same person, but almost only with CEO Coaches who are also CEO Mentors by my definition above.

Five signs you need a CEO Mentor and/or Coach:

- You are playing ‘whack-a-mole’ — running from crisis to crisis in your organization and are not able to make time to think, be current with email, or make time for important things like hiring senior executives

- Your board is getting frustrated with you, your team and/or the lack of progress in the business

- The company isn’t scaling as fast as it should

- Your leadership team is not a cohesive team and you are in the middle of all decisions

- The company has high employee turnover and/or poor reviews on Glassdoor

Do yourself and your company a favor and invest in a CEO Coach and Mentor(s). It’s an investment in accelerating your own and your company’s success. In later posts, I’ll talk about how to hire and best leverage both Coaches and Mentors.

Next post in the series coming: How to Select a CEO Mentor or CEO Coach

Addicted to Ruthless Efficiency

Last week I wrote about The Tension That Will Come With the Future of Work. No one knows what the post-pandemic world of office vs. remote work will look like, but there are going to be some clear differences between how people will respond to being in offices or not being offices going forward. As I said in that post, I think the natural, gravitational pull for senior people will be to do more remote work, because of a combination of their commutes, their personal time, their work setups at home, and their level of seniority…but with the possible exception of engineers, “all remote” may actually not be in the best interest of a number of junior or more introverted team members.

Two things popped up in the last few days that are making it clear to me that there’s another issue all of us — whether you’re a CEO or CXO or an entry level employee — will face. We’ve become much more efficient in how we do our jobs and run our lives. In my case, I’ll go ahead and say it — I’m addicted to the efficiency and scarcity of social interactions in my work life now in a way that I’m going to find hard to unwind, so I’m calling it “ruthless efficiency.”

Example 1 is a time-based example. I’ve been doing virtually all client-related meetings, whether sales calls or customer success calls, in 30 minutes over Zoom or equivalent for a year now. Sometimes I even get one done in 15 minutes. Very, very rarely, I’ll book one for an hour.

One of my Bolster colleagues who lives not too far away in Connecticut is having drinks with a very important potential partner one night next week as the temperatures outside warm up here in the northeast. She invited me to join — and really, I should join. But then “ruthless efficiency math” sets into my thinking. Instead of a 30 zoom, this will take me three hours – an hour drive each way plus the meeting. Maybe I get lucky and I can do a call or two from the car, but is the meeting really worth 4-6x the amount of time just so I can be in person? Even though this is the kind of thing I would have done without hesitation a year ago…that calculus is really hard to make from where I sit today.

Example 2 is an expense-based example. We have spent basically $0 for a year on T&E. Now we are planning some kind of a multi-day team meeting a few weeks from now around the 1-year anniversary of the company to work on planning for the next couple quarters. The quarterly offsite, including travel, hotels, etc., has been a deeply-ingrained part of my leadership Operating System for 20-25 years now. OF COURSE we should do this meeting in person and offsite if the public health environment allows it and people are comfortable. But then “ruthless efficiency math” sets into my thinking. What’s this meeting going to cost? $10,000? Depends where we do it and how many team members come since we have people in multiple cities. But YIKES, that’s a lot of money. We are a STARTUP. Shouldn’t we use money like that for some BETTER purpose?

Forget the big things. I think we all realize that we don’t have to hop on a plane now and do a day trip to the other coast or Europe or Asia for a couple meetings unless those meetings are do-or-die meetings. It’s these little things that will be tough to readjust now that we’ve all gotten used to having hours upon hours, and dollars upon dollars, back on our calendars and balance sheets because we’ve gotten addicted to the amazing, and yet somewhat ruthless efficiency of the knowledge worker, pandemic, work from anywhere, get it done in 30 minutes on a screen way of life.

OnBoards Podcast

My podcast with OnBoards is live, talking with Raza and Joe about the importance of adding independence, first-time directors, and diversity to startup boards, and how Bolster helps companies achieve that quickly and inexpensively.

I’m writing a lot about Boards at the moment on the Bolster blog. We’re compiling all of those posts into a couple of eBooks. Once all of that is done, I’ll put some digests up here on StartupCEO.com as well as make the eBooks available for download.

But the gist of it is that we are working hard to break the logjam of diversity on startup boards, and we’re starting to meet with some great success with our clients.

The Tension That Will Come With the Future of Work

The Tension That Will Come With the Future of Work

A lot has been written about the Work From Anywhere life that knowledge workers are leading right now due to the pandemic, and what will come next. Fred has a great post on it, and I’m curious to see how his and Joanne’s “Home Office Away From Home” space called FrameWork does when it opens. In that post, he references a few other posts and articles worth reading:

- Imagine Your Flexible Office Work Future – Anne Helen Petersen

- We’re Never Going Back – Packy McCormick

- The Future of Offices When Workers Have Choice – Dror Poleg

Instead of entering the debate about what the future will look like, which no one really knows other than to say “not like the past,” I want to focus on a tension I’ve been mulling over lately, and that is the tension between a company’s leaders and its employees. You could also call it a tension between extroverts and introverts. And in this regard, Packy McCormick is both right and wrong about the debate: right in the sense that employees will make the decision, not companies; wrong in the sense that the best employees “are not going to work for companies that make them shave, get dressed, hop into a car or a crowded subway, and sit at a desk in an office five days a week with their headphones on trying to avoid distractions and get work done.” That’s a blanket statement that, as with most blanket statements, misses an incredibly important point.

That some people like, want to, need to, or benefit from working in offices more often than not.

That those people are some of the most talented, creative, and high potential people in an organization.

And that those people are frequently the ones with the least “voice” in an organization — new employees, younger workers, introverts, and people from underrepresented groups.

It will be really easy for senior people who, in many cases, have longer commutes and kids they are now accustomed to seeing a lot more, not to mention really nice and private home offices, to default to working from home. In many cases, they’ve already done more of that than most employees, well, because they can. But the problem is that those people are perfectly fine working from home. Work and decisions come to them. Their career trajectories are pretty set. They will seek out anyone in the organization to ask them any question, any time.

But think about the topic from the perspective of an entry level account coordinator, an associate product manager, a graphic designer in marketing, a financial analyst in the FP&A group, or an AR specialist in accounting. . Less exposure to decision makers can’t possibly help this. If you’re one of those people, here are the things you miss out on when there’s no office:

- You don’t get to participate in or overhear interesting conversations in the break/lunch room or at the water cooler about something going on in the company that you’re not working on. This reduces your ability to learn in unstructured ways at work or get thoroughly onboarded into a new company

- You don’t get to see who comes and goes from the office or different meeting rooms. This may sound silly, but watching a business in, seeing who is in a glass-walled conference room or what slides are up on the wall, helps employees stimulate good ideas about their day to day work. This limits your ability to connect the dots and better understand the big picture at work

- You don’t get to have a casual conversation with your department head or CEO in the elevator or hallway or a conference room between meetings. That “skip level” leader is much less likely to know who you are or what you do. This can make it harder for you, the next time you have an idea you want to share or feedback you want to give, to approach a leader. It also makes it a little tougher for you the next time you’re in line for some kind of promotion or development opportunity

Of course all employees CAN in theory make themselves known, can learn, can seek out others in the organization, and can try to re-create hallway serendipity from the comfort of their own Zoom screens. It just doesn’t come naturally to most; practically speaking for many, it’s impossible; and it’s particularly hard for younger or quieter team members. There’s a ton of research about how women in particular aren’t as comfortable advocating for themselves when it comes time to ask for a raise or a promotion. If you’re the CEO of a 100 person organization, you might be inclined to chat with the new entry level AR person at the coffee machine for a few minutes; you’re unlikely to be excited about a 30-minute Zoom with her.

(By the way, this whole construct may be different for engineering, where engineers are likely more comfortable with remote work AND aren’t held back in their career development as a result.)

I’ll close this post with an anecdote. As part of our work at Bolster, I was doing something called an Executive Team Scalability Assessment with the CEO of a $75mm SaaS company a month or so ago. When we were doing a review of how strongly each of his leaders role modeled company values, he paused when he got to one leader and said, “I honestly don’t know. That person has only been here 10 months, but don’t worry, that’s just because of the pandemic. I haven’t seen them in action.” 10 months! People will discover at some point that it was much easier to “lift and shift” an existing organization to the cloud in year 1 of the pandemic than it will be to sustain or build a culture with a lot of new employees in year 2 or 3 of remote-first work.

CEOs who care about their culture, their people, inclusion and belonging, and their people’s professional development will have to really re-think how things work if they are going to steer their companies towards remote-only policies, or even remote-first employees, and still be inclusive workplaces. That doesn’t mean it can’t be done. But gravitating to a remote-only way of life, even if it’s personally enticing or if some talented and vocal employees demand it, may not be in the best interest of their overall company and employee population.

Soliciting Feedback on Your Own Performance as CEO

(Excerpted from Chapter 12 of Startup CEO)

As a CEO, one of the most important things you can do is solicit feedback about your own performance. Of course, this will work only if you’re ready to receive that feedback! What does that mean? It means you need to be really, really good at doing four things:

- Asking for feedback

- Accepting feedback gracefully

- Acting on feedback

- Asking for follow‐up feedback on the same topic to see how you did

In some respects, asking for it is the easy part, although it may be unnatural. You’re the boss, right? Why do you need feedback? The reality is that all of us can always benefit from feedback. That’s particularly true if you’re a first‐time CEO. Even more experienced CEOs change over time and with changing circumstances. Understanding how the board and your team experience your behavior and performance is one of the only ways to improve over time. It’s easier to ask for feedback if you’re specific. I routinely solicit feedback in the major areas of my job (which mirror the structure of this book):

Strategy. Do you think we’re on target with what we’re doing? Am I doing a good enough job managing to our goals while also being nimble enough to respond to the market?

Staff management/leadership. How effective am I at building and maintaining a strong, focused, cohesive team? Do I have the right people in the right roles at the senior staff level?

Resource allocation. Do I do a good enough job balancing among competing priorities internally? Are costs adequately managed?

Execution. How do the team and I execute versus our plans? What do you think I could be doing to make sure the organization executes better?

Board management/investor relations. Do you think our board is effective and engaged? Have I played enough of a role in leading the group? Do you as a director feel like you’re contributing all you can? Do I strike the right balance between asking and telling? Are communications clear enough and regular enough?

Accepting feedback gracefully is even harder than the asking part. You may or may not agree with a given piece of feedback, but the ability to hear it and take it in without being defensive is the only way to make sure that the feedback keeps coming. Sitting with your arms crossed and being argumentative sends the message that you’re right, they’re wrong, and you’re not interested. If you disagree with something that’s being said, ask questions. Get specifics. Understand the impact of your actions rather than explaining your intent.

The same logic applies to internalizing and acting on the feedback. If you fail to act on feedback, people will stop giving it to you. Needless to say, you won’t improve as a CEO. Fundamentally, why ask for it if you’re not going to use it? And that leads right into the fourth point, closing the loop with the person who gave you feedback on whether or not your actions achieved the desired change.